As the bear market has ended and future fundamentals indicate that the current bull run is likely to continue, it is time to look for ETFs such as the Communication Services Select Sector SPDR® Fund ETF (NYSEARCA:XLC) that have the best chance of capitalizing on the uptrend and outperforming the market. Other compelling reasons to consider XLC include slowing inflation, the Fed’s potential soft landing, and solid earnings growth. Furthermore, despite a year-to-date gain of more than 30%, the communication services sector appears undervalued relative to the broader market index and trades at a significant discount to other high beta sectors such as technology and consumer cyclical.

Extreme Greed and Historical Trends Hints at Solid Bullish Trend

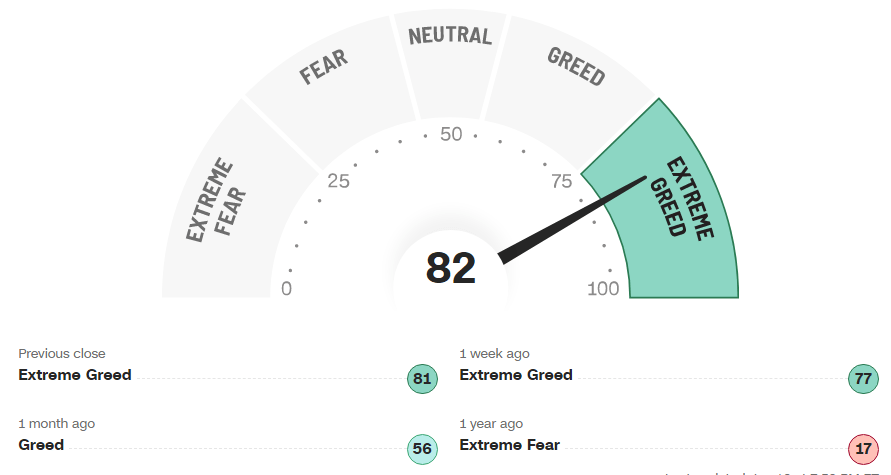

Fear & Greed Index (CNN)

Before delving into why XLC might be the best option, let us first assess how the equity market is likely to behave in the second half of 2023 and the following year. The S&P 500 is now in a bull market, with the broader market index up more than 20% from its October lows, thanks to strong gains from mega and large-cap stocks in the cyclical technology, communication, and consumer cyclical sectors. Given the extreme levels of investor greed for the US stock market, there is a good chance that the bull run will continue in the second half.

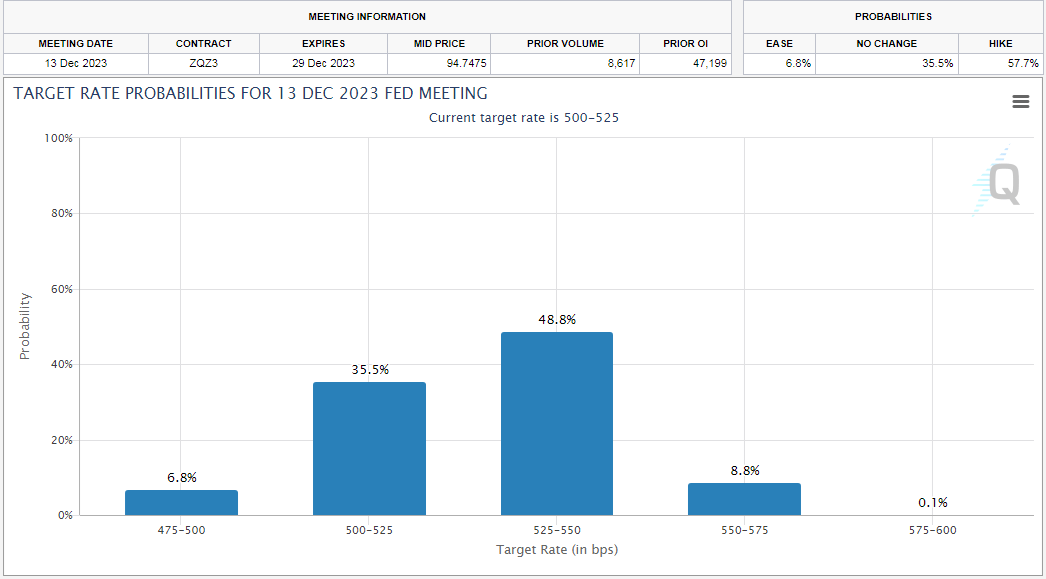

Rate Hike Expectations (CME FedWatch Tool)

