Introduction

In our previous article in April this year, we wrote a bullish article on Vector Group Ltd. (NYSE:VGR) based on its solid fundamentals, such as stable dividends and growing EPS. Since that publication, VGR stock has gained 2.04% and registered a total return of 3.65%. In this analysis, I will provide an update on this stock, especially on the most important pillars of the bull case in our previous analysis: dividend and earnings growth.

In addition, I will also mention the company’s asset utilization given its debt risk, which will also form the basis of my conclusion. In this analysis, I maintain the solid role the company’s business model and high institutional ownership discussed in the previous analysis may play in the company’s long-term success. An updated risk section will also form part of my analysis as well as a valuation section.

Earnings Growth

Most investors pay close attention to firms that show signs of remarkable profit growth, making earnings growth a crucial consideration. For growth investors, nothing is more desirable than earnings growth in the double digits, as this is usually taken as a sign that the company has promising future prospects (and stock price rises).

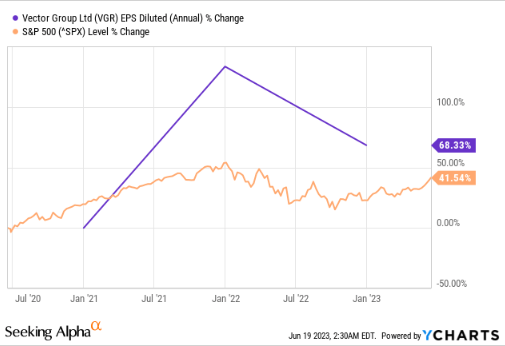

Even though Vector’s EPS has grown by 68.33% in the past three years, outpacing the S&P500, prospective buyers should pay more attention to how much it is expected to grow in the future.

YCharts

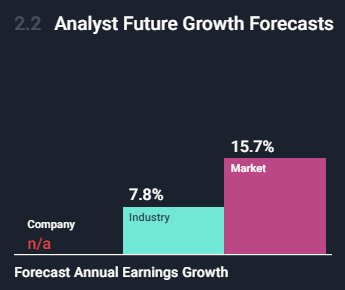

Despite the solid EPS growth over the last three years, since 2022, the company’s earnings seem to be on a downward trajectory, and this explains why the company is forecasted to experience no EPS growth in the future despite the industry’s forecasted to have earnings growth of 7.8%.

Wallstreet

I believe the current economic climate and the instability of the tobacco sector in the wake of recent legislative changes in the United States are to blame for this alarming trend in profitability. Besides these legislations enacted by the Biden administration, there have been tremendous reforms in the legal framework surrounding tobacco usage and litigation. In my opinion, these dynamics are causing a lot of uncertainty in this industry and in the most recent legislations by Biden’s government necessitating large CapEx in order to develop low nicotine products, which in my view, will eat into the profitably of companies like VGR who have relied on a cheap pricing strategy as a competitive advantage.

The Dividend Situation

On June 29th, shareholders of VGR will receive a $0.20 dividend payment. Based on this payout, the dividend yield will be 6.3%, which is about average for this industry. Checking the payout’s long-term viability is good because investors value dividend stability. Prior to the announcement of the new dividend payment, Vector Group had a dividend payout ratio of 78% of earnings but just 59% of free cash flows. I am confident that the dividend will be sustainable moving forward, especially with so much cash left over for reinvestment, as cash flows are more essential than earnings in the long run.

When thinking about dividends, it’s crucial to consider sustainability and volatility. The corporation has reduced its dividend payment at least once in the past decade, despite its long history of dividend payments. The annual dividend payment has decreased from $1.08 to $0.80 since 2013. There was a decline in the dividend of about 3% every year at that time. I am not interested in investing in a firm that cuts its dividend payments over time, as this volatility translates to unreliability.

While the dividend wasn’t reduced this year, I don’t think the stock is a good dividend investment. The company has strong cash flow, which may allow it to keep the dividend for the foreseeable future, but its track record is not encouraging. Given its history of volatility, I do not believe this stock has the potential to be a suitable income investment. More investors will be interested in a company if it has a stable dividend policy rather than one that fluctuates frequently.

Risks

Like any other investment, putting money into VGR is not without risks. Some of the major risks of investing here are as follows:

- Regulatory risks: Globally, tobacco companies have to follow many rules, such as taxes, limits on promotion, packaging rules, and bans on smoking. If these rules change, like if taxes go up or advertising rules get tighter, it could hurt Vector Group Limited’s profits and market share.

- Capital structure risk: VGR’s $1.4B in debt is 71% of its market cap of $1.95B, exposing the company to leverage risk. Increased interest payments, less financial flexibility, and problems satisfying debt obligations are all possible outcomes of carrying a large amount of debt.

- ESG risks: Factors related to the environment, society, and governance [ESG] are gaining traction among investors. VGR has ESG risks due to its role in the tobacco industry, including ethical concerns, negative societal repercussions, and the possibility of being excluded from sustainable investment portfolios.

- Economic and market risks: VGR performance is influenced by general economic conditions, consumer spending patterns, and stock market fluctuations. A weak economy can lead to reduced discretionary spending on tobacco products, affecting the company’s revenue and profitability. Changes in interest rates and market sentiment can also impact the company’s stock price.

Valuation

With a PE ratio of 12.24x against the industry median of 22.83x and an overall valuation grade of “A” from Seeking Alpha, this company seems to be trading at a discount. However, looking at the risks section and the weakening fundamentals, such as the declining EPS growth and the company’s dividend policy volatility, I believe this could be a value trap, although at the current valuation metrics, the company offers an attractive entry point. I think it is important to interrogate the company’s multiples before cashing in.

Given this background, then I believe the current inflationary environment and what I think too much-needed adaptability and investment to catch up with the new regulations in the US, this company may experience some financial constraints in the future, which I think will limit its upside potential. Much as its asset utilization is promising with an S/TA ratio of 1.5, I think it will take time if the company embarks on big investments in response to the dynamic legal framework to replicate the output of the deployed assets in its financials.

Conclusion

In conclusion, the business environment of VGR is becoming very tough both in the economic and legal spheres. These adversities are affecting the company’s fundamentals negatively, which in my view, pose a strong downside potential than upside. As a result, I believe the current valuation could be a value trap; therefore, investors should interrogate the company’s fundamentals before cashing in. From where I stand, I rate the company as a hold until the uncertainties in the business environment and the company’s fundamentals start improving.

Read the full article here