Investment thesis

Our current investment thesis is:

- Mattel (NASDAQ:MAT) has a strong competitive position but growth is a serious issue.

- Toys are less interesting to consumers due to technology, but that does not mean opportunities are lacking. Mattel could improve its course by improving direct selling to customers and expanding further overseas.

- The Barbie movie represents the potential for a Super Mario-like impact for Mattel.

- Margins are taking a big hit, which is concerning in the short term.

Company description

Mattel, Inc. is a global children’s and family entertainment company that specializes in designing and manufacturing toys and consumer products.

The company operates through three segments: North America, International, and American Girl. Their extensive product lineup includes dolls, accessories, gaming products, and lifestyle items under popular brands like Barbie, Monster High, American Girl, Disney Princess, Frozen, Fisher-Price, Hot Wheel, Matchbox, and Polly Pocket.

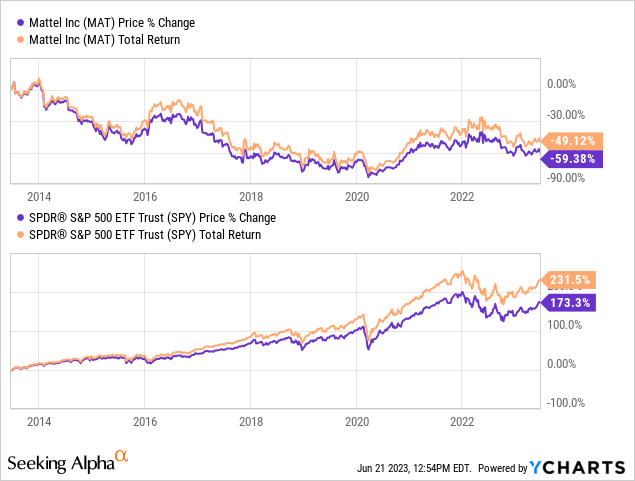

Share price

Mattel’s share price has noticeably struggled in the last decade, declining over 50% while the S&P 500 has soared. This is primarily due to fundamental shifts in the industry as toys become less desirable, contributing to reduced demand and continued tough competition.

Financial analysis

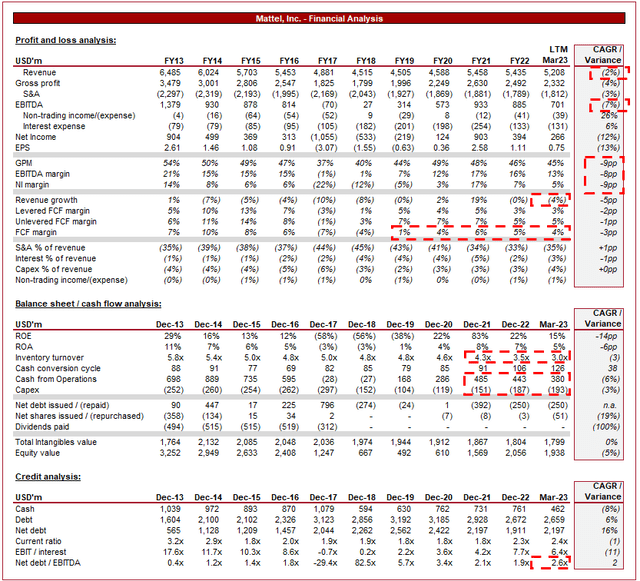

Mattel Financials (Tikr Terminal)

Presented above is Mattel’s financial performance for the last decade.

Revenue & Commercial Factors

Mattel has experienced a revenue decline in the last decade, achieving an annualized rate of (2)%. During this period, Mattel experienced 7 fiscal years of negative growth, illustrating that this decline is a fundamental issue rather than a short period of underperformance.

Business model

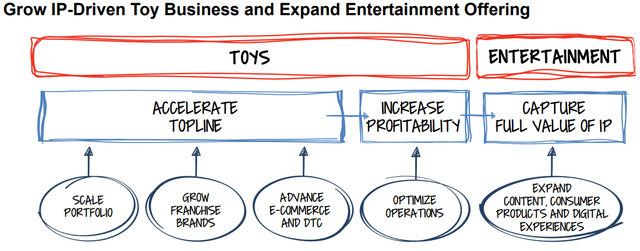

Mattel is a leading toy company, focused on creating new and innovative toys under its global franchises. Increasingly, the company is focused on entertainment IP-led growth through new franchise partnerships in areas of consumer interest. Examples of this include its partnership with Disney, Minecraft, and the Jurassic World Franchise. This is in response to slowing interest in some of its brands, and changing industry dynamics contributing to reduced consumer exposure to Mattel’s brands.

Mattel’s key area of differentiation are, firstly, the company’s strong catalog of children’s and family entertainment franchises such as Barbie, American Girl, Disney Princess, Hot Wheels, and more. These franchises are among the leading toy brands globally. Secondly, Mattel’s size and expertise in the toy industry allow it to win new IP deals, expanding its product suite. Mattel aims to leverage the IP across various verticals, including content, consumer products, and digital experiences.

