Intro

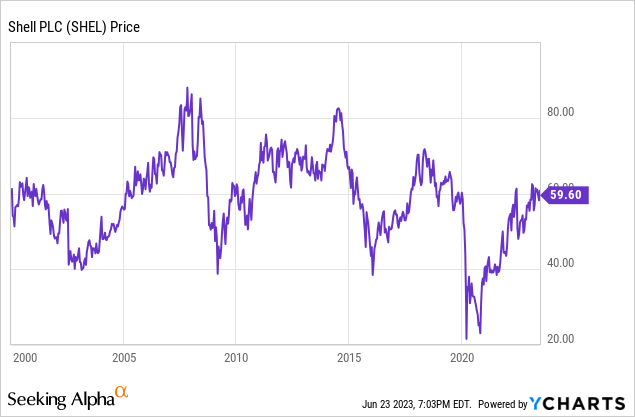

I have recently heard some bearish theses on Shell (NYSE:SHEL) echoed by a number of European investors. The arguments against Shell have included poor management, declining reserves, renewable energy, and a stock price that has gone nowhere for 20 years:

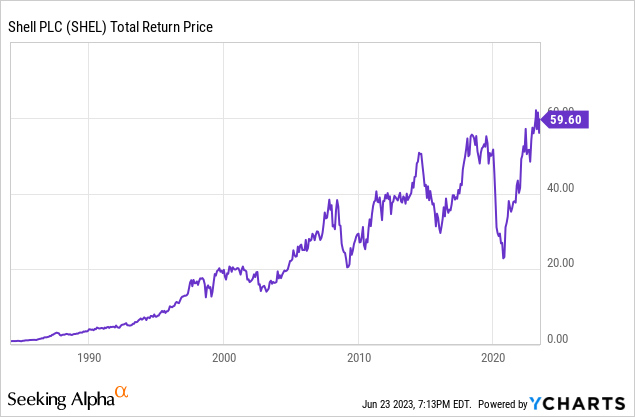

I believe these arguments are misguided. Shell now has ample oil reserves, management that is increasing dividends and buying back shares, a renewables business that shows real promise, and favorable economics that have led to total returns of 11% per annum (Compounded) since 1984:

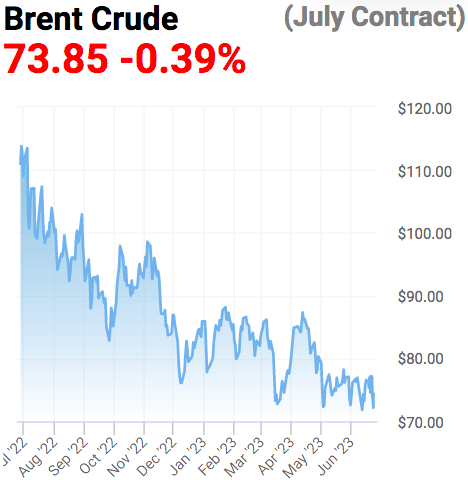

Still, oil prices are falling, and investors are likely wondering, should we be worried?

Brent Crude Price (OilPrice.com)

I think the answer is no.

Goodbye, Cyclicality?

Shell is increasingly moving away from being a cyclical commodity company. When you think of Shell, you should think of a diversified powerhouse in global energy. The company is now involved in LNG, oil & gas, chemicals, biofuels, EV charging, retail stores, carbon capture, green hydrogen, and electric utilities.

Even with high oil prices in 2022, Shell’s upstream oil segment accounted for only 39% of its earnings. When you combine Shell’s cost-advantaged upstream business with its robust integrated gas business and its array of other income streams, you get what looks like very dependable cash flows.

Shell’s integrated gas [LNG] business made $6 billion, $9 billion, and $22 billion in 2020, 2021, and 2022 respectively (Excluding impairments). I do not expect this rapid growth to continue; it is largely due to increased LNG demand in Europe due to a “slump in Russian pipeline imports.” However, you can see how consistently profitable Shell’s integrated gas business is.

