Opportunity Overview

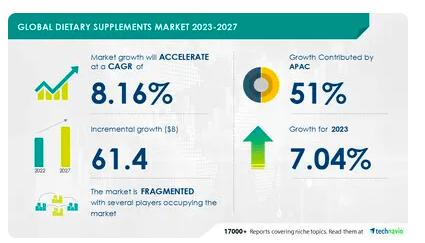

The nutraceuticals industry still has ample growth potential, but growth may be weaker relative to 2020-2021. This industry should still experience moderate growth as consumers become more health-conscious.

Thorne HealthTech (NASDAQ:THRN) is well-positioned to capture the growth of the nutraceuticals industry, particularly in higher-end segments. The company is creating more technical, higher-end products and is focusing on strategies like improving the user experience. The company also successfully sells its products directly to consumers and does not have to rely as much on Amazon and other companies.

I think shares of Thorne have moderate upside in the coming years and that the stock price is undervalued. However, weaker macro data and industry headwinds may result in a lackluster performance in 2023.

Company Performance

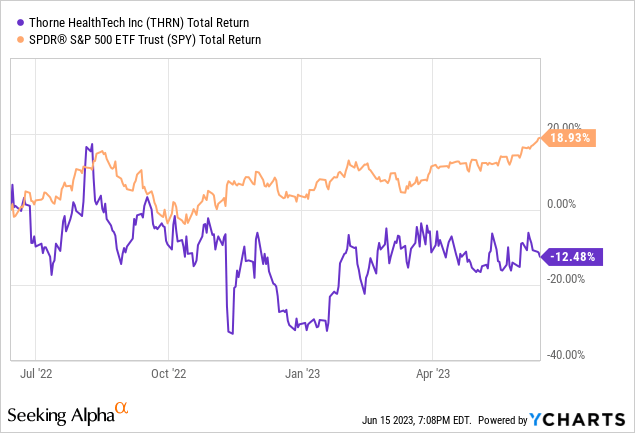

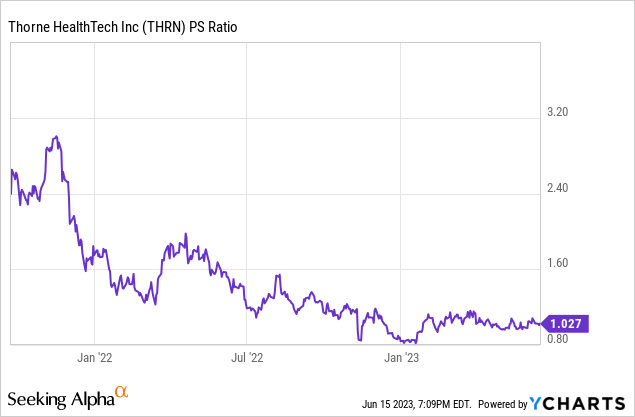

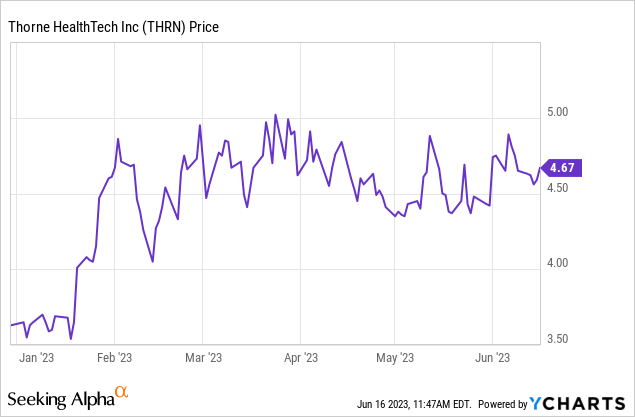

Thorn has underperformed the S&P 500 by around 30 percentage points in the past year, which has resulted in attractive valuation on a price to sales basis. Healthcare products companies can trade as high as 4.7x revenue, especially if they are in a high growth phase. Thorne’s shares are cheap based on the sector average and its historical average.

Even though industry sentiment is not as positive, as the industry’s growth rate has declined significantly, Thorne’s business is still performing very well. The company’s 2023 guidance is very favorable, so this stock may trade at a discount to sales if it continues to move sideways. The stock is also extremely cheap on a price/earnings basis. The company’s 2022 EPS was $0.30, so it currently trades at 15.6x 2022 earnings. Thorne has above industry margins and is growing rapidly, so there is room for its NIM to expand in the future if its revenue continues growing at 20+%.

2023 looks like a solid entry point, as investors may be over-concerned about Thorne’s ability to perform well in this economic environment. Although the risk of consumers switching to lower cost supplements is present, it will not likely significantly harm its operations this year.

