Investment thesis

In March 2023, I wrote an article about Flexsteel (NASDAQ:FLXS) as growing investor pessimism derived from inflationary pressures, supply chain issues, declining volumes, higher retail inventories, and growing concerns of a potential recession caused a price crash as the share price declined by 70% from all-time highs. Now, three months later, the share price has fallen by a further 2.36% while the S&P 500 has recovered some territory as it increased by 8.18%, which indicates that pessimism among investors is increasing even more regarding Flexsteel’s prospects.

After four quarters of sequential revenue declines, the company reported a 6.44% increase quarter over quarter during the third quarter of fiscal 2023 as growth initiatives are beginning to be reflected in the company’s results. Furthermore, the gross profit margin improved to almost 19% during the quarter, and the company keeps deleveraging its balance sheet. Even so, sales continue to be very depressed as they actually declined by 29.45% year over year during the quarter (despite sequential growth), and recessionary risks are keeping investors on the sidelines, which represents, in my opinion, a good opportunity for long-term dividend growth investors as the dividend appears safe thanks to a low cash payout ratio. Furthermore, the company periodically performs aggressive share buybacks, which means investors see their positions grow over time simply by holding the company’s shares.

A brief overview of the company

Flexsteel is one of the largest manufacturers, importers, and marketers of residential furniture products in the United States, and it was founded in 1893. Its market cap currently stands at $97 million as it employs over 600 workers in manufacturing facilities located in Dublin, U.S., and Juarez, Mexico, and 28.59% of the total number of shares outstanding are owned by insiders, which means the management is the main beneficiary of the good performance of the share price.

Flexsteel Industries logo (Flexsteel.com)

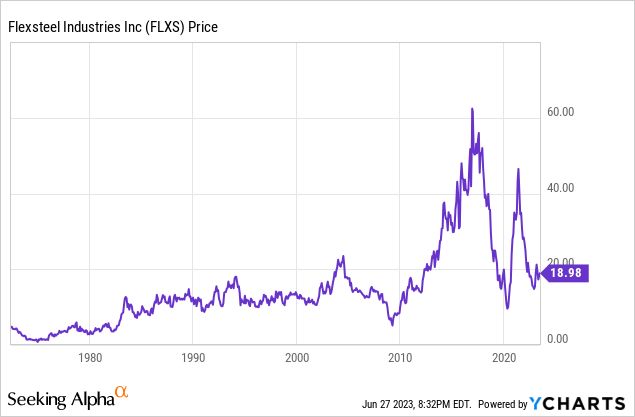

The company manufactures a wide range of residential furniture products, including sofas, loveseats, chairs, reclining rocking chairs, swivel rockers, sofa beds, convertible bedding units, occasional tables, desks, dining tables and chairs, kitchen storage, bedroom furniture, and outdoor furniture, and although its products are essential and the company has been in business for more than 100 years, its operations have been subject to periods of high volatility over the years, as can be seen in the historical price chart.

Currently, shares are trading at $18.98, which represents a 69.87% decline from all-time highs of $62.99 on December 20, 2016, and a 62.88% decline from the recent spike of $51.13 on June 8, 2021. This represents a 2.36% decline since I published the last article in March 2023, and the S&P 500 has increased by 8.18% in the meanwhile despite some recent improvements regarding sales, profit margins, and debt, as well as fewer shares outstanding boosted by share buybacks. Said growing pessimism among investors seems to be related not only to the weakening of operations in recent quarters but also to the uncertainties offered today by the macroeconomic landscape as recessionary concerns due to recent interest rate hikes do not stop growing in the investors’ community.

