Thesis

This article examines the financial performance of ReNew Energy (NASDAQ:RNW) in the context of the renewable energy market, highlighting positive indicators such as strong EV/EBITDA and Price/Cash Flow metrics. However, concerns arise from future cash flow projections and high EV/Sales ratios. The company’s capital structure analysis reveals significant leverage, posing potential risks in the face of rising interest rates. While ReNew Energy showcases resilience and growth potential, risks and headwinds in various operational aspects warrant cautious optimism.

Company Overview

ReNew Energy Global Plc is a UK-based firm, incorporated in 2011, that has made its mark in India with a strong focus on harnessing non-traditional, eco-friendly energy sources. They’ve neatly divided their operations into two main segments: Wind Power and Solar Power. Adding to their core operations, they’ve ventured into ancillary services including engineering, procurement, and construction, operations and maintenance, as well as consultancy services. As of March 31, 2022, their portfolio boasted an impressive total of 10.69 GW across wind, solar, hydro, and firm power projects, as well as distributed solar energy projects. Of this, 7.57 GW were already commissioned and 3.12 GW were pledged

Expectations

Currently, RNW is covered by seven Wall Street analysts with an average “Strong Buy” rating on the stock that projects a healthy 45%+ upside potential for its stock price.

Seeking Alpha

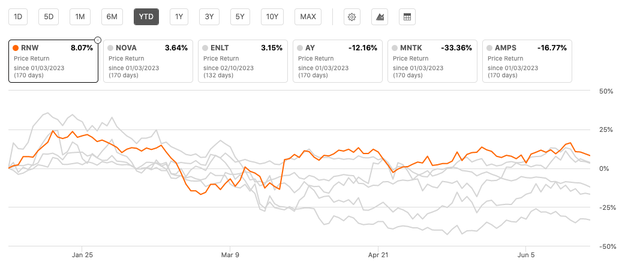

Performance

Relative its peers, RNW is the current front runner with reference to it YTD price performance that boasts a modest 8.07% positive return.

Seeking Alpha

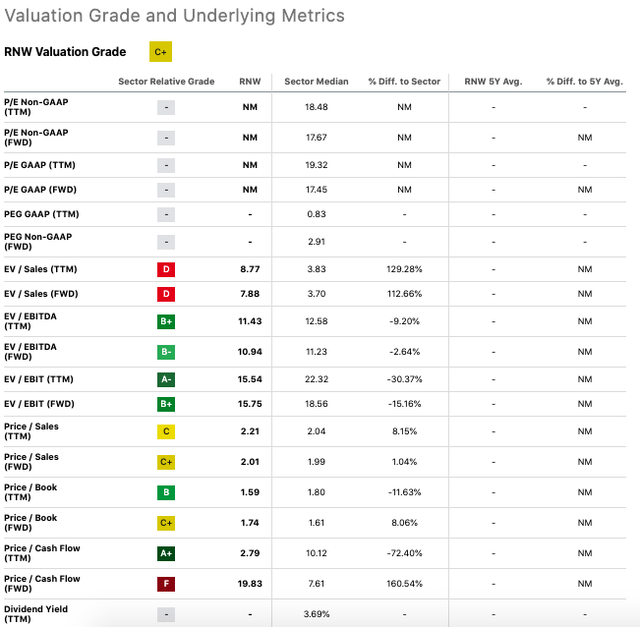

Valuation

Let’s begin with the positives, RNW is performing relatively well in EV/EBITDA, EV/EBIT, Price/Book, and Price/Cash Flow metrics on a trailing twelve months basis (see table below). In fact, I’m particularly impressed with RNW’s Price/Cash Flow (TTM) which gets an A+ grade, indicating the company is effectively managing its cash flow.

Seeking Alpha

However, I’m equally concerned with the company’s forward Price/Cash Flow which earns a concerning F grade. This paints a picture of a potential squeeze on future cash flows, a major red flag for me. Another troubling sign is RNW’s high EV/Sales ratios, both on a TTM and forward basis. With RNW’s EV/Sales (TTM) ratio over 129% above the sector median, it appears the market has factored in a lot of growth expectations for RNW. And yet, we’re missing data on P/E, PEG, and dividend yield, which could provide a more rounded view of the company’s growth (more on that below in “Risks & Headwinds) and income prospects.

Seeking Alpha

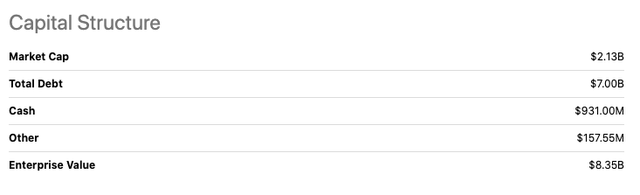

And finally, capital structure analysis has shown that RNW is heavily leveraged, with a debt load of $7.00B against an estimated market cap of $2.13B. This level of leverage could put its financial stability in jeopardy should interest rates rise or cash flows become unstable.