Thorne has a lot of value added products that are superior to lower end nutraceutical companies’ products, and many consumers may still be willing to spend the same amount on these products. A recent LEK survey found that consumers were willing to spend as much money on supplements in 2022 as they were in 2021.

Latest Innovations

Thorne has been making massive breakthroughs lately and has developed new testing products and devices. Moreover, it also regularly collaborates with Mayo Clinic. These are several of many developments that can help the company offset the price-sensitive preferences of some consumers. Companies that purchase a test kit may be more likely to buy Thorne’s products. Moreover, positive studies and product releases can help boost consumer confidence.

Testing Updates: The company currently offers 11 different at-home testing products. Customers can use these to monitor their health and to create a new plan afterward, which may involve taking supplements. Thorne’s newest launch in this area includes a new gut health test with its patent-pending Microbiome wipe.

New Studies: One of the benefits of Thorne is that it has a heavy R&D focus, which allows it to stand out among the crowded nutraceutical space. A new study by Mayo Clinic focused on how its SynaQuell drug could impact neurological functioning in ice hockey players. SynaQuell is a supplement for brain health that was specifically designed for athletes that play high-contact sports.

New At Home Blood Test: Thorne also recently launched a new at-home blood sampling device, which earned a CE Market Certification in the European Union. Thorne will likely be able to sell this device in other countries like Japan in the future. Future Markets projects that the home blood testing market will grow by 10.8%/annum through 2033.

Strong DTC Growth

The company’s net revenue grew by 20.7% YoY last quarter, which was largely driven by growth from DTC (direct-to-consumer sales). This growth is very favorable, given that the U.S. dietary supplement market only grew by 1.7%. Thorne’s higher end, diversified portfolio, coupled with its investment in R&D, has allowed it to outperform the industry growth average.

Thorne Q1 Report

Amazon heavily dominates the market and accounts for a large % of vitamin and supplement sales for most companies. Amazon currently has a 37.8% market share in ecommerce. However, Thorne has been able to rely on its website/UX design to attract customers, which has supported its margins.

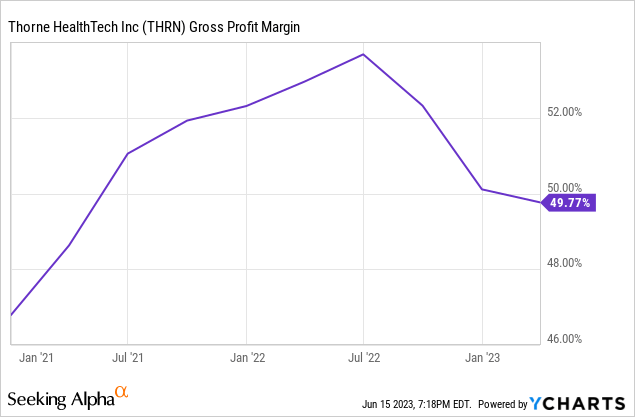

Its DTC channel has also helped to support its margins, as its gross margin has remained around 50% in the past three years. Supplements companies can have a GPM of 20-50%, so this % is favorable.

Top Areas to Focus On

Thorne has over 180 supplements on their website, which can be used for a wide variety of health issues. Three of the most popular supplements in the United States include multivitamins, Vitamin D supplements, and Omega-3 supplements. Thorne sells basic supplements, as well as more advanced products that may combine popular types of products.

Nutraceuticals for Sleep: Sleep supplements sales declined by 4% in 2022, after having much more rapid growth in 2020 and 2021. However, there is still strong long-term growth in this area. Around 27% of adults take melatonin as a sleep aid. Furthermore, they may rely on other supplements, like magnesium supplements, to improve their sleep. Thorne sells lower-end products like melatonin supplements ($13), as well as more expensive products like GABA supplements (around $60).

Cognitive Products: Many consumers are also taking supplements to help sharpen their cognitive functioning or to reduce stress and anxiety. Grandview Research projects that the brain supplements market will have a CAGR of 13.3% through 2030.

Bone/Joint Health: Some of Thorne’s top-selling supplements include bone and joint supplements. WebMD notes that supplements like glucosamine, chondroitin, and Omega-3 can help with arthritis and joint pain. One notable product Thorne sells includes its joint bundle supplement, which has glucosamine, chondroitin, curcumin, and omega-3 fish oil.

Gut Health: Nutraceutical consumers are also increasingly purchasing supplements, such as probiotics or collagen, to improve their gut health. The gut health supplement market is projected to grow at around 8%/year through 2030.