Sales are stabilizing, albeit at low levels

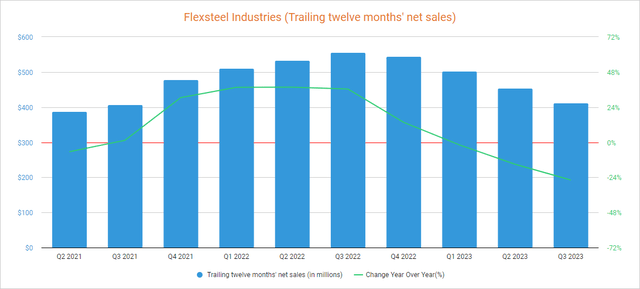

The sales growth trend changed direction during the third quarter of fiscal 2022 as sales declined by 0.92% quarter over quarter, but the decline intensified during the fourth quarter as sales declined by 11.32% quarter over quarter. The decline continued in fiscal 2023 as sales declined by 23.13% sequentially during the first quarter, and by a further 2.72% in the second quarter. This sharp drop in sales has been caused by a steep decline in demand as a consequence of weakening purchasing power among consumers due to inflationary pressures, as well as recessionary concerns. Of course, customer destocking has not helped in maintaining healthy sales.

Flexsteel trailing twelve month’s net sales (Seeking Alpha)

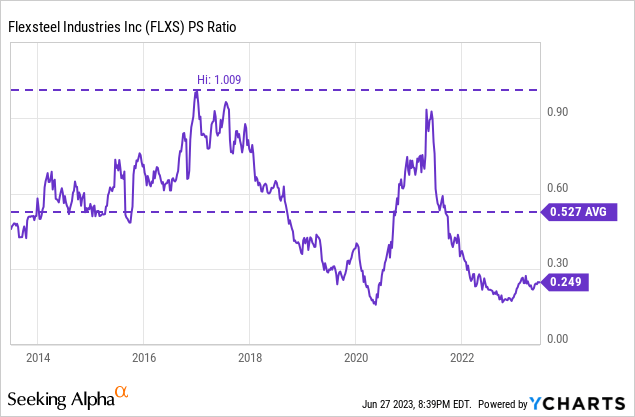

Trailing twelve months’ net sales declined by 25.82% during the third quarter of 2023 as net sales declined by 29.45% year over year, but they actually increased by 6.44% quarter over quarter as the company is launching new products to the market and recent growth initiatives generated net sales of $12 to $13 million in the quarter. In this regard, net sales are expected to decline by 28.17% in fiscal 2023 compared to fiscal 2022, but the recent increase on a quarterly basis is a very positive sign as the company has low-to-zero seasonality while the industry remains very weak. But despite overall net sales declines, the sharp drop in the share price experienced in recent quarters has driven the P/S ratio through the floor at 0.249, which means the company currently generates $4.02 in net sales for each dollar held in shares by investors, annually.

This ratio is 52.75% lower than the average of the past 10 years and represents a 75.32% decline from decade-highs of 1.009 reached in December 2016, which means investors are currently placing much less value on the company’s sales. Nevertheless, the management expects the recent increase in net sales to continue during the fourth quarter of fiscal 2023 and the whole of 2024 as net sales are expected to increase by 6.32% in 2024 compared to 2023. In this regard, the management expects to expand the Charisma Brand, which is its recently launched brand for more price-sensitive younger consumers, as it launched new products with affordable prices during the third quarter of fiscal 2023. In this regard, it seems that the management knows that in order to survive the potential recession that the economy could face soon, it must expand to those groups that may suffer weakening purchasing power the most in times of economic uncertainty.

Profit margins are also starting to stabilize

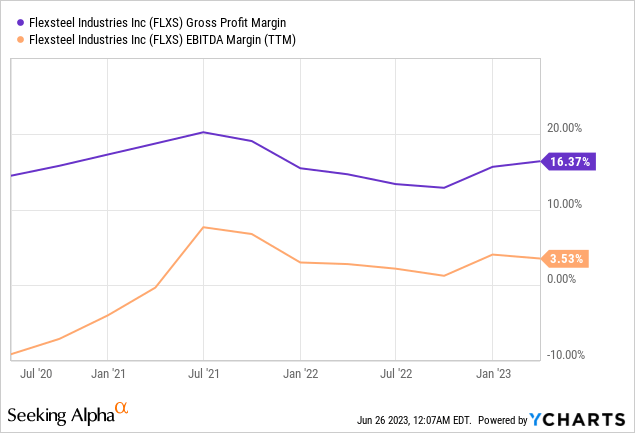

Profit margins continue to stabilize after a large deterioration suffered in fiscal 2022 as a consequence of inflationary pressures, supply chain issues, and lower volumes as competitors are performing aggressive pricing actions in order to reduce their inflated inventories at a time when retail inventories are also high, but both gross profit and EBITDA margins significantly improved in the past 2 quarters boosted by cost savings initiatives and some (but very limited) volume stabilization. In this regard, the trailing twelve months’ gross profit margin currently stands at 16.37%, whereas the EBITDA margin is at 3.25%.

