Calavo Growers, Inc. (NASDAQ:CVGW) may grow due to the international growth of the avocado market. In addition, further investments in capacity, headcount growth, and recent reorganization could bring future FCF growth. Even considering that 2023 appears to be a challenging year for Calavo, both management and market analysts appear quite optimistic about the future. Yes, there are risks from supply chain issues, changing preferences from consumers, or concentration from clients, however I believe that Calavo appears quite undervalued.

Calavo Growers

Managing to supply its distribution channels through plantations in Mexico and California, Calavo Growers is a company dedicated to the packaging and sale of agricultural products, mainly avocado and papaya, as well as other types of food supplies such as sandwiches, salads, and snacks among others. Its products are distributed locally in the United States, and are also exported to the international market.

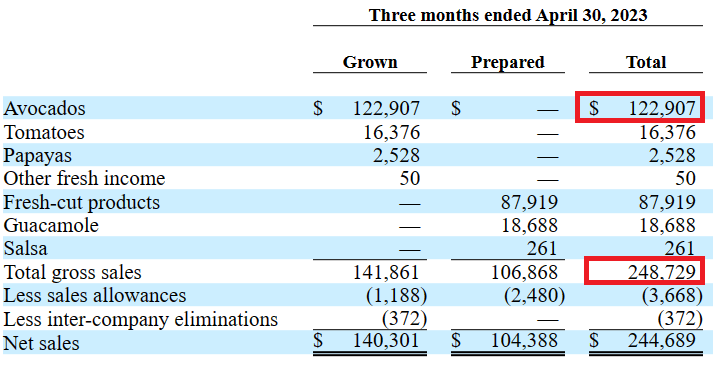

Distribution also includes prepared avocado-based products, which are delivered to retail markets, large markets, fresh and health food stores, and other distributors in regional markets. It is worth mentioning that Calavo Growers obtains net sales mainly from the sale of avocados, which represented close to 50% in Q1 2023, and fresh-cut products.

Source: 10-Q

Recently, the company decided to reorganize its business model into two new segments: preparations and sowing. The planting segment includes avocados, papayas, and tomatoes, which are purchased from the plantation agricultural regions and then distributed to the local and international markets. Within the prepared segment are those products that are made from the named foods, such as guacamole, packaged salads, sauces, and sandwiches.

The avocado is available throughout the year, with some peaks during the seasons of high temperatures, and the duration, once the harvest is done, is between one and three weeks depending on the maturation of the product. To conserve the products, Calavo has a high-cost conservation infrastructure, and plans with the producers to coordinate the harvests and subsequent distribution. Regarding this segment, the company distinguishes two keys that are its added value: the maturation of its products, for immediate distribution and consumption, and the packaging in bags that, according to its studies, increase the possibility of sales in stores directly to the public.