Q4 2023 Bullish Earnings Takeaways

With the Indian government escalating its renewable energy auctions threefold to a staggering 50 GW annually from FY ’24 onwards, the renewable energy market is on the cusp of a major expansion. The government’s focus seems to be shifting towards more complex and wind auction segments, niches where ReNew Energy holds a robust competitive edge. This surge in auctions coupled with an inclination towards intricate projects is poised to provide ReNew Energy with an avalanche of market opportunities.

The Power of Strategic Alliances

On another front, ReNew has strategically chosen to partner with Gentari, the renewable energy arm of Petronas. This joint venture is projected to amplify ReNew’s stronghold and enhance its project execution capabilities. The move not only reaffirms ReNew’s foresight in securing financial underpinning for its expansion blueprint but also is a testament to its aggressive growth strategy.

Financial Resilience Amidst Debt Crisis

In an environment beleaguered by formidable debt hurdles, ReNew’s financial prowess was highlighted when it successfully refinanced over $1 billion in maturing debt and managed to slash its interest expenses. Adding to its financial triumphs, it has trimmed its DSOs (Days Sales Outstanding) to a respectable 138 days as of March 31, thanks to initiatives such as the Late Payment Surcharge.

Robust Portfolio and Revenue Growth

The past fiscal year was marked by a substantial 28% Y-o-Y growth in ReNew’s portfolio, reaching an impressive 13.7 GW. This growth was mirrored in the company’s total income for FY ’23, which swelled by 29% from $912 million to a commendable $1.1 billion.

Demonstration of Solid Financial Performance

Despite some turbulence due to wind resource availability and carbon credit sales, the company’s adjusted EBITDA climbed by a robust 12.4%. This evidences ReNew’s efficiency in handling its central operations, despite external challenges.

Cash Flow Optimization

ReNew’s concerted collection efforts seem to be paying dividends, as indicated by an impressive near-50% improvement in DSOs year-over-year, which has resulted in better cash flow management.

Positive EBITDA Projections

Even with cautious assumptions for FY ’24, ReNew is forecasting an adjusted EBITDA range of INR 60 billion to INR 66 billion. Moreover, they’re optimistic about a 35% growth by FY ’25 which casts a promising light on the company’s future growth prospects.

Promising Share Buyback Program

And finally, ReNew’s ongoing share buyback program, accounting for 30% of their free float, underscores their confidence in their stock as a high-yield investment.

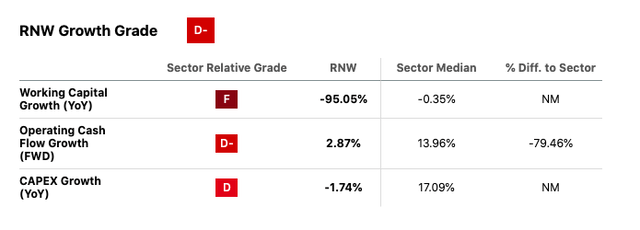

Risks & Headwinds

Seeking Alpha

First off, the company’s negative EPS revisions are an immediate red flag. This is a classic indicator of potential future stock underperformance. Even more troubling is RNW’s declining growth when compared to other Utilities stocks. The data (see above) is clear as day – it earns a D- grade, which is frankly disturbing. This is far below the sector median, indicating that RNW’s peers are substantially outpacing it. Also, the second alarm bell is ringing loud and clear in RNW’s Working Capital Growth, which is showing a year-on-year decline of a staggering -95.05%.

In the realm of renewable energy, the Indian government’s robust support stands out, setting a favorable environment for companies like ReNew. However, ReNew finds itself navigating a sea of uncertainties with shifts in policy and regulatory frameworks acting as turbulent waves. Such unpredictability in the regulatory climate introduces considerable risks to ReNew’s operational framework and future growth curve.

Furthermore, ReNew finds itself dependent on Power Purchase Agreements (PPAs), where a significant slice of the company’s projected revenue rests on securing these agreements. The rhythm of this momentum can be disrupted by delays or failures in sealing these PPAs, and any missteps could strike a harsh blow to the company’s financial well-being. Also, while ReNew’s manufacturing facility is poised to kickstart production, looming over it are the shadows of supply chain risks. Notably, the sourcing of solar modules in India presents a major challenge, potentially throwing a spanner in the works of the company’s production plans.

Moreover, although its core business currently boasts a healthy EBITDA margin of approximately 80.3%, overall EBITDA margin has seen a decrease since previous periods, due to accounting for transmission projects. Such a downward spiral might set off alarm bells with investors who might view this development as an early warning signal.

Finally, projecting into FY ’23, there’s an anticipated decline in cash flow to equity, signifying an increased burden of debt on the company’s financial structure. This could set off warning signals for shareholders, hinting at potential risks should debt levels spiral out of control.

Final Takeaway

Given ReNew’s robust past performance and promising future growth prospects, especially within the burgeoning renewable energy sector in India, I believe a “Hold” rating is warranted. However, its high debt burden, concerning cash flow metrics, and a myriad of execution risks highlight the need for cautious optimism.

Read the full article here