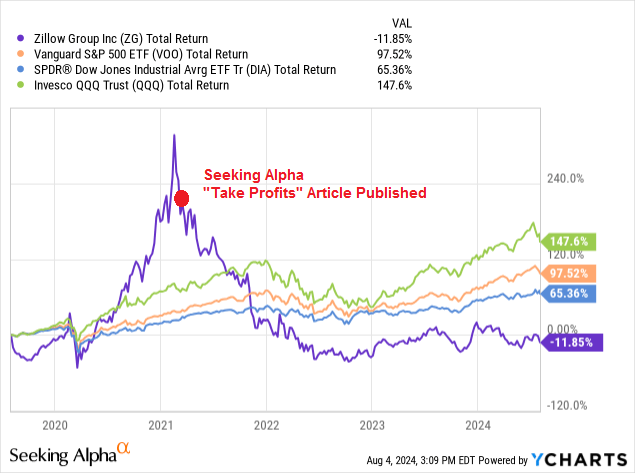

Seattle, Washington-based Zillow Group, Inc. (NASDAQ:ZG) operates the very popular Zillow.com website where pretty much everyone I know goes to check on their home’s “Zestimate” value and to snoop on the home values of friends, acquaintances, and the rich-n-famous (and look at photos of those homes). Indeed, the company’s mobile apps and websites are so popular that they have hundreds of millions of visitors every month. That said, back in March 2021 I advised Seeking Alpha investors to Take Profits in Zillow based on its extremely elevated valuation. It was a good call: ZG has dived 71% since Seeking Alpha published that article and the stock has obviously and drastically under-performed the broad market averages over the past 5 years (see chart below). But now that a lot of hot air has been released from the Zillow balloon, today I’ll take a fresh look at the company to see if its stock is now worthy of consideration in your portfolio.

YCharts

Investment Thesis

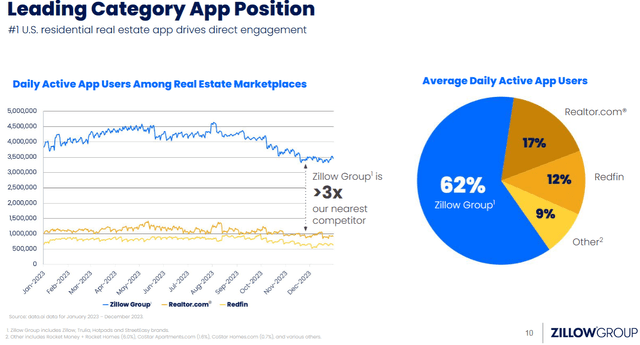

As mentioned previously, Zillow has a very popular website. Indeed, in the company’s February 2024 Presentation, information from data.ai is cited that shows Zillow operates far-n-away the #1 U.S. app in the Residential Real Estate category:

Zillow

However, as I pointed out in my follow-up articles on Zillow (see here and here), a good app does not necessarily make for a compelling investment. Indeed, Zillow has made several attempts in the past to better monetize the website’s popularity – including the “iBuying” and “Premier Agent” initiatives – and to better tap into what is a huge TAM (multiple $100’s of billions) if we combine the Zillow.com website and apps potential with real estate transactions (buyers & sellers), mortgages, and rentals (see slide 13 of the previously referenced Feb. Presentation). The latest initiative is called the “Housing Super App”, which is targeted at solving consumers’ and partner’s real estate “pain points”:

Zillow

Zillow is also targeting the “Rentals” market and has been adding features like “Touring” to its website. Since it has been quite some time since I have covered the company, let’s take a closer look at its most recent earnings report to see if it has (finally…) figured out the “secret sauce” to monetize its very popular website.

Q1 Earnings

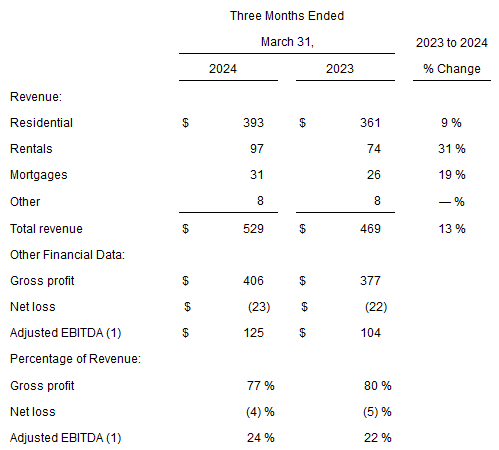

Zillow released its Q1 EPS report back on May 1st. Q1 highlights are shown below:

- Revenue of $529 million was +13% yoy.