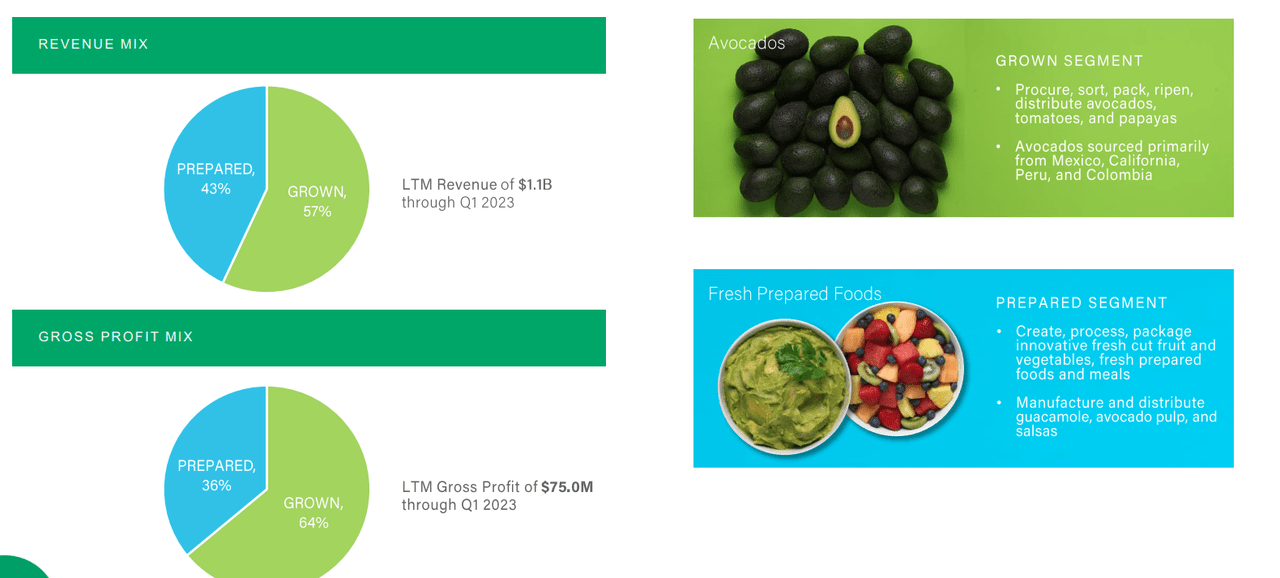

On the other hand, the prepared segment, with a current position of smaller scale, has production plants in Mexico, where the company preserves and packages the guacamole with vacuum sealing technologies. These products are distributed under the Garden Highway Fresh Cut, Garden Highway, and Garden Highway Chef Essentials brands. The following slides show information about the two segments.

Source: Investor Presentation

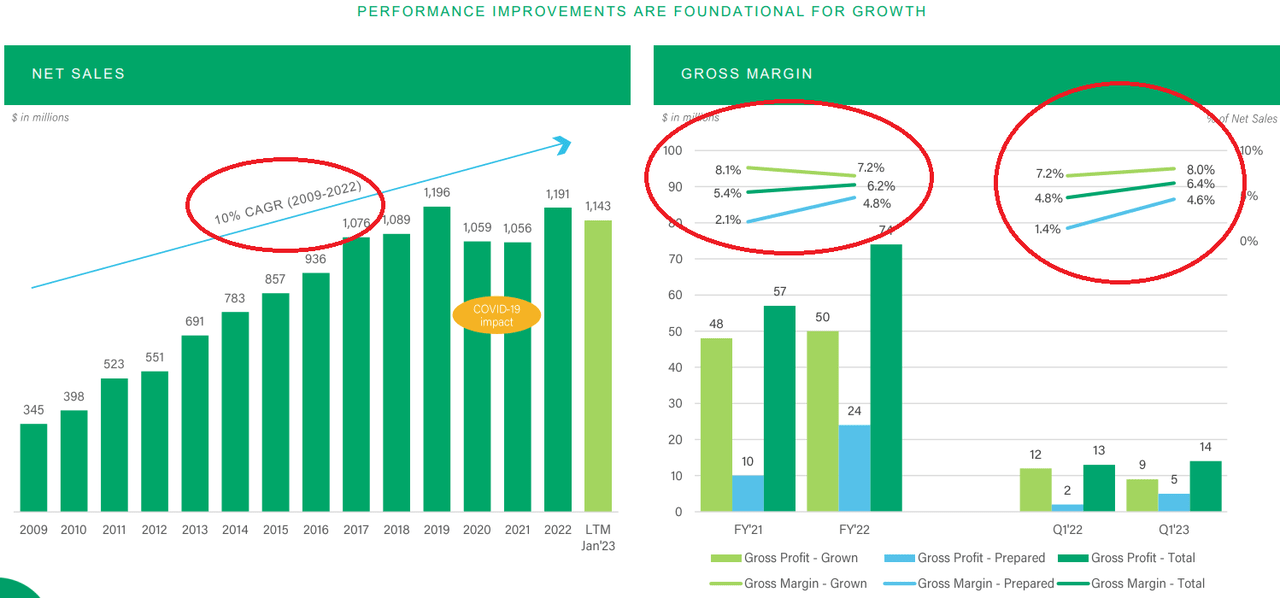

I believe that the selection of the avocado as the main product was smart. In the last decades, the company enjoyed double digit growth as well as gross margin growth mainly driven by headcount growth, acquisitions, and increase in the properties and equipment. I usually do not look at the past to judge the future, but with those figures, we can say that Calavo found some product and a business model that appears a bit unique. I do not see why the business model will not enjoy certain traction in the coming years.

