Summer is upon us, and despite macroeconomic doldrums, most market-watchers are still expecting a banner travel season as consumers continue to catch up on post-pandemic travel. Airfare remains elevated, and hotel rooms and vacation homes remain in high demand with average daily rates soaring to new highs.

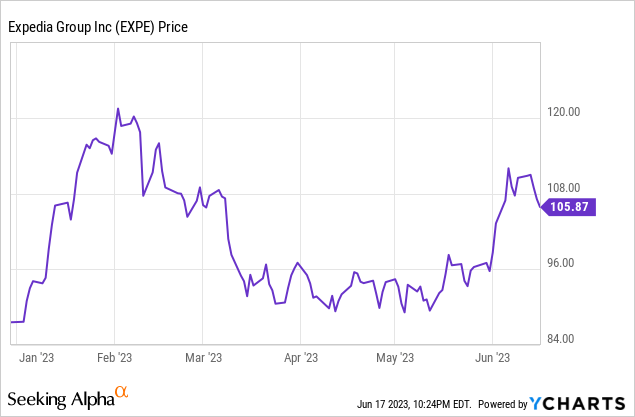

Amid this backdrop, Expedia (NASDAQ:EXPE) is a great stock to look into. The second-largest of the online travel agents (OTAs) behind Booking.com (BKNG), Expedia stock is up ~20% this year: less than its larger rival, but better than the S&P 500.

Expedia may not be the most successful OTA, but a cheap valuation makes up for its uncertainties

Earlier this year, I expressed a bullish opinion on Booking.com, but my enthusiasm is more for the travel space and OTA industry in general rather than for particular names. Vis-a-vis Booking.com, Expedia remains a slightly more convoluted and controversial name (hence the valuation disconnect versus Booking, which I’ll touch on shortly).

Two things are at play here. First, Expedia has long had a profitability gap versus Booking.com. This is in part driven by Booking.com’s successful pivot to a merchant booking model (representing ~85% of its hotel bookings), wherein Booking directly handles payment from the customer. Expedia, however, still is a roughly 50/50 split between merchant bookings and the agency model, where hotels collect payments and send the OTA its commission after the stay.

Second, Expedia is in the midst of integrating its vacation rental subsidiary, Vrbo, into its tech stack and rewards system this year. Though Expedia acquired Vrbo more than a decade ago, integration had not been a major priority for the company until now, and investors are nervous about the outcome and execution.

In spite of this uncertainty, we are seeing strong trends for Expedia and I think there is a strong bull case to be made here, driven by the following factors:

- Red-hot travel demand. After a quiet COVID season, travelers are catching up on lost vacations. Picking up on strong end-customer demand, airlines and hotels have also raised rates, which benefits Booking’s commission model.

- Work from anywhere. Airbnb (ABNB) has cited this as a benefit to its growth in stays: now that many companies have allowed remote-work from anywhere, many travelers are opting to stay in vacation destinations for extended chunks of time, bringing their work laptops with them. This new “format” for travel has increased wallet share and spending on overall travel.

- Vrbo is Expedia’s answer to Airbnb. Whether customers want to stay in a hotel or book a vacation rental home (both formats of stays, we now universally agree, are two entirely different types of vacations, with the former generally offering more creature comforts and the latter a more authentic, local experience), Expedia has the right option for its customers’ preferences.

- One Key will unify Expedia’s brands. Outside of its namesake site, Expedia is also home to Orbitz, Vrbo, Hotels.com, Hotwire, HomeAway, Egencia, and a number of other brands. The company’s plan to unify all of its rewards programs under “One Key” this year will hopefully help to maximize the group’s marketing spend and boost its following.

Above all, I think a modest valuation is the ultimate incentive to invest in Expedia. At current share prices near $106, Expedia trades at a market cap of $15.68 billion (versus a near-$100 billion market cap for Booking.com, though the latter is also immensely more profitable despite being only slightly larger from a revenue scale perspective). After we net off the $7.10 billion of cash and $6.24 billion of debt on Expedia’s most recent balance sheet, the company’s resulting enterprise value is $14.82 billion.

For the current fiscal year, meanwhile, Wall Street analysts are expecting Expedia to generate $12.92 billion in revenue (+11% y/y) and $9.22 in pro forma EPS. And if we assume Expedia’s TTM adjusted EBITDA margin of 19.5% holds, adjusted EBITDA in FY23 will be roughly $2.52 billion.

This puts Expedia’s valuation multiples at:

- 1.1x EV/FY23 revenue

- 5.9x EV/FY23 adjusted EBITDA

- 11.5x P/E

Booking.com, meanwhile, trades at a ~17x P/E ratio. I like both stocks given the strength in travel trends, but I think Expedia at its much cheaper valuation is especially attractive.

