Dear readers/followers,

When I wrote about Edenred (OTC:EDNMF) (OTC:EDNMY), there frankly wasn’t much interest for a French company in this sector. I didn’t expect much from my coverage there, but I did expect some more interest than what it got. However, that’s why I believe this article will serve as a healthy update for you.

Because Edenred, in accordance with my overall expectation for the company, has actually outperformed. The ADR fails to capture this – which is why I would look at native share prices, to begin with, but at this time, on a 1-year basis, the company is up double digits. And considering that when I wrote about it the company was trading at sub-€40/share levels, this company is currently outperforming most of the market indexes as it currently is trading close to €60/share.

My small position in the company has therefore outperformed, and if you ignored the article or didn’t invest, well, you may have missed out on some growth here.

In this article, I mean to provide you with an update to this investment, and why I view the company as less of a “BUY” here, but still with potential upside.

Edenred – Plenty to like about Employee benefits

I do not know the entire global industry in the field of employee benefits – but it’s a big one in Europe. That’s why industry giant Accor had a whole service section, which was spun off as Edenred in 2010 to a native French listing. What has been a ticket/coupon-based business became mostly digital in 2012, launched the Ticker Restaurant card the same year, and we find it with almost 90% of the current lineup of products being fully digital.

The company’s business idea is to offer companies the ability to offer their employees prepaid benefits, which in most operating geographies come with significant tax-related benefits. In effect, it’s easier for companies to pay for employee meals than it is for the employees to pay the meals by themselves. This is how I run my businesses – and this benefit is a great argument from the corporate side. It’s cheaper than a salary bump, it’s a “quality-of-life” sort of benefit that’s really easy to argue for. A win-win situation, at least as I’ve seen it.

The company has a degree of fundamental safety. In fact, saying a degree is an understatement. Edenred is A-rated from S&P Global and comes with a 1.7% yield, and an unbroken line of payouts in dividends for almost a decade. Due to various capital structures and choices, the company actually comes with a 121% LT debt/capital ratio, but there is more to that is reflected by the S&P Global credit rating. It has a current market cap of around €14.7B, and the results for the business, including the latest set of results, have actually been very positive.

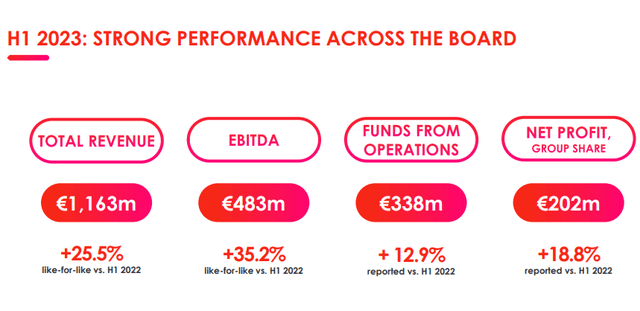

What we have to consider are the half-year company results, where the company was able to confirm a significant revenue growth rate of 26.1% or 25.5% LFL, with EBITDA growing more than 32% or 35% LFL, and an EBITDA margin of over 41%.

Cash generation was strong, and the company recently got that bump in its credit rating, affirming for the first time this A-rating.

The company acquired GOintegro, addressing the LATAM market, Reward Gateway, for UK/Australia/US, and is continuing on its journey to offer worldwide employee benefits/engagement rewards and solutions.

The company can now estimate an EBITDA run rate of over €1B, which would be a YoY increase of over €200m compared to the 2022 fiscal. Overall, the high-level view in terms of results is extremely good and in line with expectations both in my previous article, but also for forecasts for this company.

Edenred IR (Edenred IR)

While the growth rate in terms of revenue isn’t as high as it was during record years, such as 2020, it’s still well above a 15% level. Given how the company improves its earnings growth as well, it’s fair to say that Edenred is certainly in a bit of a “growth” phase still, and commands a premium in accordance with this expectation.