Given the challenging macroeconomic landscape, the company is constantly controlling operating costs, and the management expects these initiatives to further improve gross profit margins in the fourth quarter of fiscal 2023 to 17%-19%, which looks feasible as gross profit margin already improved to 18.82% during the third quarter of fiscal 2023. Nevertheless, strong pricing pressures, as well as uncertain demand put profit margins in a precarious position as operations are currently subject to strong volatility. Furthermore, the EBITDA margin remains low as it stood at 3.37% during the past quarter, which means profitability must improve even further. Nevertheless, debt has not stopped declining as the management has recently made use of the company’s high inventories.

The deleveraging process is almost finished

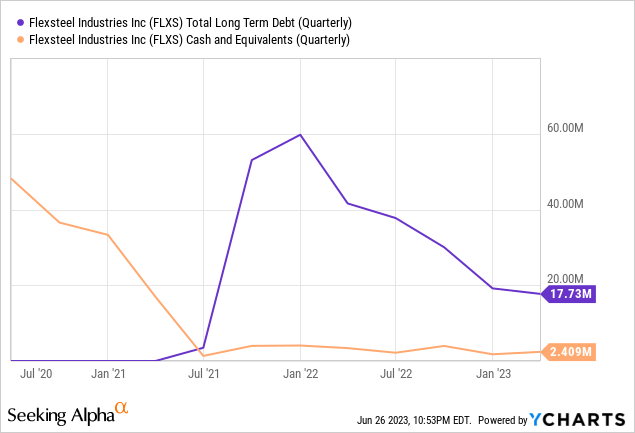

The company is currently reducing its levels of debt acquired in 2021 to expand inventories, invest in profitability and growth initiatives, and carry out aggressive share buybacks, and long-term debt declined by $1.4 million during the third quarter of 2023, with which long-term debt currently stands at $17.73 million vs. ~$60 million at the beginning of the deleveraging process, and further reducing it remains a top priority as stated by the management during the third quarter’s earnings call conference.

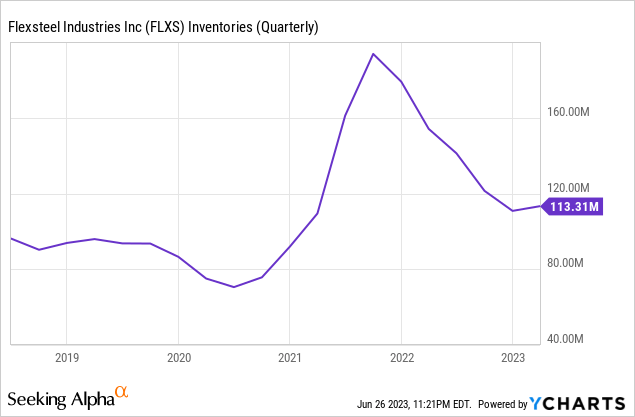

Said deleveraging despite weak operations has been possible thanks to a partial emptying of inventories to $113.31 million, which is still high enough to allow the company to continue with the deleveraging process until ending up with a debt-free balance sheet as the management has recently demonstrated its ability to convert inventories into actual cash. This conversion will be needed to keep deleveraging the balance sheet as cash and equivalents are currently very low at $2.41 million.

Thanks to this significant debt reduction, the company’s risk has decreased significantly and the balance sheet is strengthening in the face of a potential recession, which means that the company is increasingly prepared to face the potential headwinds that may come from macroeconomic factors in the short, medium and (also) the long term.

