Investment Thesis

With quarterly results just around the corner, I wanted to take a look at ManpowerGroup (NYSE:MAN) to see if it is worth a long-term investment. With current negative macroeconomic sentiment looming globally and the lack of revenue growth, I believe that this is not a good time for a new investor to start a position and would wait until the company gets back to decent revenue growth.

Outlook

Macroeconomic Headaches

Economies around the world have been very hot for a while. The United States has been on a tear of hiring for a while now, which is not what the Fed was looking for when it started to increase interest rates to push down inflation. We are starting to see some cracks in the unemployment numbers right now, however, the US economy is still very robust and will need further intervention from the Fed in the upcoming months as two more hikes are still on the table. Now that we are seeing a slowdown kicking in, I don’t see how the company is going to grow its business, as most of the regions it operates in are seeing declines in revenues. The management is seeing further softening in the demand for their services, and it sounds like it is going to be persistent throughout the year.

With higher unemployment numbers predicted to come in the remainder of the year, I can see a lot of volatility in the global stock markets which will affect all the stocks not just Manpower.

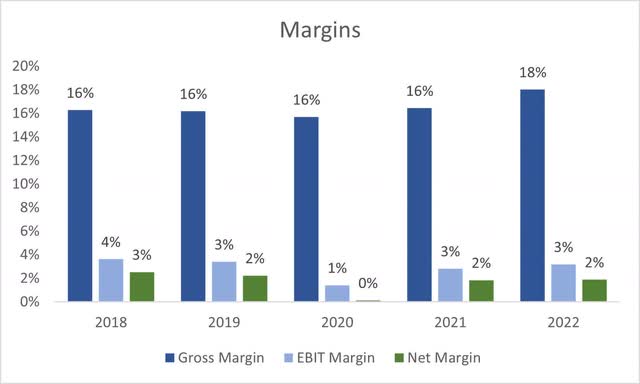

Margins

In the most recent quarters, which are FY22 and Q1 ’23, the company managed to improve margins. The company is operating with very thin net margins, so any improvement is going to play a huge role in the company’s valuation. If the company cannot grow through the top line growth, as it has not done for at least the last decade, the company needs to look into becoming more efficient and improving these thin margins by any means necessary.

The management has been cutting some “lower margin activity”, which is good to hear. The company needs to focus on their higher margin businesses like Experis to achieve higher efficiencies, which will lead to higher EPS without the need for top-line growth if the top line at least remains where it is at these years.

I think there are a lot of ways for the company to improve profitability. The company is going the right way in achieving this with its DDI strategy. The main point in my opinion of this strategy is the digitization and innovation parts. I believe that digitization is one of the most productive ways of achieving higher margins, no matter what the company is. I have seen many examples of logistics and other companies that you would hardly associate with technology where digitization of any part of their business, which in those cases was mostly customer-side, improved operating margins tremendously. Companies like Schneider Electric, an old-timer company that used to sell electrical products moved on to also provide energy management solutions.

Levi’s (LEVI) managed to get ahead of the COVID pandemic by investing in digitization efforts early on and managed to switch a lot of their business online as the company invested in AI and predictive analytics to spot that customers are more into online shopping than they were before.

ManpowerGroup belongs to this category as it is quite old and if their strategy works out in the future, I could see them rewarding their shareholders handsomely if investors can look past 0 top-line growth.

Financials

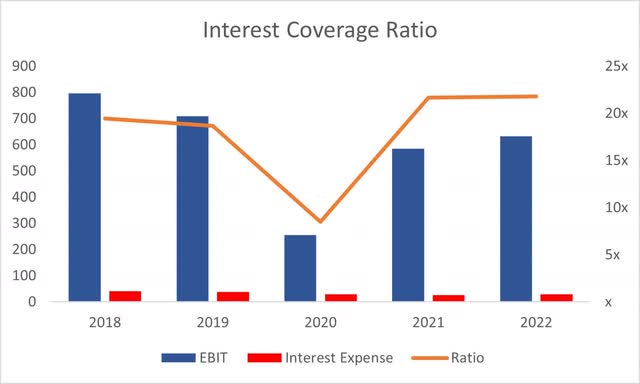

The below graphs will be as of FY22. I will provide some figures from the latest quarter if I believe they will be necessary for more color. As of Q1 ’23, the company had $706m in cash and equivalents against $972m in long-term debt. Many investors may stay away from a company just because of this difference; however, leverage is a great way to operate a company especially if it is used sensibly and is manageable. MAN’s debt is sensible in my opinion and does not pose any risk of default because the interest coverage ratio is around 22x, which means that EBIT can cover the annual interest in debt 22 times over. Even a coverage ratio of 2 or 3 is deemed healthy.

Interest Coverage Ratio (Author)

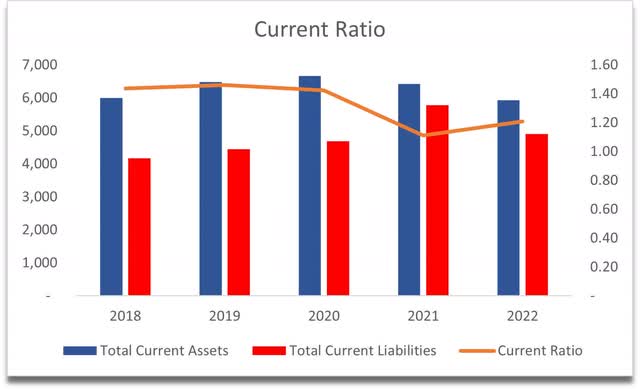

The company’s current ratio or working capital ratio stands just a little over 1 which indicates that it can cover its short-term obligations without an issue if they were all due today. It doesn’t look like the company has any liquidity issues.