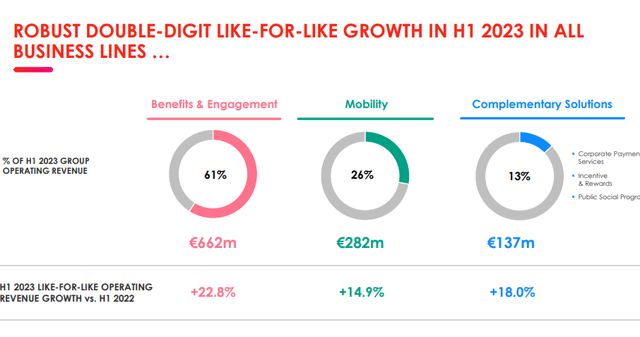

The current growth is robust. It’s across the company’s segments – both the main segment, the mobility segment, and the complementary solutions segment.

Edenred IR (Edenred IR)

My real only current regret is that I did not stick to this company closer and buy more shares when it was incredibly cheap. Because the fact is, it’s no longer incredibly cheap.

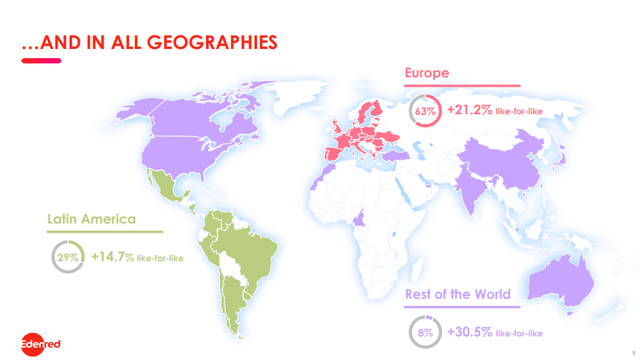

Oh, and by the way – that growth we’re seeing above, that’s not just the EU. It’s growth on a worldwide basis.

Edenred IR (Edenred IR)

This is one of the few companies I currently review that not only managed significant volume growth, but also managed to drive earnings more than volume, seeing synergies here. The company’s margins are up, not down.

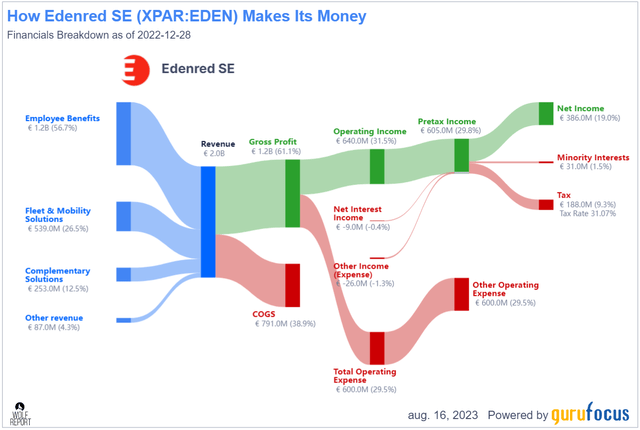

Just how good is this company in context? Well, it’s a service company that manages Gross margins of close to 52%, and net margins of over 18%. No matter how you slice that, this is one of the lowest COGS I’ve seen in a business this size. Usually, this is accompanied by outsized OpEx due to different weightings, but no – OpEx here is just below 30%.

Edenred Revenue/net (GuruFocus)

The company’s revenue and earnings trends over time are solid, and the company has not been ROIC/WACC unprofitable in over a decade, since listing the company after the GFC. We’ve seen some dilution over the past few years, but this is natural given the company’s significant overall expansion.

The addition of mobile pay and digital services is adding to the company’s appeal here. Due to how the company leverages the various tax rules in the nations where they operate, Edenred is also one of the largest tax refund service providers in all of Europe. VAT refunds are now available in 31 countries, including gas, tolls, repair services, and accommodation. The company even offers partial excise duty refunds in 7 countries – and the company is growing in core areas (like France) as well as in new growth areas across the Atlantic.

Edenred IR (Edenred IR)

Future investments – and the company is investing heavily – are going into things like API, Cloud platforms, scaling its payment platform, and data/AI. The company already has over €100B in annual payment volume, and this is set to expand further.

The company works on a combined benefit and engagement basis, which is something I believe is set to grow on a forward basis.

Edenred IR (Edenred IR)

And the additions of the new M&A’s you see above – GOintegro and Reward Gateway, will add the leading SaaS employment engagement platform with an already-existing footprint in several countries and almost 10M combined users before even considering what’s already on offer in Edenred.