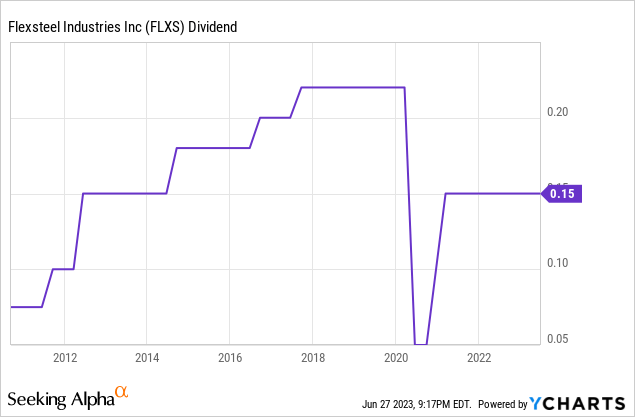

The dividend looks safe in the short term, but profitability remains a concern

The company has been paying dividends since 1938, but the management has a tendency to cut them when the company needs to preserve cash in tough times, allowing it to maneuver by allocating cash in those areas that are most important at any given time. In this regard, a dividend cut from a quarterly payout of $0.22 to $0.05 was announced amidst the coronavirus pandemic crisis in 2020, and the management soon raised it to $0.15 by March 2021.

Considering the current share price of $18.48, the company’s shares are currently offering a dividend yield on cost of 3.17%, which is very generous considering the historically low cash payout ratio. In the table below, I have calculated the dividend sustainability by calculating what percentage of (trailing twelve months’) cash from operations has been allocated in recent quarters for dividend payments and dividend expenses, but in the dividend section of my last article, you can see the cash payout ratio since 2014 where you can better appreciate the company’s ability to cover the dividend in the long term.

| Period | Q3 2021 | Q4 2021 | Q1 2022 | Q2 2022 | Q3 2022 | Q4 2022 | Q1 2023 | Q2 2023 | Q3 2023 |

| Cash from operations (TTM, in millions) | -$11.0 | -$32.7 | -$74.8 | -$62.8 | -$21.2 | $8.0 | $65.3 | $73.6 | $42.4 |

| Dividends paid (TTM, in millions) | $4.4 | $2.6 | $3.2 | $4.1 | $3.1 | $3.9 | $3.7 | $2.5 | $4.1 |

| Interest expense (TTM, in millions) | $0.1 | $0.0 | $0.2 | $0.4 | $0.6 | $0.8 | $1.0 | $1.0 | $1.1 |

| Cash Payout ratio | – | – | – | – | – | 58.75% | 7.20% | 6.47% |

12.26% |

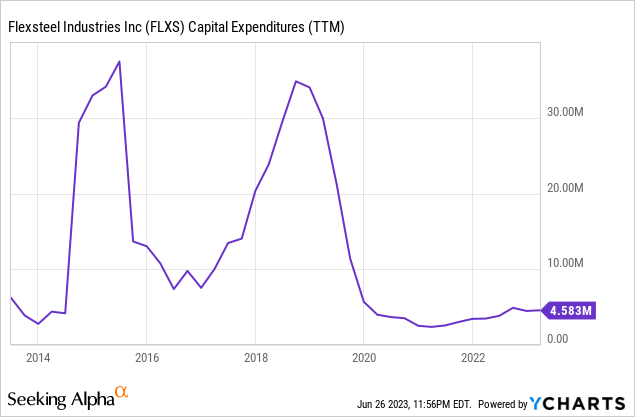

Despite negative cash payout ratios in fiscal 2021 and part of 2022 (due to increasing inventories, strong share buybacks, and weak performance), the cash payout ratio has been very low in recent quarters (and historically), so the dividend growth potential is, in my opinion, quite high. Still, the company is currently investing in growth and profitability initiatives, as well as performing aggressive share buybacks as the share price has declined significantly in recent quarters, and these initiatives are limiting dividend growth (and should limit it for longer as the macroeconomic landscape is still uncertain). Furthermore, the company will eventually need to increase its profitability in order to not rely on inventories in order to keep issuing the dividend as cash from operations was $5.8 million during the third quarter of fiscal 2023, inventories increased by $2.5 million, and accounts receivable increased by $3.8 million but accounts payable also increased by $8 million, and the company needs to cover over $4 million in annual capital expenditures.