Source: Investor Presentation

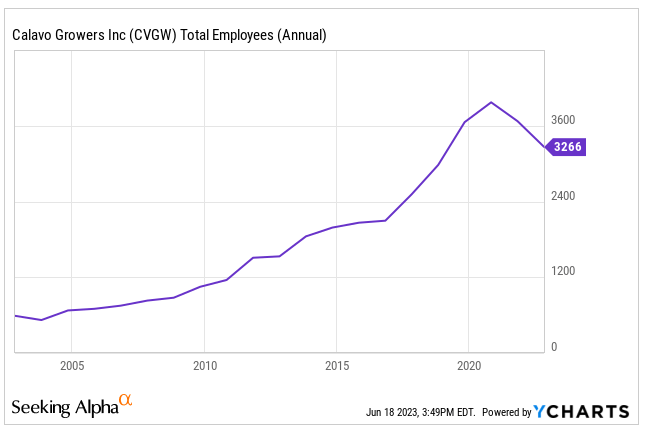

If you believe that a company is only successful when more and more employees are willing to work for the organization, you may want to have a look at the following charts. Since 2005, the number of employees has not stopped growing.

Source: 10-k Source: Ycharts

Despite The Guidance In 2023 Does Not Seem That Promising, There Are Beneficial Expectations For 2024 And 2025

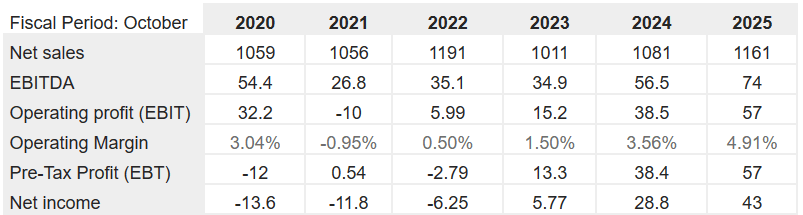

I believe that investors may want to have a look at the expectations of other financial advisors as they are quite beneficial. Other analysts expect 2025 net sales close to $1.161 billion, 2025 EBITDA of about $74 million, operating margin close to 4.91%, and 2025 net income of about $43 million.

Considering the current valuation, if the market price does not change, and the share count stays the same, the EV/2025 EBITDA would not be far from 10x-11x EBITDA. Yes, in my view, there is a certain undervaluation.

Source: Marketscreener.com

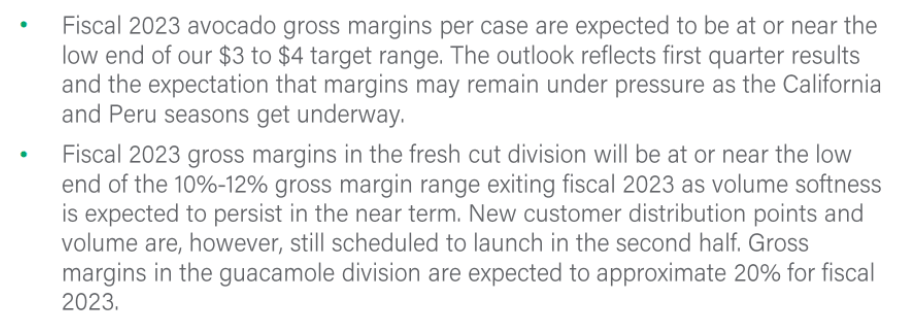

I believe that management is not optimistic about the results for the year 2023 because of the pressure in the margins in California and Peru. With that, it is expecting to launch new customer distribution points, which may increase volume. Besides, the company believes that the guacamole division could bring close to 20% gross margin for fiscal year 2023.