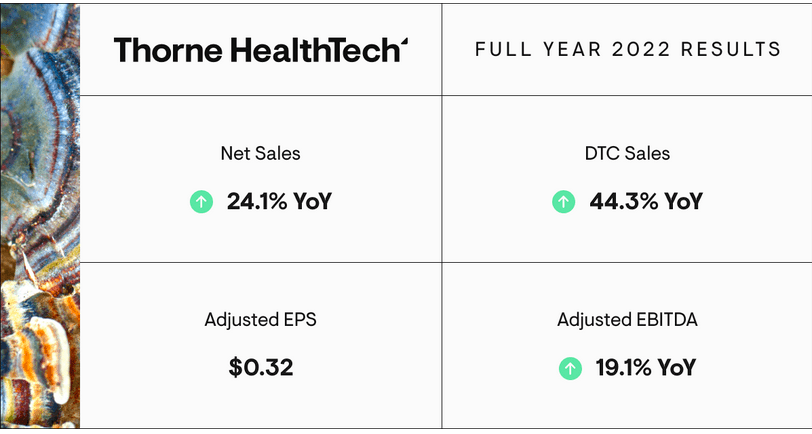

Favorable 2022 Performance

Even though the industry growth rate was much slower in 2022, following rapid growth in the two previous years, Thorne still had strong revenue growth. The Nutrition Business Journal noted that the growth of supplement sales in the United States was only 1.7% in 2022. However, it looks like the industry outlook may improve in the coming years, and return towards the historical highs of 2020 and 2021.

Yahoo Finance

The main driver of growth has been the strong performance of its direct-to-consumer, which outpaced overall revenue growth by around 20 percentage points.

Thorne

Thorne has also boosted its marketing and R&D expenditure, which has supported its revenue growth in 2022. Marketing as a % of total sales still fell from 12.4% in 2021 to 11.6% in 2022.

Thorne

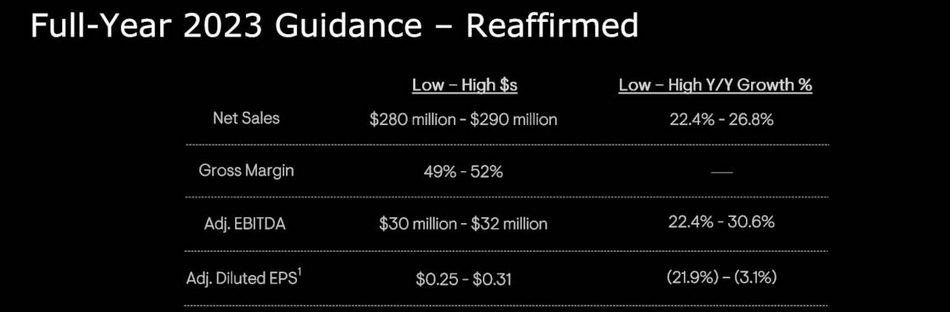

Thorne’s management projects that its revenue growth will exceed 20% again this year, and that it will still maintain a favorable GPM of around 50%. Thorne has a very strong position in the United States and can also expand in other global markets, where the supplements market is rapidly growing.

Thorne

I think that shares are a good buy in the $4-5 range and that positive performance in 2023 could lift its share price as high as $8/share. Shares have rallied significantly YTD following positive 2022 performance.

If Thorne hits the lower end of its EBITDA target, then shares would also be cheap on an EBITDA basis. Healthcare companies can typically trade as high as 19x EBITDA. Shares would trade at around $5.70/share if this multiple were applied to Thorne’s potential 2023 EBITDA of $30 million.

I think that Thorne can continue to stand out from the market for the following reasons:

1) Thorne takes a very scientific approach to its product marketing and developing its product. The supplements market is somewhat crowded, as there are around 1,440 supplements companies in the United States. However, it can be hard to verify some of the claims of all these products, and consumers may be more likely to trust larger and established brands. Thorne’s use of clinical research can allow it to stand out from the pack.

2) Thorne does not have to heavily rely on Amazon or other parties to sell its products. The company’s website has a user-friendly design, and customers can search tests and supplements and make an informed choice. This approach has also allowed the company to have above average margins.

3) Thorne is continually seeking new sources of growth, through both product launches and global expansion. Its products are currently sold in around 37 different countries.

I think the most significant risk with this stock is that it may be vulnerable to short-term pullbacks in 2023 due to weak industry and/or macro data. Price-sensitive consumers may begin switching to cheaper products this year. However, Thorne appears positioned to continue outpacing industry growth due to its new product launches and innovation. Because of this, I have Thorne listed as a hold. The share price has rallied YTD already, so there may be a better entry point below $4 this year.

Read the full article here