Q1 download

We should also clarify that despite its cheap valuations, Expedia isn’t exactly suffering from a fundamental perspective. The Q1 earnings highlights, which Expedia released in early May, are shown below:

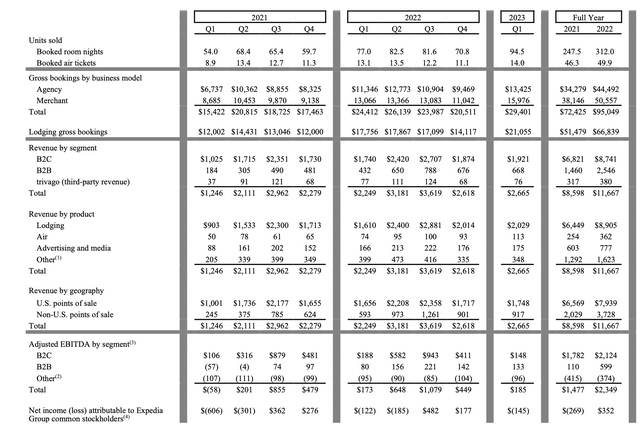

Expedia key highlights (Expedia Q1 earnings release)

Expedia’s total revenue grew 18% y/y to $2.67 billion, beating Wall Street’s expectations. As shown as well in the chart above, room nights booked reached a multi-year high at 94.5k, up 23% y/y. From a dollar perspective, total gross bookings of $29.4 billion grew 20% y/y, while lodging gross bookings (more than 70% of the company’s total) grew 19% y/y.

Note as well that Q1 tends to be a seasonal low for Expedia in terms of both revenue and profitability: the true test will come during the summer travel season which spans across Q2 and Q3.

The company notes that strong end-customer demand was buoyed by a resurgence in desire to travel internationally, a reopening in Asia, and travel to major cities and capitals. Per CEO Peter Kern’s remarks on the Q1 earnings call:

We posted our highest ever quarter for lodging gross bookings and free cash flow and our best first quarter for revenue. Throughout the quarter, we saw strong consumer demand with acceleration in international and big city travel and more of Asia reopening. The reemergence of major international cities has meant increased hotel demand, offset in part by flattening demand in vacation rentals as travel demand mix to urban destinations over extended beach and mountain trips. Similarly, air has continued to mix towards international travel and away from COVID era concentration in domestic.

By and large, prices have held up quite well after several years of inflation. We’ve seen lodging ADRs hold fairly steady across geos. Air ticket prices, however, continued to increase as strong demand continues to outstrip capacity. The only area where we have seen any meaningful decline in average daily rate is in the car rental space where larger inventories have allowed rental companies to drive more volume at the expense of price.

Overall, we are pleased to see broad travel demand remain strong in what appears to be a more structural post pandemic environment of people prioritizing travel above most other categories of spend. This has held up despite inflation and recession worries and even, more recently, bank system concerns. While economists continue to debate potential recession outcomes and clearly many unknowns are still out there, consumers have so far shaken it off and continue to travel.”

The company also notes as well that it has integrated ChatGPT as a plugin into the Expedia app, building on an AI tech stack that Expedia has already been leveraging to sort recommendations and enable price comparisons.

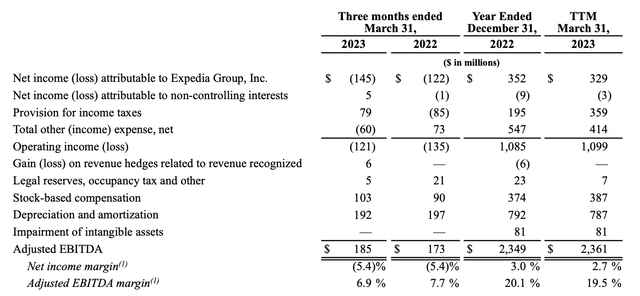

Expedia Q1 results (Expedia Q1 earnings release)

From a profitability standpoint, as shown in the chart above, Expedia generated $185 million of adjusted EBITDA in the first quarter, up 7% y/y and representing a 6.9% margin, down 80bps from 7.7% in the year-ago quarter. The main drag here was FX, which was a 300bps headwind on revenue growth and an 80bp headwind on adjusted EBITDA margins – offsetting gross margin gains driven by lower customer support call volumes. Again, Q1 is a relatively minor quarter for Expedia – I’m optimistic that strong travel demand will lead to double-digit revenue growth in Q2 and Q3 and help Expedia begin to achieve operating leverage.

Risks and key takeaways

Long underrated in the OTA space, I think Expedia benefits from both a low valuation plus the tailwinds of strong consumer travel demand.

There are, of course, downside risks here. First, as previously mentioned, the company is working on integrating Vrbo into its tech stack as well as rolling out the One Key loyalty program across its brands. The latter may be perceived as a devaluation (especially as Hotels.com’s beloved “Stamp Rewards” get replaced by the new program) and cause Expedia to lose share to Booking.com. In addition, from a macro perspective, the current travel surge may quickly dissipate if layoffs and general consumer malaise overtake pent-up travel demand.

I’d say, however, that these risks are already more than contemplated in Expedia’s bargain valuation. Stay long here and stay patient for Expedia’s rebound as it claws its way back to a more normalized price.

Read the full article here