Shell also has an upstream cost advantage in deepwater oil because of its position in the Gulf of Mexico and Brazil. Moreover, the company has been divesting its higher-cost oil assets. This gives Shell an exceptionally low break-even price of $30 per barrel Brent:

Break-Even Price Brent Crude (Shell Capital Markets Day 2023)

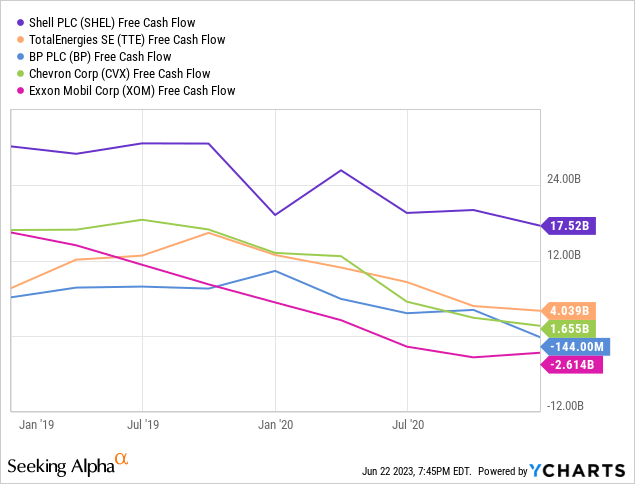

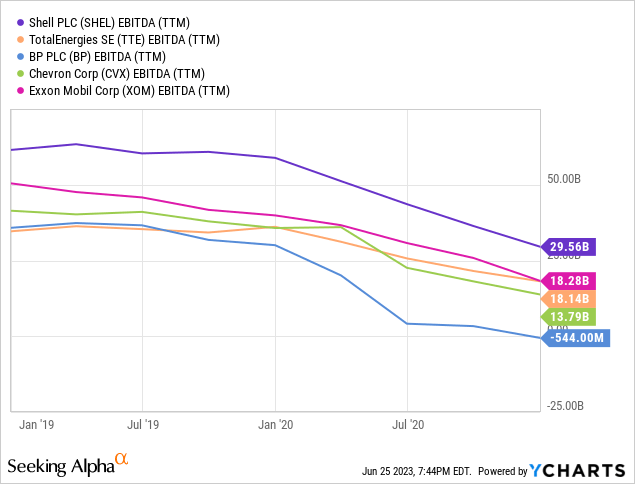

When the world appeared to be falling apart in 2020, and the likes of Exxon (XOM), Chevron (CVX), BP (BP), and TotalEnergies’ (TTE) free cash flows were on the brink, Shell was still minting cash to the tune of $17.5 billion:

Shell also maintained the highest EBITDA among peers in 2020:

Shell hasn’t eliminated cyclicality entirely, but it should now be in an even stronger position with Brent crude below $50 / barrel.

Normalized Earnings

By the way, I still think Shell’s normalized earnings power is around $21 billion, which is $6.20 per share on the current shares outstanding. $21 billion is also the company’s average free cash flow over 2019, 2020, and 2021. The price of Brent crude averaged $60 per barrel over this period.

European Pension Funds Should Buy

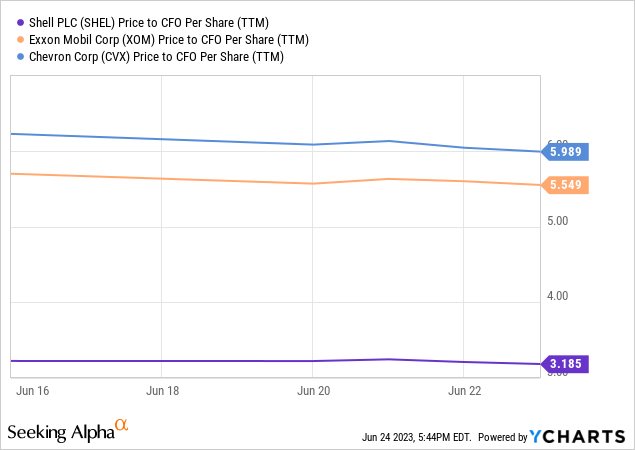

When you look at Shell’s ability to produce substantial free cash flow even at depressed oil prices, I think the company deserves a higher multiple. I don’t think it would be crazy for European pension funds to buy Shell at 15x normalized earnings; in fact, I think it would help these pension funds meet their obligations. European government bonds currently yield just 3.2%. 15x normalized earnings equates to $315 billion, representing 58% upside from the current market cap ($200 billion).

If Shell’s valuation were to re-rate closer to American peers Exxon and Chevron, you would get similar upside.