Source: Investor Presentation

Balance Sheet

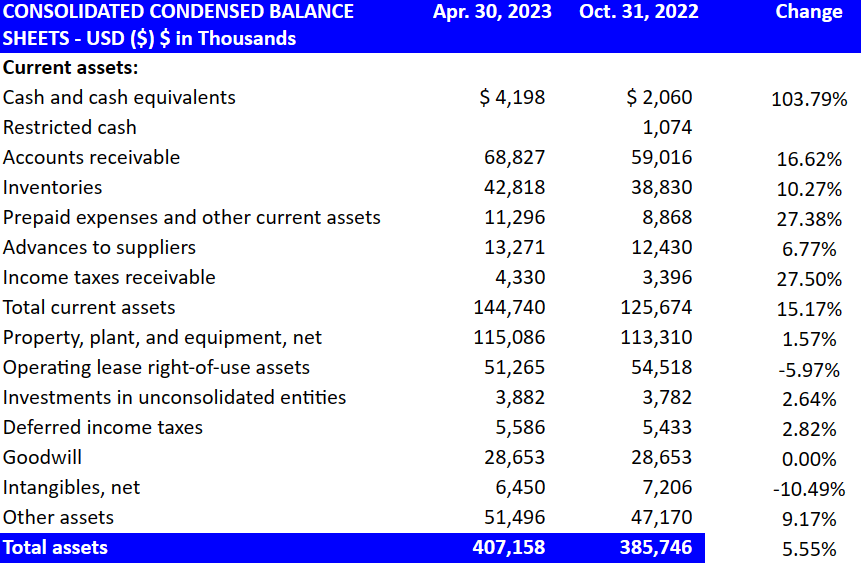

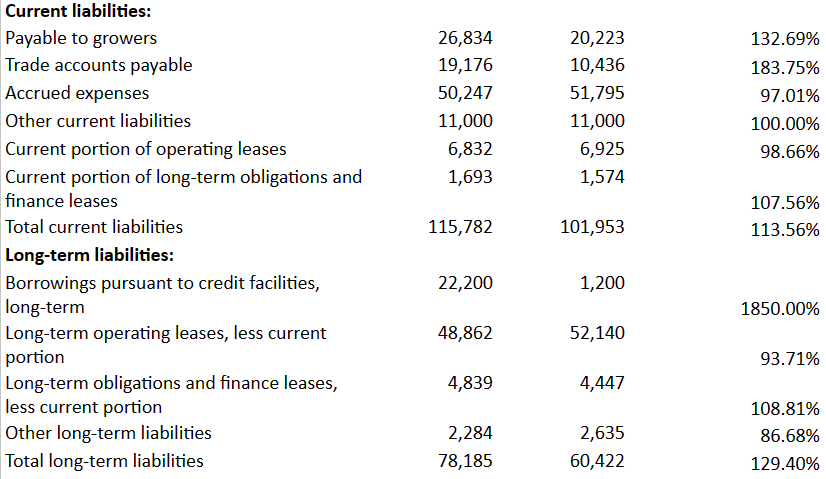

I believe that the most recent quarterly report was beneficial. Calavo Growers reported a significant increase in cash, accounts receivable, inventories, prepaid expenses, and total current assets. Total assets increased by more than 4%, and the asset/liability ratio stood at close to 2x. I believe that the financial situation improved.

More in particular, Calavo Growers reported cash and cash equivalents worth $4 million, accounts receivable of $68 million, inventories of about $42 million, and prepaid expenses and other current assets close to $11 million. Also, with property, plant, and equipment worth $115 million, non-current assets also included operating lease right-of-use assets of about $51 million, investments in unconsolidated entities worth $3 million, goodwill stood at $28 million. Total assets were equal to $407 million.