Current Ratio (Author)

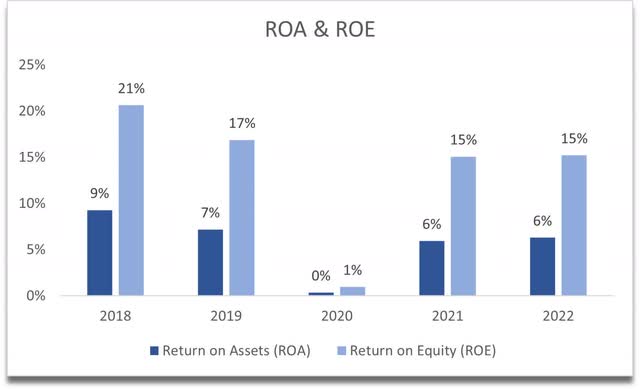

In terms of efficiency and profitability, ROA and ROE are acceptable but nothing to write home about. These are just above my minimums of 5% on ROA and 10% on ROE. These indicate that the management can utilize the company’s and shareholder capital somewhat efficiently and is creating some value.

ROA and ROE (Author)

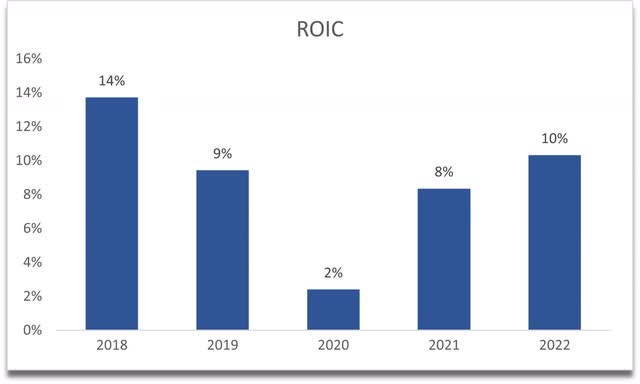

A very similar story can be seen in the company’s return on invested capital. I’m looking for around 10% as a minimum and the company reached 10% just last year. I’d like to see it improve over time. Nevertheless, 10% indicates to me that the company has some competitive advantage and a moat.

Return on invested capital (Author)

In terms of margins, as I mentioned earlier, I would like to see these improve with further advancements in technology, digitization, and even AI implementation. Even with the slightest improvements over the next decade, as long as revenues remain stable, the company will achieve higher profitability and valuation.

Margins (Author)

Overall, the metrics are good enough to warrant the lowest margin of safety I add to companies when I perform a DCF analysis in the next section. I did not see any red flags that would warrant extra caution.

Valuation

In the last decade, the company did not grow its top line at all. Revenues went from $20.25B in FY13 to $19.83B at the end of FY22. I don’t see a reason why this would change in the next decade as I believe the way the company will create value is by improving profitability and keeping revenues stable as they have.

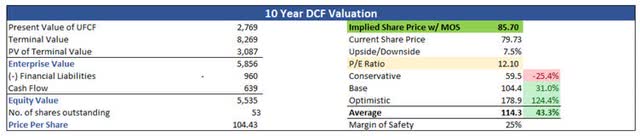

For the base case, I went with 42bps or .42% of revenue increase over the next decade. For the optimistic case, I went with 2.9% to account for some unforeseen catalyst, and the conservative case, I went with -1.5% CAGR.

For the margins, I decided to improve gross and operating margins by around 100bps over the next decade because I believe that is very achievable. This will bring net margins from 1.9% in FY22 to around 3.2% by ’32. For the optimistic case, I improved gross and operating margins by an extra 50bps in every period, and vice versa for the conservative case from the base case.

As I mentioned I am ok with adding a 25% margin of safety because the financials were good enough. With that said, the company’s intrinsic value with these assumptions is $85.70, implying a 7.5% upside.

Intrinsic Value (Author)

Closing Comments

According to the calculations, even with basically no revenue growth over the next decade, the company is cheap. Do I think it’s cheap? No, I don’t think it’s a great deal right now. There are too many variables at play that can keep the company just floating around this price point for much longer and never rewarding its shareholders. Over the last 10 years, the total return of the company has been around 67%, compared to SPY’s 227%. In my opinion, the lack of top-line growth is what investors are looking at and if the company is not able to find a way to improve that, the share price will never see the potential that the company holds in terms of actual improvements in profitability and efficiency.

For new investors, I would suggest not investing right now in the company even though there aren’t many good deals out there right now. It is better to be on the sidelines and wait for some macroeconomic catalyst that will bring more volatility to the markets, which can present better entry points for companies like MAN.

If you are already an investor and are not looking to sell, I understand. The dividend yield is decent at around 3.7% with a 33% payout ratio, meaning the dividend is safe and with a decent dividend growth historically.

I’ll follow how the company’s digitization and innovation strategy progresses and will reassess if needed in the future, but for now, I don’t think it’s worth putting my money into the company.

Read the full article here