Looking ahead, the company’s strategy is to grow its IP-driven toy business and expand its entertainment offering. This is a logical development given the current position of the market, with the entertainment industry highly influential in the interests of children. This is essentially a circular model based on the strength of the IP.

Strategy (Mattel)

Toy industry

The digital revolution since the creation of the smartphone has materially impacted the toy industry. In just over a decade, the number of children entertained by things other than toys has skyrocketed, namely tablets/smartphones and TV. This is only going to continue, as businesses find improved ways of tailoring products to kids, such as YouTube Kids. The ability to combat this development is difficult, as the entertainment provided is leagues apart. A clear positive is that this does not render the toy industry obsolete, as technology is introduced after several years, and many parents continue to keep technology away from children for as long as possible.

Mattel’s response has been a logical expansion of the entertainment side of the business. Most recently, the company is expecting the launch of the highly-anticipated Barbie movie, as well as the recent launch of the Hot Wheels show. The expectation is that Mattel can expand its offering while also enhancing the value of these brands. The Barbie movie has an estimated budget of $100m, boasting Margot Robbie, Ryan Gosling, and Helen Mirren, among others. Interestingly, Will Ferrell is cast as the “Mattel CEO”, which could mean direct marketing for the business (and thus its website and wide range of brands). Regardless of Mattel’s fundamentals, we suspect this movie, alongside the TV show, will have a strong near-term impact on both share price and earnings. It is critical that this movie is a success, and could lead to a pipeline of further developments. Nintendo (OTCPK:NTDOY) is experiencing a similar thing following the success of its Super Mario movie ($100m budget, $1.3bn gross), with many now believing a future Zelda movie is now guaranteed.

Given the power technology now possesses, collaborations with popular franchises, movies, and TV shows have become increasingly important to drive future growth. IP owners usually sign exclusively with a toy manufacturer, pressuring Mattel to be attractive relative to Hasbro (HAS), among others. Thus far, we believe Mattel has a good suite of brands, but this is an unattractive aspect of the industry, as the business is pressured to maintain and win the leading brands.

Social media platforms and influencer marketing have become powerful tools for brand promotion and reaching target audiences. The historical avenue for marketing was TV but now, the likes of YouTube Kids and other methods are far more important. Given Mattel’s brand value, its products are regularly reviewed and thus promoted. This said, the return on marketing investment has been poor given the lack of sustainable growth, implying an improvement in this is required.

Various segments within the toy industry have seen changing levels of demand. Interest in educational and STEM-focused toys, for example, has increased. Parents are seeking toys that promote learning, creativity, and problem-solving skills, representing a personal development opportunity rather than just entertainment.

Despite the poor growth thus far, we do see areas of opportunity that could support improving growth in the coming years.

E-commerce and Direct-to-consumer represent a key opportunity for Mattel. Both are trends we have seen develop over the last few years across the retail industry, and Mattel has positioned itself to exploit this. The company has an online store stocking all of its brands, offering a one-stop-shop. The benefit to bringing sales in-house is that Mattel is able to cut out the middleman, improving margins.

Further, expansion into new markets, particularly emerging markets, represents an opportunity to expand its addressable market. With developing economies and a growing middle class, the demand for Western products, including toys, should inevitably rise. These regions are entertained by the same media as the West, allowing for brand development even if a structured toy offering has not yet been developed.

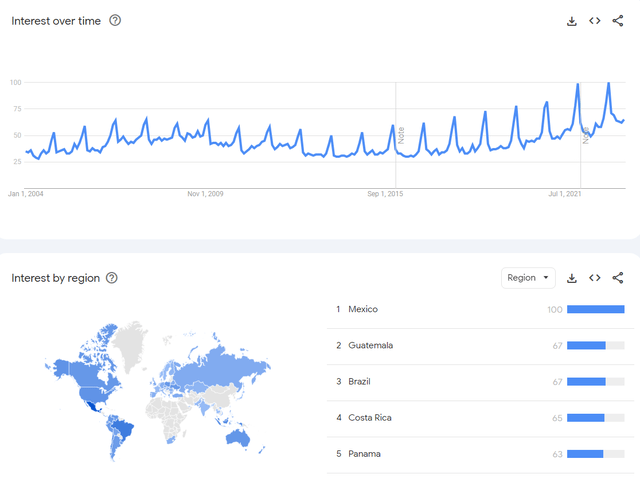

The following illustrates the interest in hot wheels over time. The brand experienced a consistent decline since 2009 before a reversal around 2015. Looking at the interest by region, the brand has materially shifted from the West. In the most recent quarter, YoY growth was positive only for vehicles, implying an above-average strength in this particular brand.

Hot Wheels (Google Trends)

Economic & External consideration

Current economic conditions represent a near-term headwind for the business. With consumers’ finances being squeezed by inflation and interest rates, we are seeing softening discretionary spending.