Source: 10-Q

The most interesting thing about Calavo Growers is that management does seem to need a lot of debt to run its operations. Providers and clients appear to support the operations of the company. In the last quarterly report, Calavo reported payable to growers worth $26 million, trade accounts payable close to $19 million, accrued expenses of $50 million, and current portion of operating leases of $6 million. Besides, the current portion of long-term obligations and finance leases was equal to $1 million.

Borrowings pursuant to credit facilities, long-term stood at $22 million, with long-term operating leases worth $48 million and long-term obligations and finance leases. In sum, total long-term liabilities stood at $78 million.

Source: 10-Q

My DCF Model Implied Significant Upside Potential

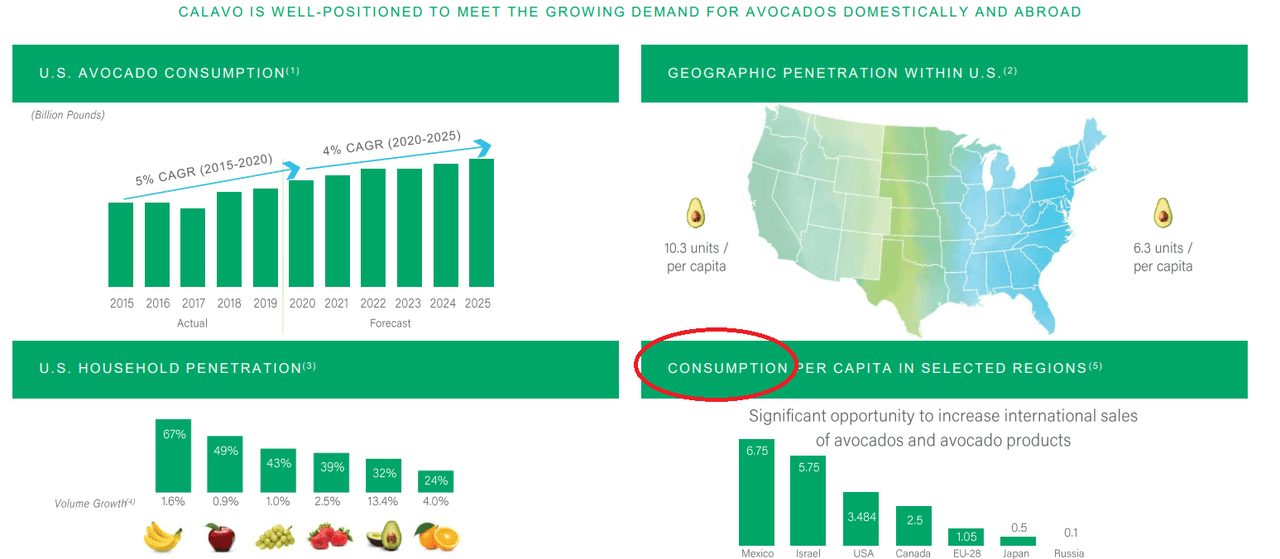

Under my DCF model, I assumed that Calavo Growers will successfully grow at close to the growth pace expected for the avocado market. In the United States, avocado consumption is expected to reach 4% CAGR from 2020 to 2025, however I believe that international efforts in Canada, Europe, or even Japan could bring significant organic growth.

Source: Investor Presentation

With that about the growing markets in which Calavo Growers operates, it is worth noting that management is optimistic about the future. Even though the year 2023 may be a complicated year, in my view, ongoing changes could bring significant benefits. In the last quarterly report, management noted that it pursues grower recruitment opportunities.