In addition to investor sentiment, the fundamental elements support the uptrend. For instance, interest rate traders now expect only one rate hike in the second half and a cut at the beginning of the following year. Furthermore, it appears that the Fed has successfully been achieving its goal of reducing inflation without severely depressing the economy. In May, inflation dropped to its lowest point in two years, and unemployment hit a record-low level dating back to 1969. Market experts from Goldman Sachs anticipate that there is no danger of economic collapse with such a robust job market. All of this suggests that the Fed will most likely have a soft landing, which would be ideal for the equity market and growth stocks in particular.

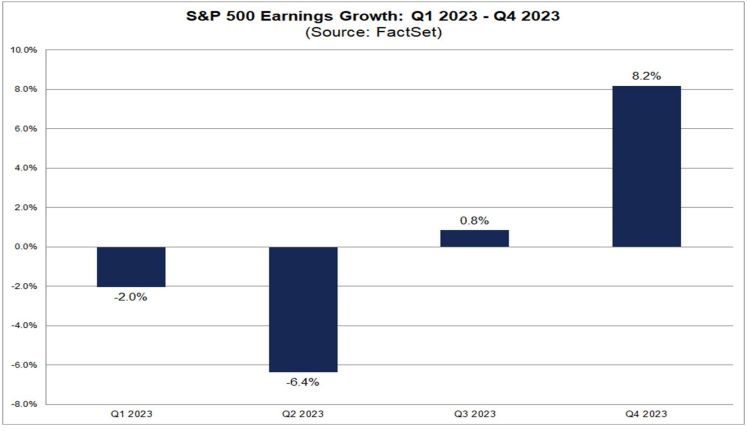

FY2023 quarterly Earnings Expectations (FactSet)

Furthermore, there is no doubt that the economy’s underlying strength has begun to show in corporate performance. In the first quarter, the S&P 500’s earnings growth was negative 2% year over year, contrary to initial predictions of a decline in the mid-single digits. Wall Street expects a solid earnings recovery in the second half, with fourth-quarter growth in the high single-digit percentage. For the full year, the S&P 500 is now anticipated to experience positive growth in the low single-digit percentage range compared to initial expectations for negative earnings.

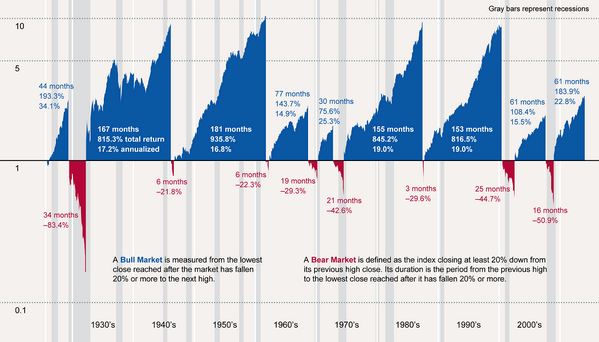

Bull and Bear Market History (RBC Global Asset Management)

Historical stock market behavior is another factor that boosts confidence in the continuation of a bull market. There have been numerous bear markets and downtrends of more than 20% throughout history. However, as shown in the above chart, bearish trends are shorter in duration and intensity than bull markets. The chart also shows that the stock market has the potential to gain more than 100% after a bear market and that a bull market usually lasts significantly longer than a bear market. The most recent bear market began in early 2022. However, after hitting lows in October, the S&P 500 began to recover, and the recovery rate accelerated in the first half of 2023. With gains of more than 20% since the October low, we have officially exited the bear market and entered the bull market. Although historical data cannot predict actual future returns, it can be used to forecast how markets will behave in general. Therefore, if the market follows its historical pattern, a long bull run is likely.