Price to operating cash flow:

The Hyper-Growth Of Renewables

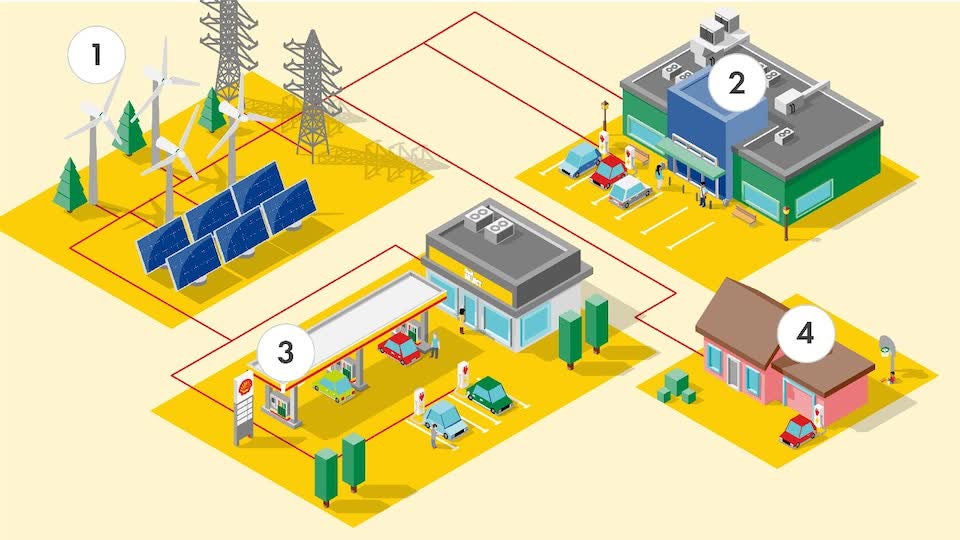

Shell is now a global leader in electric vehicle charging. With 150,000 EV charge points (30,000 of which are public), Shell’s public charging network is 2nd in the world, trailing only Tesla (TSLA), with 45,000 public chargers. And, Shell is planning to increase its EV charging capacity by 333% over the next three years.

Shell’s competitive advantage here is its world-leading network of gas stations. Shell reports having “more than 45,000 service stations in more than 90 countries.” The company can install new charge points at these locations. I expect this to dramatically improve the profitability of these stores because the average EV customer spends 2x that of the traditional customer. When you think about it, this makes a lot of sense; it takes longer to charge an EV than it takes to fill up on gasoline. Thus, you have more time to buy chips, soda, cigarettes, and/or food in Shell’s stores. Here’s a look at Shell’s EV charging ecosystem:

EV Charging Ecosystem (Shell)

Increasing sums of money are beginning to flow into Shell’s renewables segment. From 2021 to 2022, renewables and energy solutions revenue increased from $27 billion to $60 billion, a 120% increase; this hyper-growth was discussed in my last article on Shell. You can see that if revenue continues to grow at a rapid pace, Shell will only have to earn a thin margin in order to make billions of dollars from renewables.

Takeaways – Capital Markets Day 2023

On spending and costs, Shell seems to be taking a disciplined approach. To engender renewables growth and decarbonize, Shell plans to spend $10-15 billion on low-carbon energy solutions between now and 2025. Shell is lowering its overall CapEx guidance to $22-25 billion for 2024 and 2025. This should help boost free cash flow. Executives said this will force them to be disciplined with their capital allocation.

Shell has become a very shareholder-friendly company of late; the company plans to increase the Q2 dividend by 15%, buy back $5 billion of stock by year-end, and distribute 30-40% of operating cash flow year-in and year-out. Shell’s been buying back stock in mass, and I think this is being done at accretive prices:

