Warner Bros. Discovery (NASDAQ:WBD) is starting to differentiate itself in an increasingly crowded entertainment space. The company has experienced major successes just as competitors like Disney (DIS) have begun to lose steam. In fact, Warner Bros. Discovery recent movie, streaming, and video game hits The Last of Us, Hogwarts Legacy and Barbie have all dominated viewing/sales/box office charts in the respective genres.

While WBD is dwarfed by larger competitors like Netflix (NFLX), Disney, and Amazon (AMZN) in terms of market capitalization, WBD arguably has the strongest IP in the entire industry. WBD’s war-chest of popular franchises like Game of Thrones, Harry Potter, and DC, along with its strategic shift, could help the company over its current hurdles and thrive in an increasingly crowded space.

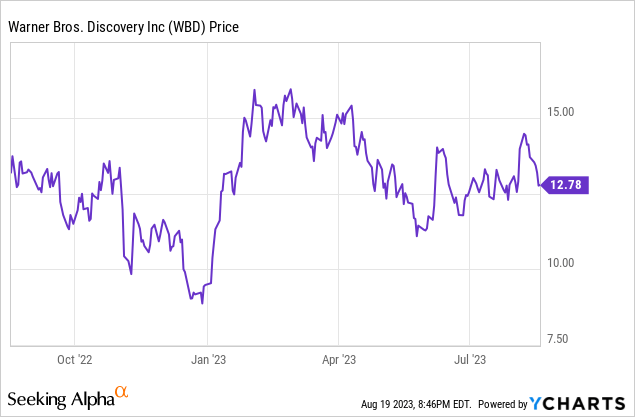

WBD has managed to stabilize over the past year as competitors like Disney have seen their valuations plummet.

Maximizing on WBD’s Unparalleled IP

WBD arguably has the strongest IP library in the entire entertainment space, especially as Disney’s Star Wars and Marvel have begun to experience major dips in popularity. While WBD has previously been unable to capitalize on its library, the company’s new management has done a far better job leveraging its most popular franchises.

WBD’s growing focus on its proven and top-performing IPs like Game of Thrones and Harry Potter have already started to pay off in a big way. House of the Dragon and Hogwarts Legacy, for instance, have helped establish both WBD’s streaming and gaming divisions as serious competitors in their respective industries. In fact, HBO’s streaming business is now outpacing Disney+ in terms of growth.

WBD’s management has been particularly shrewd in leveraging the increasingly competitive landscape. CEO David Zaslav has been open to the idea of licensing many of its popular titles to other platforms, despite the fact that WBD is competing with these platforms. WBD understands that the upside gained from licensing its IP to competing platforms like Netflix or Amazon Prime Video greatly outweigh the downsides.

Growing the popularity of its IP through an “arms dealer” approach is far more lucrative than siloing content on a single platform in an increasingly fractured landscape. Sony (SONY) has proven this to be true, as it stands as a clear financial winner in the streaming wars. In fact, there is very little to be gained from content exclusivity for anyone not named Netflix, as the streaming model itself is proving to be far from lucrative, especially for the smaller players.

WBD has begun to license many of its titles to competing platforms.

HBO

Streaming Turnaround

WBD has made great efforts to improve its financial situation over the past year. The company has managed to find cost savings through major restructuring efforts and programming cuts to its less popular titles. Despite the backlash such drastic actions have garnered, the company appears to be successfully turning things around. In fact, WBD’s streaming service Max will likely join Netflix as one of the few profitable streaming services very soon.

Despite the fact that WBD is now licensing much of its popular streaming titles like Ballers to other platforms, the company is still managing to keep a strong streaming customer base. This has largely been due to some major streaming hits like House of the Dragon and The Last of Us attracting new customers and retaining old customers. With even more popular shows coming to Max in the coming years, Max should continue to see healthy growth for the foreseeable future.

Large Risks Remain

Despite recent successes like Barbie, which will likely end up being the highest grossing movie of the year, WBD still faces major obstacles. The company notably has an enormous debt load, as it ended Q2 with $47.8 billion in debt and only $3.1 billion cash on hand. This amount of debt should significantly hamper the company’s ability to capitalize on its franchises, even as it gains momentum from recent successes.

WBD has also experienced unprecedented flops with many of its DC titles like Shazam and The Flash, which is extremely concerning given how important the DC brand is to the company. In fact, DC could be a determining factor in WBD’s long-term success, given how much the company has already invested in the brand. On the bright side, DC is set to undergo a complete revamp in a couple of years.

Conclusion

WBD is just starting to find its footing as competitors like Disney begin to lose steam. The company’s IP is stronger than it has ever been and will likely continue to grow in popularity as rival brands like Marvel and Star Wars continue to fade. Despite a relatively large debt load, WBD has a great deal of potential upside at its current market capitalization of $31B and low P/S ratio of 0.7.

Read the full article here