Why Is XLC a Solid ETF to Capitalize on the Bull Run?

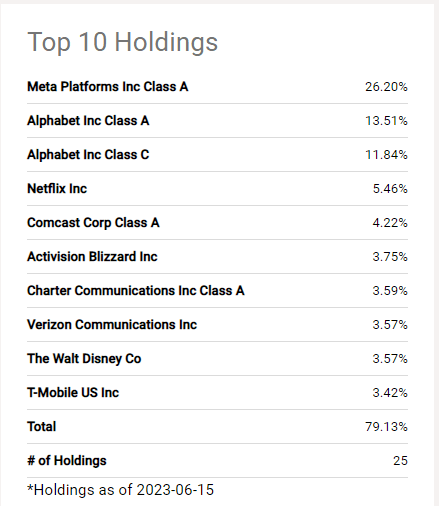

XLC Holding Breakdown (Seeking Alpha)

As I anticipate a bull market in the second half and beyond, it is critical to choose the ideal stock or ETF in accordance with one’s investment goals and risk tolerance. I think the best option for investors looking to fully benefit from the bull run and reduce the risk involved with a single stock investment would be XLC, which tracks the performance of the communication services select sector index. It has the highest liquidity of its peer group, which I discussed in detail in the quant rating section, as well as a low expense ratio of 0.10%.

With a high beta of 1.14, XLC has the potential to outperform the broad market index when the market is bullish. XLC has produced a price return of 33% so far in 2023, which is almost twice as much as the S&P 500’s gain of over 15%. XLC’s portfolio also appears solid with a collection of well-established 25 large-cap companies engaged in modern communication and information delivery services. It includes well-known FANG names like Facebook parent company Meta (META), Alphabet (GOOG) (GOOGL), Netflix (NFLX), The Walt Disney Company (DIS), Activision Blizzard (ATVI), and Verizon Communications (VZ), as well as a slew of other major entertainment and telecommunications firms.

FY 2023 Earnings Expectations (FactSet)

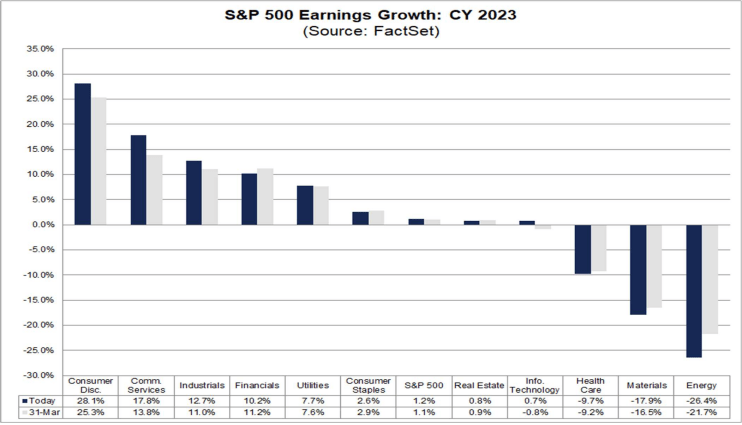

One of the main factors influencing share price growth has always been earnings growth. In the case of XLC and the communications sector, the positive financial outlook fully supports the increase in share price. For instance, despite FactSet data indicating that the S&P 500 is likely to experience a mid-single-digit percentage earnings decline in Q2 earnings, the communication services sector is likely to outperform trends with 12% earnings growth. This is due to the strong performance from across the sector and especially from the largest names like Meta and Alphabet, which collectively account for around 50% of XLC’s portfolio. The data also shows that the entire communication services sector is likely to experience a robust growth trend in the second half of 2023 with Q4 earnings growth expectations of 36%. Wall Street expects the communication services sector to experience 17% earnings growth in fiscal 2023, the second fastest among S&P 500 sectors. Earnings growth of 18% for 2024 also indicates that earnings support for share price upside will continue in the following year.