Sales in the most recent quarter are noticeably down, implying this is having a significant impact on Mattel. We expect current conditions to remain in the coming quarters, until expansionary policy can return. This implies a difficult FY23 is ahead, with the only hope for resilience placed on the impact of the Barbie movie in our opinion.

Margins

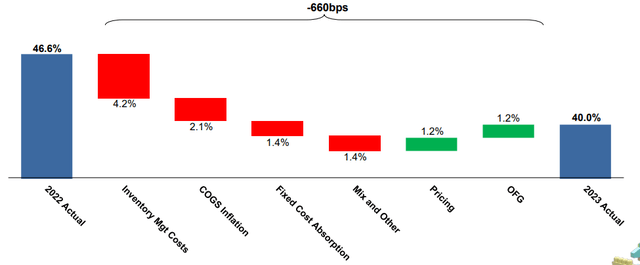

Mattel’s margins have been unusually volatile during the historical period, with the company currently having a GPM of 45%, EBITDA-M of 13%, and a NIM of 5%.

The recent margin deterioration is attributable to cost inflation, as Mattel has been unable to wholly pass this on to customers. In the most recent quarter, GPM declined 6.6%, with a positive pricing impact of 1.2%.

GPM bridge (Mattel)

We suspect there will be some margin improvement in the coming 18-24 months, as inflationary pressures subside, but the ability to win back all of its margins remains uncertain. This is due to the soft level of current growth, making aggressive pricing potentially detrimental to growth.

Balance sheet

Mattel’s inventory turnover has materially declined since December 2021, contributing to an accumulation of inventory that is being unwound, eroding margins. This is a reflection of poor management, although the depth of the decline in sales was likely difficult to foresee. We suspect this could lead to another quarter or two of poor margins.

Cash flow generation has been relatively steady despite the increased CCC in recent years. There is scope for further improvement here in line with inventory, implying cash flow upside.

Given the weak financial performance, material distributions to shareholders have ceased, which is a disappointing development given the reinvestment has not yielded improvement.

Mattel is moderately financed with a ND/EBITDA ratio of 2.6x. Given the variability in EBITDA and the near-term weakness ahead, we believe the company is likely at the maximum it should operate with.

Industry analysis

Industry (Tikr Terminal)

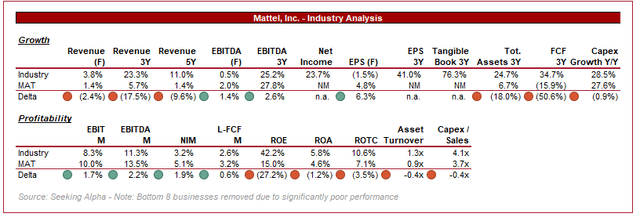

Presented above is a comparison of Mattel’s growth and profitability to the average of its industry (Leisure Products), as defined by Seeking Alpha (26 companies).

Mattel’s growth weakness is considered an underperformance relative to the industry, supporting the assertion that the toy industry is overly exposed to headwinds.

From a profitability perspective, however, Mattel looks quite attractive. Its margins are superior and have driven profitability improvement. This is significant given the margin erosion in recent years, implying improvement will significantly widen its strength.

This does imply a fundamentally strong business. The critical area of assessment is whether growth can return.

Valuation

Valuation (Tikr Terminal)

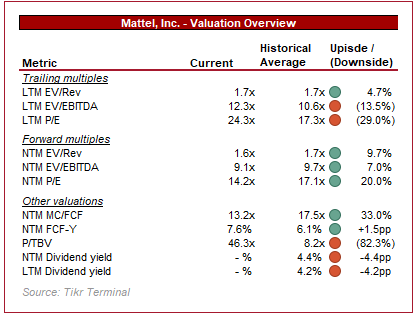

Mattel is currently trading at 12.3x LTM EBITDA and 9.1x NTM EBITDA. This implies some uncertainty in the market when pricing this asset. Given Mattel’s share price did not materially move following its Q1 results, we believe the NTM multiple is a better reflection of the company’s valuation, which implies a discount.

For most of the last 10 years, Mattel has struggled with volatile margins and declining revenue. For this reason, the historical average implicitly captures poor performance. This means, to assess the company’s relative position, the question to ask is whether the trajectory of the business has improved or decayed.

Our view is that Mattel remains in line with its prior performance. Growth is still in question and a positive margin trajectory has yet to be achieved. The potential for upside, which is unquantifiable, is the impact of the Barbie movie and Hot Wheels TV show.

Final thoughts

Mattel has a strong competitive position. It is one of a few businesses that have the scale, expertise, and market position to deliver leading IP toys. This insulates the business somewhat, as toys are not going away any time soon. This said, the ability to achieve consistent meaningful growth looks uncertain.

Margins are also a concern, although on a relative basis, are fairly attractive. We expect some improvement in the coming years.

With Mattel trading around its average historical multiple, we believe the company is fairly valued. We are highly anticipating the release of the Barbie movie, and what this could do to the stock.

Read the full article here