Investment Thesis

Vizsla Silver (NYSE:VZLA) is Canadian silver development company, with its flagship Panuco project in Mexico. The stock is listed in the U.S. and Canada. The company’s fiscal year ends in April and it reports in Canadian Dollars.

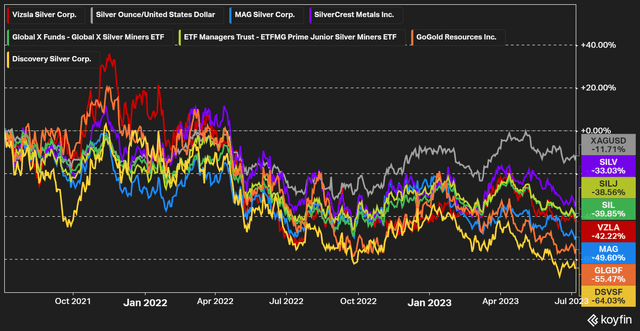

Over the last few years, Vizsla Silver has managed to grow the Panuco silver gold project to over 200M high-grade silver equivalent ounces but has like most silver mining companies had a poor stock price performance over the last two years. Even if there are developers in the industry which have performed significantly worse.

Figure 1 – Source: Koyfin

Vizsla Silver is aiming to become the next large high-grade silver producer in Mexico, which has the potential to re-rate the stock substantially in the long run, but the investment is not without risk.

Size & Liquidity

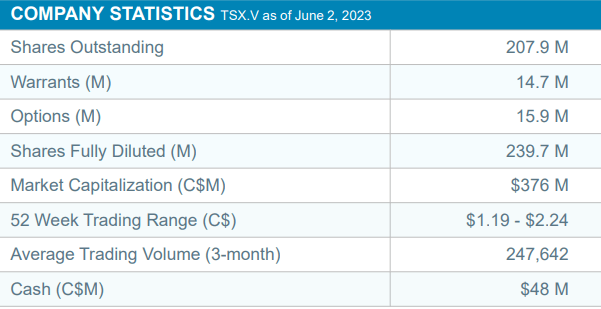

It has now been a few months since the last financial statement was filed, as the annual report has yet to be released. So, I will rely on the corporate presentation for the share count, where we can see that the company has 239.7M fully diluted shares outstanding. This includes the shares issued in the C$45M private placement earlier this year.

Figure 2 – Source: Vizsla Corporate Presentation

That gives us a market cap of $278M using the latest share price. Vizsla Silver has no debt and C$48M in cash, which translates to an enterprise value of 242M.

With C$48M in cash, there are no near-term liquidity concerns. The company should have sufficient cash to drill aggressively in 2023, release a resource update during the second half of this year, and a preliminary economic assessment (“PEA”) following that in 2024.

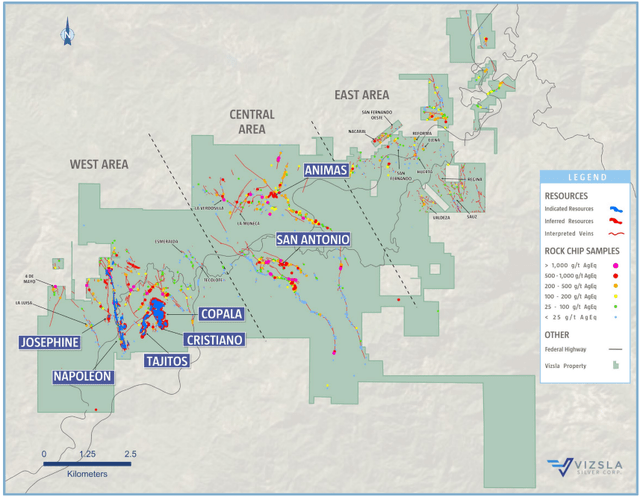

Panuco Project

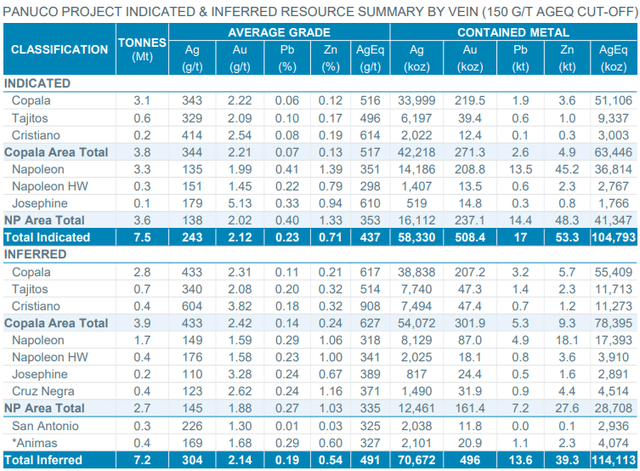

Vizsla Silver owns 100% of its flagship Panuco project and has been drilling aggressively lately. The company did in January of 2023 release a resource update, which confirmed the substantial size of the project.