Source: Investor Presentation

We believe that cash flows from operations, the available Credit Facility, and other sources will be sufficient to satisfy our future capital expenditures, grower recruitment efforts, working capital and other financing requirements for at least the next twelve months. We will continue to pursue grower recruitment opportunities and expand relationships with retail and/or foodservice customers to fuel growth in each of our business segments. Source: 10-Q

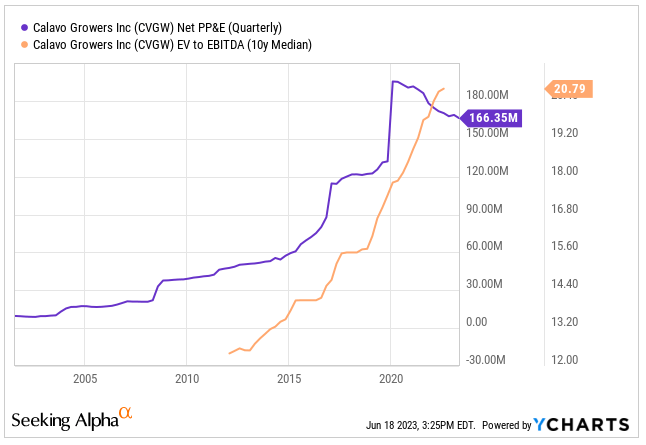

I think that further investments in infrastructure in order to provide better quality service to its customers as well as to be able to offer its products without interruptions throughout the year will bring further FCF generation. In my view, economies of scale will most likely play a major role in the future of Calavo. In my view, investors will most likely be ready to pay a bit more EV/EBITDA multiples as the property and equipment grow north.

Source: Ycharts

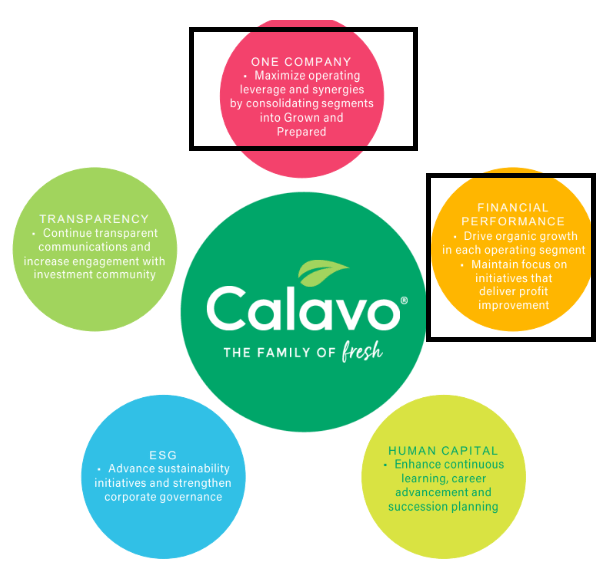

I also believe that Calavo Growers will most likely benefit in the coming years from further consolidation in the growth, prepared business segments, operating synergies, and operating leverage that smaller peers may not obtain. I also think that further efforts to focus on initiatives to grow inorganically and profit improvement will most likely bring FCF growth. I am not thinking out of the box here. Some of these initiatives were noted in a recent presentation to investors.

Source: Investor Presentation

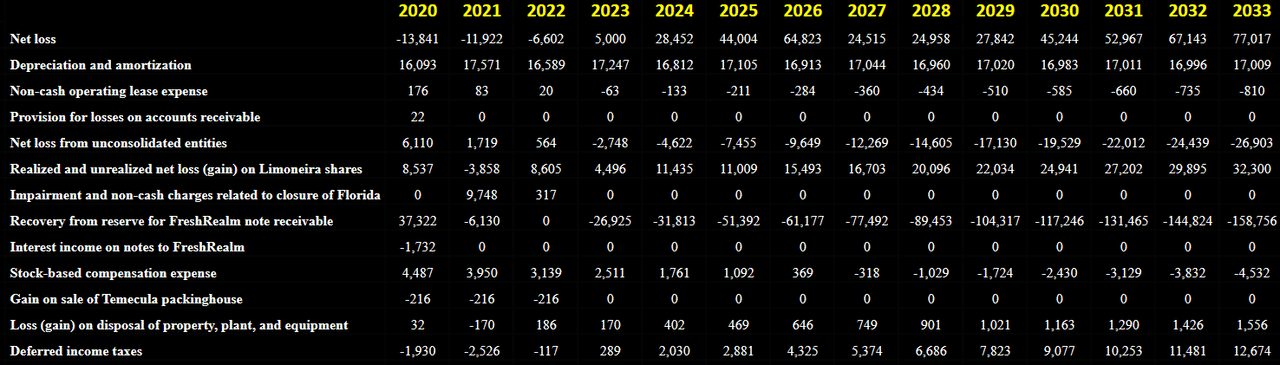

Under very conservative assumptions, I included 2033 net income close to $77 million, 2033 depreciation and amortization of about $17 million, 2033 recovery from reserve for FreshRealm note receivable close to -$159 million, and 2033 stock-based compensation expenses worth -$5 million.