The company is targeting inorganic growth at this time – these latest M&A’s examples of this. Given the company’s excellent track record of inorganic growth integration, I have no issue with this company playing to their strengths. The company’s main markets remain central European geography and USA, but now adding Australia and South/Latin America as well.

The company’s new fundamentals come with a stable outlook. While financial costs are obviously up due to interest rates, and a 100 bps resulting in around €16M in annual pre-tax financial expense, the company is still able to borrow money at a comparatively low 3.6%, and no maturities in 2023 whatsoever, with only a small €500M maturity in 2024, which in this case is a convertible bond.

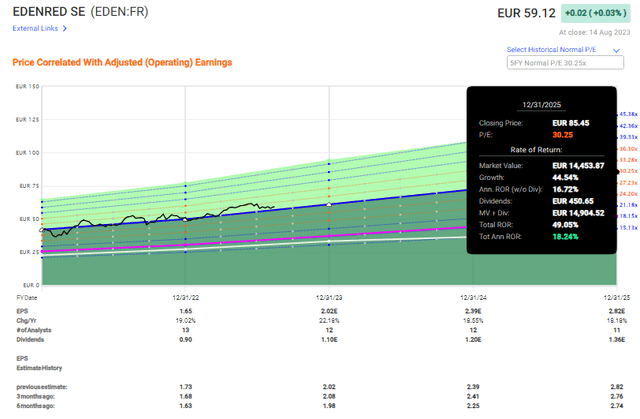

2023 is set to be a record year, with over a billion in estimated EBITDA (euros). Based on this, I would look at the company from a valuation perspective in the following manner.

Edenred Valuation – Upside, but based almost solely on growth, not on dividends or reversal.

So, the company is for certain a story about growth – and where we’re going based on that growth. The company has managed a 5-year growth rate close to 20% in terms of EPS, and is expected to maintain that 20% yearly growth rate in the future as well.

This also shows us one of the problems with the company. Such a growth rate comes with a P/E, and in this, the company sticks pretty close to around 30x P/E, with a yield of around 1.7%.

I realize it’s a tall order for anyone to pay 30x P/E for a company out of France with an A-rating in S&P Global that you may not have heard about before. Most people have no idea what Edenred is when I ask them about it.

Still, this is what you can expect in terms of RoR, if you’re actually willing to give the company that sort of target.

Edenred Upside (F.A.S.T Graphs)

At this point, if you follow my writing, you know my strategy for beating the market over time. I buy over-qualitative companies at undervalued prices, and I keep them until they go into overvaluation before rotating/trimming them. I’ve been doing this for years, and this is what I’ll continue to do here on a forward basis.

This company does not share some of the undervaluation specifics of some of the opportunities I typically consider appealing. That being said, I consider that 30x P/E as safe and as clearly established as some of the other companies with over 30x P/E that I accept – such as water companies.

Edenred is an over-qualitative business service company, and analysts are equally keen of ownership here. 14 analysts follow the company, and 12 of those are at “BUY” or “outperform” ratings. My own PT of around €62/share is conservative compared to the range of €61 to €72 and the average of €68/share that’s being kept here – but I do prefer not to estimate this company above 30x, even if the growth rate is good. The company has shown us that financing costs will impact the bottom line by around €16M per year per percent here, and I do expect we’ll see more interest rate hikes in Europe.

For that reason, I’m going to €62/share, but not above, and consider Edenred to be a “BUY” here.

Questions?

Otherwise, here is my current thesis on Edenred.

Thesis

- The current thesis for Edenred is a positive one. The company is a market leader in employee engagement and rewards, with solid market-leading positions in incumbent and attractive geographies, including Europe and the USA. It’s focusing on inorganic expansion, already catering to almost 10M new customers across Australia and South/Latin America with its most recent M&A’s.

- The current valuation, while not close to as favorable when I last called for a “BUY” for Edenred, could still make sense to you as a long-term investment and with an eye to total return. There is double-digit potential in Edenred.

- I give the company a fair value target of at least €62 for the long term, which still makes it a “BUY” here at this time, with an overall share price of €58 here.

Remember, I’m all about :1. Buying undervalued – even if that undervaluation is slight, and not mind-numbingly massive – companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn’t go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

The company has a solid upside, provided you accept that the upside is primarily based on growth, not reversal or undervaluation. I am willing to accept this in a few cases, and this is one of them.

I say “BUY”, and I say PT is €62.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here