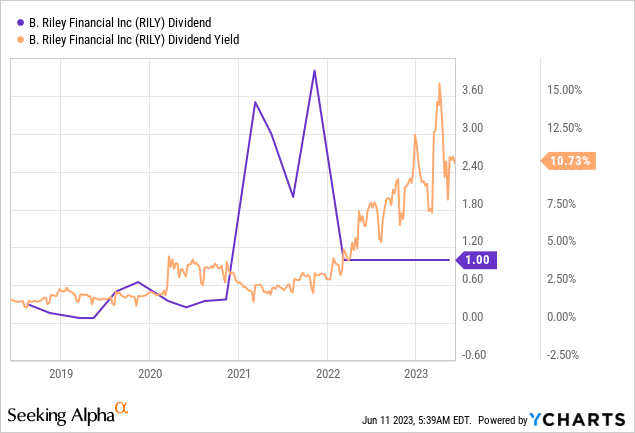

B. Riley Financial (NASDAQ:RILY) last declared a quarterly cash dividend of $1 per share on its common shares, in line with its prior payout and for a 10.7% annualized forward yield. The yield of the Los Angeles-based diversified financial services company has been pushed to its highest level in over half a decade on the back of shares down by 27% over the last 12 months. Is the double-digit yield now a buy? It depends. B. Riley has a short interest of 28%, one of the highest in the Nasdaq, as bears bet on a near-term dividend cut against fiscal 2023 first-quarter earnings that saw its net income come in at $15.1 million, around $0.51 per share. Critically, this meant its payout ratio stood at 196% for the quarter.

However, bulls would be right to flag that cash from operations at $52.6 million was markedly higher than earnings and was more than enough to cover the $46.9 million in common stock dividends paid during the quarter. It was also sufficient to cover the $2 million in preferred stock dividends. The mismatch between earnings and actual cash generated was driven by a number of non-cash items including a stock-based compensation expense of $13.7 million. B. Riley’s management was incredibly upbeat on the prospect of their business during the first quarter earnings call, flagging their confidence in maintaining the dividend and the business opportunities being chased.

Building Scale And Reducing Risk

B. Riley Financial

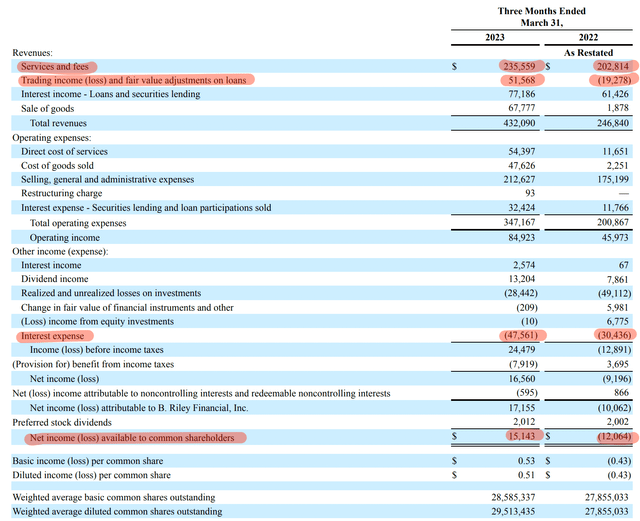

The company operates across six business segments that cover several areas of expertise including investment banking, principal investments, and wealth management. B. Riley realized revenue of $432.1 million for its fiscal 2023 first quarter, an increase of 75.1% over its year-ago quarter. This growth was driven by services and fees revenue that grew by $32.75 million over its year-ago comp. Trading income and fair value adjustments on loans of $51.6 million was a huge improvement on a loss of $19.3 million in the year-ago quarter.

B. Riley Financial Fiscal 2023 First Quarter Form 10-Q

The company ended the quarter with $210 million in cash and equivalents, $1.04 billion in net securities and other investments, and $772 million in loans receivable at fair value. This was a strong liquidity position that was offset by a total debt balance of $2.5 billion as of the end of the first quarter. This meant a net debt position of $427 million against total cash, investments, and other assets. Its debt balance drove interest expenses of $47.56 million during the first quarter, up around $17.1 million year-over-year.

B. Riley Financial Fiscal 2023 First Quarter Form 10-Q

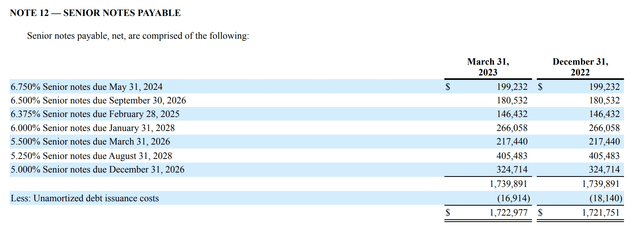

However, upcoming debt maturities are quite staggered. There are no senior notes maturing in 2023 with $200 million due by the end of May 2024. Another $146.4 million will come due in 2025 with 2026 seeing the bulk of maturities worth $722.7 million. Critically, B. Riley has the liquidity to meet its upcoming maturities and could always refinance with the Fed funds rates, currently at 5% to 5.25%, unlikely to be at its currently elevated level high in two to three years. The first quarter was incredibly positive for the bulls with B. Riley generating $80 million of operating EBITDA against a period of weak investment banking and liquidation activity.

Indeed, mergers and acquisitions activity has fallen to its lowest level in more than ten years with US M&A volume falling 44% to $282.7 billion. Recent B. Riley transactions include an at-the-market offering for Main Street Capital (MAIN), sell-side advice to Canadian book manufacturer Marquis Book Printing which got acquired in June, and co-managing a common stock offering for Hannon Armstrong Sustainable Infrastructure Capital (HASI).

The Commons Or Preferreds?

B. Riley Financial Fiscal 2023 First Quarter Form 10-Q

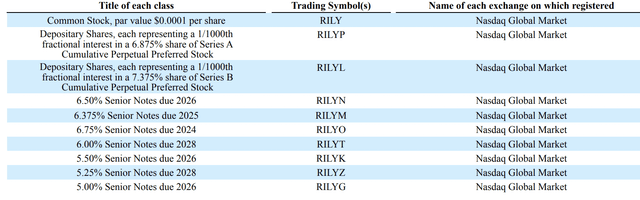

B. Riley’s series B preferred shares (NASDAQ:RILYL) have the highest headline coupon rate at 7.375% and are currently swapping hands at $20.58 per share, a roughly 17.7% discount to their $25 par value. To be clear, these cumulative preferreds whose quarterly dividends are fully covered by highly cash-generative B. Riley can be bought for 82 cents on the dollar and an 8.96% yield on cost against a $1.84375 annual coupon.

QuantumOnline

The company also has a number of baby bonds with similar yields and discounts as the market sourced on fixed-income securities on the back of the Fed’s interest rates hikes. This discount to par could get closed once interest rates normalize against a still healthy economy. The market is currently pricing in a 70% chance of the Fed pausing rates at its upcoming June FOMC meeting to set the backdrop for what could be a recovery of the baby bonds and preferreds. However, I’m leaning towards the commons here with their covered yield that’s 174 basis points higher than the Series B preferreds and as a potential call option on the eventual recovery of the capital market.

Read the full article here