Source: My Financial Model

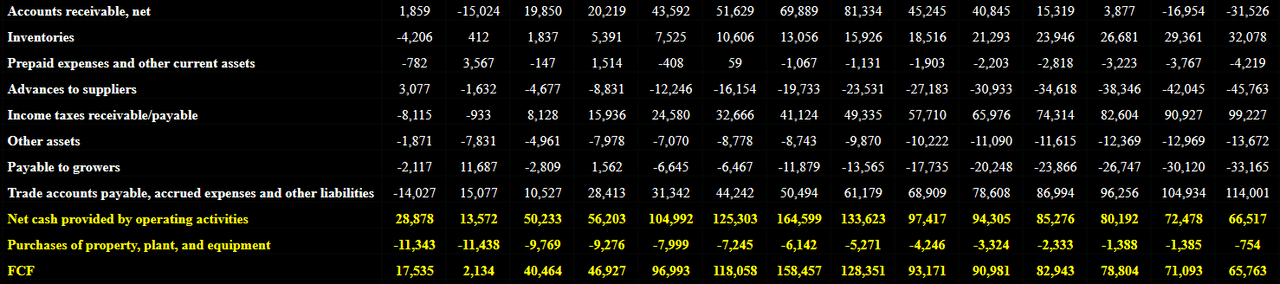

Also, with 2033 deferred income taxes worth $12 million, 2033 accounts receivable of -$32 million, 2033 inventories close to $32 million, and prepaid expenses and other current assets of close to -$5 million, I also assumed advances to suppliers of -$46 million.

Finally, with payable to growers of about -$34 million and 2033 trade accounts payable, accrued expenses and other liabilities of close to $114 million, net cash provided by operating activities would be $66 million, and 2033 FCF would be $65 million.

Source: My Financial Model

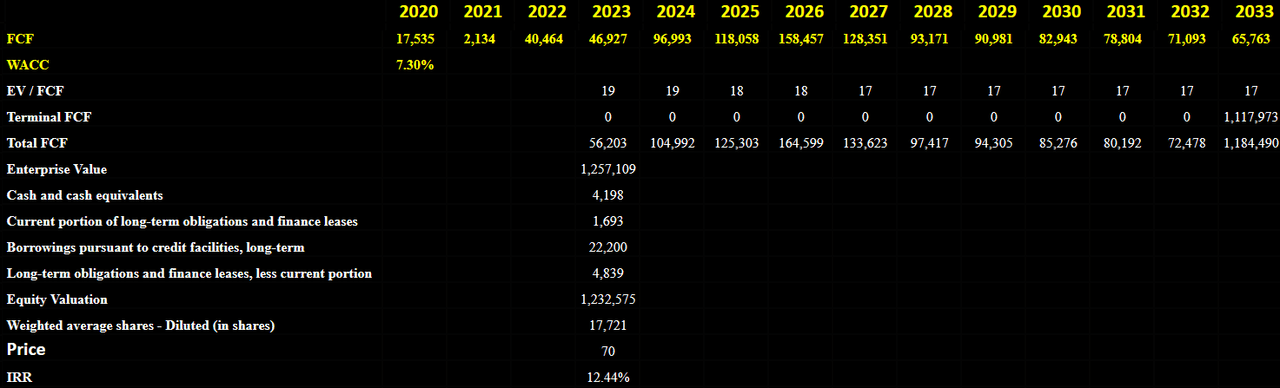

If we assume a WACC of 7.3% and an EV/FCF of 17x, the implied enterprise value would be close to $1.257 billion. If we add cash and cash equivalents of $4 million, and subtract current portion of long-term obligations and finance leases close to $1 million, borrowings pursuant to credit facilities of $22 million, and long-term obligations and finance leases close to $4 million, the implied equity valuation would be $1.232 billion. Finally, the implied fair price would be $70 per share.