Regarding profitability investments, capital expenditures are expected to be in the $1 million to $1.5 million range during the fourth quarter of fiscal 2023 as the company is currently expanding its ERP (Enterprise Resource Planning) capabilities, which is not so high considering the company’s historical cash generating capacity.

Share buybacks continue at full speed, although should soon slow down

Due to the sharp decline that the share price experienced since the coronavirus pandemic in early 2020, the management decided to (only) partially raise the dividend after the cut in order to allocate more cash for share buybacks.

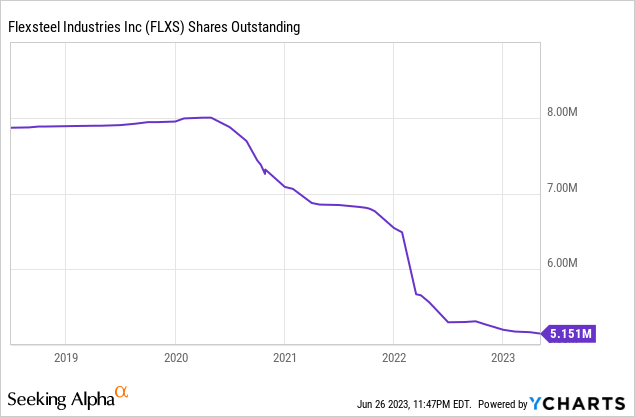

This means that each share now represents a significantly bigger portion of the company as the total number of shares outstanding has declined by 34.53% during the past 5 years, and the management expects to perform further share buybacks in the short term. Still, inventories are approaching lower levels, so the current rate of share buybacks is not sustainable in the long term. Even so, I believe that the company will be able to continue performing share buybacks (albeit at a slower rate) once the long-term debt has been paid in full (and the macroeconomic context slightly improves).

Risks worth mentioning

Overall, I believe that Flexsteel’s risks are not as high as they may appear at first glance. But despite the fact that operations seem to be stabilizing and the debt is about to be completely reduced, there are certain risks that I would like to highlight for the short and medium term.

- A potential recession could cause a decline in demand for the company’s products as consumers with lower purchasing power could delay updating their home furniture, and this would have a direct impact not only on net sales but also on margins due to lower volumes.

- Inventories are being reduced at a very high rate. Although this is a very good sign as the company is converting them into cash that is being used to cover the dividend, make strong share buybacks, invest in profitability and growth initiatives, and deleverage the balance sheet, these inventories are limited and will soon stop providing the current boost to cash from operations.

- Profit margins could remain depressed if inflationary pressures do not ease as retailers deplete inventories to healthier levels.

- The dividend could be cut if the current headwinds (inflationary pressures and weaker demand) persist for longer than expected, or if a recession finally materializes. Of course, share buybacks could pause in such a scenario.

Conclusion

It is true that Flexsteel’s operations are still significantly weak, and that is why the share price remains depressed despite the recent recovery in the S&P 500. But despite this, both sales and profit margins have recently improved, and long-term debt keeps declining, so the company is, in my opinion, well prepared for a potential downturn. I believe that investors shouldn’t forget that the company’s operations date back to 1893 and that the recent share price decline (despite a 34.53% decrease in the number of shares outstanding) is leaving a juicy (given the historically low cash payout ratio) dividend yield on cost of 3.17%.

For this reason, and given the recent improvements in sales and profit margins, as well as having (still) high inventories, I believe that this represents a good opportunity for long-term dividend investors with enough patience to wait for the current macroeconomic landscape to improve as, in my opinion, Flexsteel is poised to be a wealth creator for long-term investors, especially considering insiders own a whopping 28.59% of the company’s shares. Still, short and medium-term risks remain a concern as profit margins need a further slight improvement as inventories are being reduced at a fast rate in order to deleverage the balance sheet while covering the dividend, which should be possible once retail inventories get reduced even more and inflationary pressures ease a bit more.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Read the full article here