Co-authored with “Hidden Opportunities.”

“Blue chip” is a term used to describe well-established publicly traded companies that are nationally (or internationally) recognized, well established, and financially sound. Retail investors often feel comfortable owning these names as they have reputable brands built and maintained over many years. A blue chip company typically provides widely known and high-quality goods or services.

Considering their established nature in the industry and stable operations, blue chips are a must-have in your portfolio. Today, we will discuss Owl Rock Capital Corporation (ORCC), the 2nd largest public business development company, or BDC, that provides the dual benefits of safety and high yields and represents an under-the-radar blue chip investment. Let’s dive in!

Background

ORCC provides direct lending solutions to U.S. upper middle-market companies. The BDC’s typical customer base generates an average EBITDA of $176 million. Middle-market companies constitute ~40% of the GDP, employ about 40% of the workforce, and represent the heartbeat of the American economy.

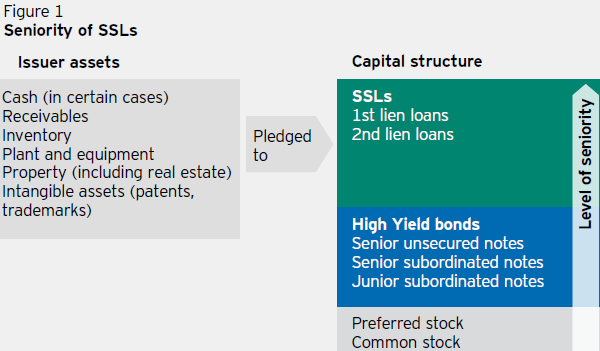

ORCC provides vital financing to these companies through the issue of predominantly senior secured loans. 71% of ORCC’s investment portfolio is first lien, and 14% is second lien loans, providing significant safety in good and bad times. Source.

Invesco website

Senior loans are backed by the borrowers’ vital assets. Looking at data over the past 30 years, we see that during instances of default, senior secured loans typically recover 80% of the principal on average (compared to 48% for high yield bonds). With such a high recovery rate and a historical average annual default rate of 3%, the historical net credit loss of senior secured loans is a meager 0.6%.

ORCC maintains a highly conservative lending strategy backed by its disciplined investment and underwriting process, and has a small 15 bps annual loss rate since its inception. This lending diligence and prudent portfolio composition makes ORCC highly suitable for your portfolio when economic uncertainties surround us.

Growing Portfolio With Strong Credit Quality

ORCC maintains an investment-grade balance sheet, rated BBB- by leading agencies. The company’s investments are diversified across 187 companies and 98% of the borrowings are floating rate.

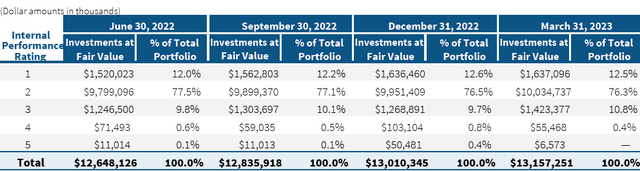

~90% of ORCC’s assets are performing at or above initial expectations and <1% is performing below expectation or is at a default status, portraying a picture of good health and bright prospects as we stare down the recession barrel. Source.

ORCC Mar 2023 Investor Presentation

During Q1, ORCC reported a record Net Investment Income (“NII”) of $0.45 and easily covered its $0.33 dividend. The BDC also issued a $0.04 supplemental dividend in the last quarter. For Q2, ORCC announced a supplement increase to $0.06 to be paid in June and the regular $0.33 dividend to be paid in July. ORCC intends on continuing to pay regular supplements based on actual earnings as long as they continue to exceed the regular dividend.

ORCC is taking advantage of the rising rate environment and is firing on all cylinders while maintaining its leverage at 1.21x. The BDC has $1.7 billion of liquidity in cash and undrawn credit, providing adequate flexibility with its cash flows and the ability to weather declining credit quality.

Deeply Discounted Valuation – Insiders Are Loading Up!

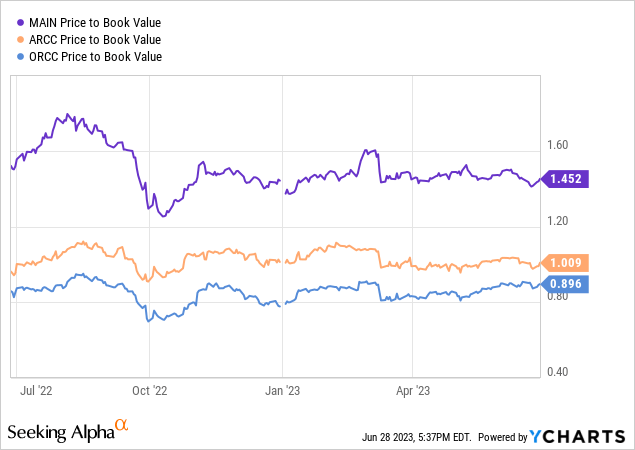

ORCC trades at a deep 10% discount to NAV, a true bargain compared to the current valuations of blue chip BDCs like Ares Capital Corp. (ARCC) and Main Street Capital Corporation (MAIN), which represent stellar investments on their own merits.

It isn’t surprising to see ORCC aggressively pursuing share repurchases at this massive discount. As of May, $49 million worth of common stock was repurchased by the company from its previously announced $150 million share repurchase plan.

ORCC insiders purchased almost $1.2 million of common stock in May, with CEO Craig Packer responsible for the bulk ($1 million) of these purchases. In addition, ORCC’s external manager has been scooping up shares using the employee investment vehicle. Almost $25 million worth of stock was purchased as part of the program, bringing the total purchase to $74 million. Together, these repurchases represent 1.4% of ORCC’s market cap, reflecting a significant return to shareholders. There is more where that came from, as $100 million remains available in the funds approved by the board.

Insider buying activity indicates a strong alignment of management intentions with shareholder interest, making it a big plus for income investors.

Conclusion

Understanding what you own, why you own it, and how it will help achieve your investment goals is critical. By understanding the fundamentals of your investments and the execution, you will not feel pressured to make poor decisions just based on the stock price movements. At High Dividend Opportunities, we provide detailed insights on the fundamentals of the securities we recommend to our subscribers. Our “model portfolio” has +45 dividend payers with an overall yield of +9%, and ORCC represents one of many gems that contribute to our growing income stream.

ORCC is a blue chip BDC we are buying with both hands due to its:

-

Investment grade credit ratings and healthy liquidity position

-

98% floating rate assets primarily in senior secured loans and record low annual loss rates since inception

-

Aggressive share repurchases and heavy insider buying in recent months

-

Massive ~10% discount to NAV

-

Well-covered 10% yield to lock in at the deeply discounted valuation.

We may be facing a recession, but having ORCC in my portfolio at current price levels provides me a lot of comfort. This is because of the portfolio composition into senior secured loans, increasing management alignment with shareholders’ interests, and adequately covered dividends. ORCC’s discount to NAV won’t last long; this is the opportunity to lock in big yields from this blue-chip BDC. I am buying up more Owl Rock Capital Corporation stock while insiders are, too!

Read the full article here