Source: My Financial Model

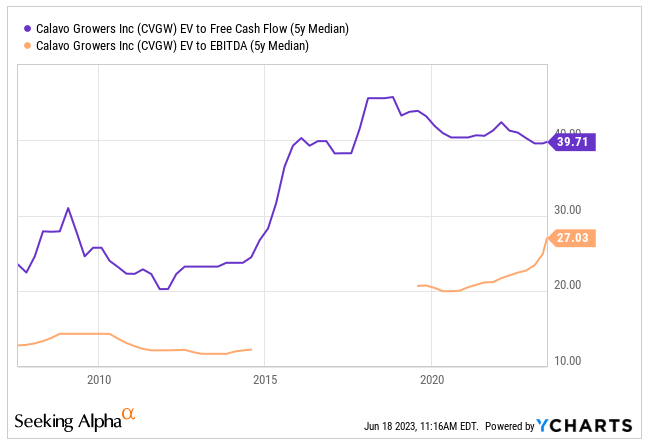

I took a look at the EV/FCF and EV/EBITDA multiples to assess my terminal EV/FCF multiple. I believe that I was very conservative. In the past, Calavo reported an EV/5 Years median FCF of close to 20x-39x and EV/EBITDA of about 27x.

Source: Ycharts

Competitors And Clients

The avocado distribution market is highly competitive, both locally and internationally. At the local level, the main competitors in the distribution of these products are companies dedicated to similar purposes, with a business model that is dedicated exclusively to the distribution of the fruits and not to their cultivation and production.

Calavo appears to be the top distributor and the company with the highest performance in both sales and profits. The prepared food segment, on the other hand, has a large number of competitors, among which we find historical brands as well as emerging brands dedicated to the supply of fresh prepared foods.

With that about peers, I believe that we may find more information about the partners and clients that work with Calavo. In the last quarterly report, the company noted massive blue-chip customers like Amazon (AMZN) and Starbucks (SBUX). If these large companies collaborate with Calavo, I believe that we can say that the operations of the company are top-notch.

Source: Investor Presentation

Risks

The first risk to highlight is the lack of diversification in sales revenue currently registered by Calavo. In the last 10-k, almost 40% of the revenue reported is concentrated in its three main clients: Walmart (WMT), Kroger (KR), and Trader-Joes. A change in the strategic decisions of these consumers could seriously affect the current model of the company. As a result, we could see a significant decline in sales and stock price declines.

In addition to the instabilities of the global economy and the possible problems regarding the continuity of supply chains as well as the increase in transport prices, we can add the regulations for trade and business activity in the countries where Calavo Growers is present. Mainly, Calavo sustains its activities through a good relationship with its suppliers and its customers. Besides, any new legislation that affects the relationship with hourly paid employees in avocado and tomato plantations could generate inconveniences in the supplement of products for future distribution.

Finally, I believe that a change in consumer preferences or inability to react to new trends in the food market could bring lower net sales than expected. If Calavo fails to offer the net sales expected by the market, I believe that shareholders may sell their stakes, which may lead to price volatility and declines in the market valuation.

My Takeaway

Calavo Growers benefits from the growing avocado market in the United States and internationally. With large clients and partners, I believe that the company appears well positioned for further capacity growth and headcount growth. In my view, further synergies obtained from the recent reorganization of business segments could bring new FCF that most analysts may not be expecting. Even considering the challenging 2023, I think that the changes announced by management, optimism about the future, and expectations from market analysts are sufficient reasons to follow the stock. Yes, there are risks out there from concentration of clients, changing consumer preferences, or global recession. With that, in my view, future FCF would imply a higher valuation than the current stock price.

Read the full article here