Figure 3 – Source: Vizsla Corporate Presentation

The January 2023 release confirmed 105M indicated silver equivalent resource ounces with an excellent grade of 437 g/t AgEq. The resource also has 114M inferred silver equivalent resource ounces with a grade of 491 g/t AgEq. Later this year, there is yet another resource update due to be released, which should hopefully grow the existing resource by a decent amount.

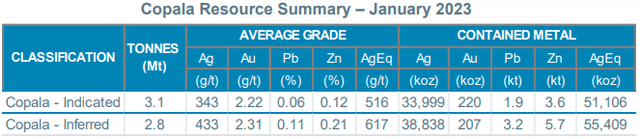

Figure 4 – Source: Vizsla Corporate Presentation

Copala is the most interesting area of the project, with its near-surface high-grade structure. The structure accounts for almost half of the known resource of the Panuco project today, but the project covers a fairly substantial size, which means it has the potential to continue to grow over the next few years.

Figure 5 – Source: Vizsla Corporate Presentation

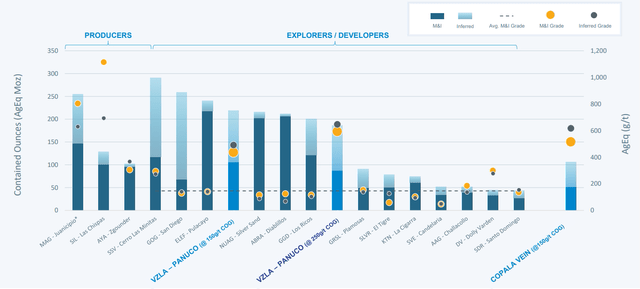

Comparison & Conclusion

There is little doubt Vizsla Silver, and the Panuco project has the potential to become the next high-grade silver mine in Mexico. The below figure illustrates the quality characteristics of the project, even if it is of course not completely fair to compare the grade with known open-pit projects.

Figure 6 – Source: Vizsla Corporate Presentation

It is very difficult to accurately estimate the value of the project at this stage before a preliminary economic assessment has been released. Even if I do think it is relatively safe to assume the net present value will be multiples of the current market cap.

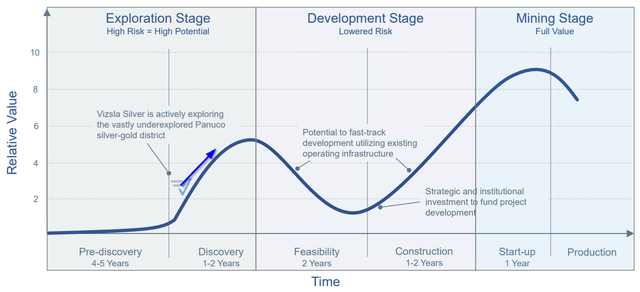

What makes me a little bit hesitant to invest in Vizsla Silver at this point, is the stage of the project. I don’t doubt Vizsla Silver will grow with the next resource update and the initial independent economic estimates will be confirmed with a PEA in 2024. However, I do think at least there is a risk that the company is closer to the first peak in the Lassonde Curve than what the company would like to admit, as illustrated by my arrow in the chart below.

Figure 7 – Source: Vizsla Corporate Presentation

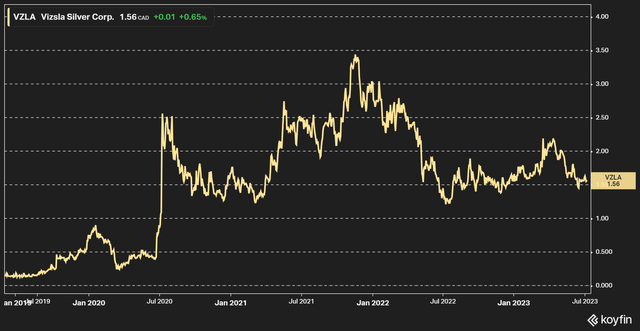

The stock price movement is rarely as smooth as the graph above illustrates and with the extremely depressed sentiment for most silver miners today and developers specifically. It is difficult to know how much of the recent stock price performance is due to the development cycle and how much is just due to the very poor sentiment for silver miners.

Figure 8 – Source: Koyfin

Given the size of the Panuco project, Vizsla Silver could in theory be exploring this asset for some time, but let’s assume the company will aim to move forward towards production as quickly as possible. We are probably still 4-5 years from production in the best of circumstances, which is a rough guess. So, even if the company has liquidity for the next year, we can likely expect more dilution until the project reaches production.

Now, if metal prices cooperate and the sentiment turns more positive over the next few years, which I think is likely. Vizsla Silver is likely to perform quite well. Having said that, we have lately seen not just developers get cheap, but also producers sell-off substantially as illustrated in figure 1 above. So, even if Vizsla Silver looks relatively attractive on an absolute basis, I don’t think the risk-reward today is more attractive than known producers or later stage developers.

Also, while I still believe Mexico is a viable mining country, the risk has increased lately with more permitting delays than what we have seen in the past. We have still seen underground (and some open-pit) projects get permitted under the current administration. However, I would need to see a larger margin of safety than what Vizsla Silver offers today to add more Mexican development risk to the portfolio in the current environment.

Read the full article here