- GAAP earnings were a net loss was $23 million (4% of total revenue), or $0.10/share – a penny worse than the $0.09/share loss in Q1 of FY23.

- Adjusted EBITDA was $125 million (24% of total revenue).

- Traffic to Zillow Group’s mobile apps & sites was 217 million average monthly unique users (flat yoy). Total visits during Q1 were 2.3 billion (+3% yoy).

- Share-based compensation in Q1 was $108 million.

The company operates three primary segments, and the revenue results are broken out below:

Zillow

As you can see, revenue in Residential ($393 million), the company’s largest segment (74% of total revenue), is growing the slowest (%). Rentals revenue ($97 million) grew 31%, but only equated to 18% of total revenue. Mortgages and “Other” combined for only 7% of total revenue.

Zillow did not break out the gross profit, net loss, and adjusted EBITDA numbers for each segment, but we can see that the entire business lost money (again…) in Q1 while adjusted EBITDA did grow 20% yoy.

Zillow is scheduled to release Q2 results on Wednesday. According to Yahoo Finance (24 analysts), the Q2 consensus revenue estimate is $538.3 million, which would be +13.8% yoy.

According to Seeking Alpha’s Earnings Calendar, consensus Q2 earnings estimates are for:

- Adjusted earnings of $0.27/share.

- A GAAP loss of $0.19/share.

That is, the Q2 GAAP loss is expected to be $0.09/share worse than Q1.

Valuation

On a GAAP TTM basis, ZG has lost $0.69/share, so there is no “P/E”. The company pays no dividend, so there is no yield.

Seeking Alpha says the forward P/E=32.8x. However, that is on an “adjusted” earnings basis (i.e., non-GAAP), and it is still a significant premium as compared to the S&P500 (27.9x on a GAAP basis).

According to data compiled by Seeking Alpha, TTM gross profit of $1.55 billion is actually below that of FY2021 ($1.81 billion). Not a good look for a “growth” company.

Bottom line: in my opinion, the Zillow Group is still trading at a relatively high valuation, with much of the future potential good news already fully baked into the stock price.

Risks

In the Q1 10-Q, we can see that total debt was $1.7 billion versus cash and cash equivalents of $2.9 billion (which was +$100 million from the end of Q4 FY23). From that standpoint, the company’s balance sheet is strong.

On the Q1 conference call, we learned that Zillow has repurchased a total of $100 million shares YTD. That could be throwing good money after bad if the company is not able to accelerate its profitability metrics. That said, the total fully diluted share count has been reduced from 262 million at the end of FY21 to 234 million at the end of FY23. The point here being that the share repurchase program is positively outpacing share-based compensation issuance.

Downside risks include investments in the “Housing Super App” not coming to fruition from an ROC standpoint, although I must say I have much more confidence in this strategy as compared to the ill-fated “iBuying” initiative, which I predicted would fail (and boy did it).

Upside risks include a revitalization of the housing market with coming Federal Reserve interest rate cuts, and that the “Super App” will benefit and gain traction from a more vibrant real estate sector.

Summary & Conclusion

Despite the big drop in ZG’s stock price, I still find the valuation level to be quite rich as compared to its growth rate. That said, I do have more confidence in the company’s new “Housing Super App” strategy as compared to its past initiatives to better monetize the awesome website. And, rate cuts from the Federal Reserve should provide a tailwind of sorts going forward. However, I just can’t get past the fact that after being publicly traded for more than a decade now (boy, how time flies – Zillow started publicly trading in 2011) the company still is not demonstrating it can be profitable on a GAAP basis. Sorry, Zillow lovers, but I maintain my SELL rating on the stock. That said, I will be watching Q2 results and commentary for signs that the “Housing Super App” is gaining traction and, if it looks promising, I may upgrade the stock to HOLD in the near future. Meantime, investors should view the first stock chart in this article, again, to remind themselves of the huge opportunity costs of investing in ZG stock.

Read the full article here