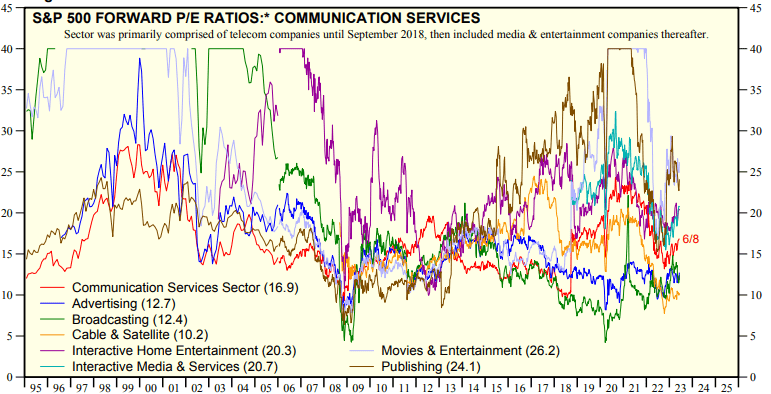

Communication Services Sector Forward PE Ratio (Yardeni.com)

In addition, compared to the broad market index and other high-growth industries like technology and consumer cyclical, the communication services sector is currently trading at a significant discount. For example, its shares are currently trading at 16.9 times forward earnings, compared to 18.5 times and 25.6 times forward earnings for the S&P 500 and tech sector, respectively. Although 2022’s selloff helped to lower the forward price-to-earnings ratio in the communication services sector, the strong earnings forecast also significantly contributed to lowering the forward valuations. The drop in the forward price-to-earnings ratio due to robust earnings growth increases the room for potential upside in my view.

Quant Rating

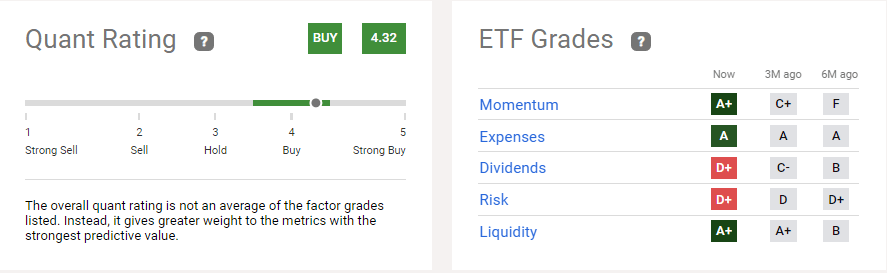

XLC Quant Rating (Seeking Alpha)

XLC earned a buy rating with a quant score of 4.32 due to a high score on momentum, expenses, and liquidity factors. Momentum is a technical indicator that assists investors in predicting potential price movement. Stocks or ETFs with high momentum scores are thought to extend the uptrend. XLC also appears to be a solid ETF due to its high grade on liquidity factor, owing to its large assets under management and high trading volume in comparison to peers. High liquidity reflects investor interest and confidence in the ETF. The ETF received an A rating for its expense ratio of 0.10%, which is significantly lower than the average expense ratio for all ETFs of 0.49%. The only ETF with a slightly lower expense ratio than XLC is Fidelity® MSCI Communication Services Index ETF (FCOM), but it lags XLC in terms of momentum and liquidity. Overall, according to quant ratings, the Communication Services Select Sector SPDR® Fund ETF ranked first among peers due to its strong momentum and liquidity score.

Risk Factors to Consider

Although investing in XLC reduces the number of risks associated with a single stock investment, the ETF still carries a number of risks, including the possibility of tail events. The main risk to the XLC and communications sectors seems to be the Fed’s rate hike policy. The communication sector may experience volatility if the Fed raises rates more frequently in the second half compared to expectations for one hike and a cut at the start of 2023. This is because the sector is cyclical and its performance is dependent on macroeconomic conditions. A hard landing by the Fed could have a negative impact on the financial growth of communication service companies.

In Conclusion

The Communication Services Select Sector SPDR Fund ETF appears to be a solid ETF for capitalizing on the bull run. The high beta, low valuations, and strong earnings growth of XLC’s portfolio holdings increase its ability to produce impressive returns over the coming quarters. It also qualifies as a strong ETF to hold over the long term due to its low expense ratio and high liquidity.

Read the full article here