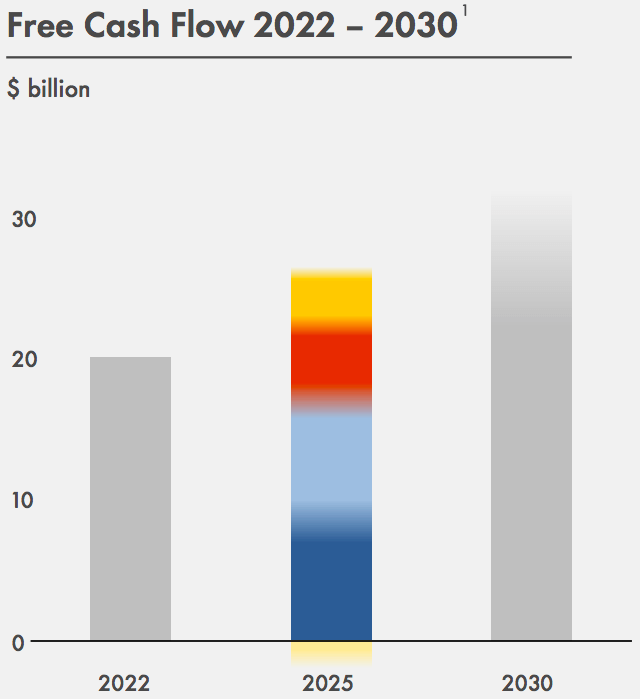

Shell also expects to make approximately $32 billion of normalized free cash flow in 2030:

Normalized Free Cash Flow Estimate (Shell Capital Markets Day 2023)

The company calculates this number using a starting Brent crude price of $65 that grows alongside inflation. To engender its growth, management plans to use prudent capital allocation and cost-cutting. At first glance, the company’s normalized FCF projection looks aggressive to me, but given what I now see in Shell’s renewables, LNG, break-even, and oil reserves, I am increasing my prior projections (Just not to the extent that Shell itself has).

Long-term Returns

In the decade ahead, I project total returns of 13% per annum for SHEL:

| Normalized EPS | $6.20 |

| Current Dividend | $2.64 |

| Compound Annual Growth Rate | 6% |

| Year 10 EPS | $11.10 |

| Terminal Multiple | 13x |

| Year 10 Price Target | $144 |

| Annualized Returns (Dividends Reinvested) | 13% |

This is a base-case estimate. The “compound annual growth rate” is for dividends and earnings.

Risks

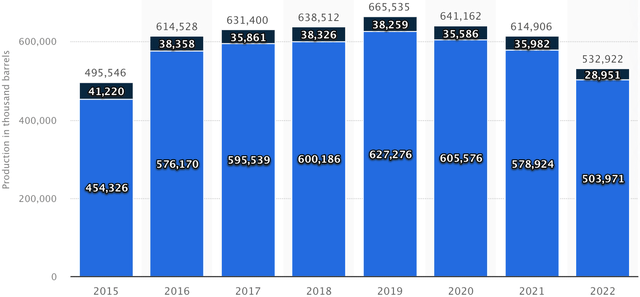

While Shell has an incredibly strong balance sheet, double A credit rating, and arguably $30 billion in excess cash, returns could still be lower than I expect due to management shortcomings and/or regulatory interference. For example, SA Analyst Acutel expects “that increased tax, legal and regulatory risks in Europe will weigh on the stock.” There are a lot of anti-energy and climate activists in Europe, and they have succeeded in getting Shell to reduce its emissions. As a result, Shell’s annual oil & gas production has fallen:

Shell’s Oil & Gas Production (Statista)

The company seems on track to meet its emissions targets and plans to hold production steady going forward. With 9.578 billion barrels of oil equivalent, Shell now has ample proven oil reserves, given how much annual production has dropped. And, these reserves are now beginning to grow again:

Shell Proven Reserves (BOE) (Statista)

As for the thesis on oil prices, Shell is in a good position. Still, if oil prices fell below $40 / barrel for an extended period of time, Shell may have to cut its dividend, representing volatility risk ($40 / barrel Brent is Shell’s dividend break-even). I think this is quite unlikely due to the power of OPEC.

The Bottom Line

Management’s recent growth projections for normalized free cash flow shocked me to the upside. I’ve factored in a range of outcomes, including the chance of increased regulation in Europe; still, I am upgrading my outlook for Shell’s growth prospects and expect returns of 13% per annum from here.

Reasons to be bullish include Shell’s low break-even price on deepwater oil, robust LNG business, 120% year-over-year growth in renewables, and low valuation. Therefore, Shell shareholders shouldn’t be deterred by oil fluctuations above $40 / barrel Brent. I maintain my “Strong Buy” rating on Shell.

For another “Strong Buy” energy company, take a look at my article “Petrobras (PBR): The Worst Has Been Avoided” here.

Until next time, happy investing!

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here