Commercial office real estate hasn’t been a popular place over the past 12+ months. However, it appears that the dust has finally settled, with plenty of risks already priced into the beaten down names. As the saying goes, “buy straw hats in winter”, since that’s when the best bargains can be found.

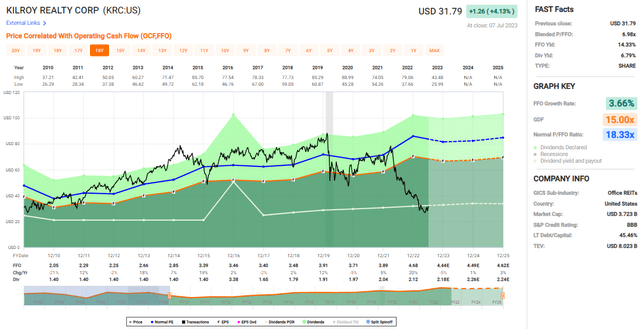

Kilroy Realty (NYSE:KRC) represents one such opportunity, with recent price movements suggesting that it’s found a bottom. As shown below, KRC has found support at the ~$27 level and has now moved over the $30 threshold.

KRC Stock (Seeking Alpha)

I last covered KRC here back in February, highlighting its pivot towards the life sciences industry and its quality portfolio. In this article, I provide an update and discuss why KRC represents a bargain high yield opportunity at present.

Why KRC?

Kilroy Realty is an office REIT that’s focused on owning and developing properties along the U.S. west coast and Austin, Texas. It’s also one of the oldest REITs, having been around for over 70 years, and is led by its long-time CEO and Chairman with its namesake, John Kilroy, who will retire at the end of this year.

Based on the share price action alone over the past 12 months, it would seem as if the company were falling apart. However, reality doesn’t seem to justify that, as occupancy and leased rates were 90% and 92% during the first quarter, respectively, falling by just 1% point each from 91% and 93% in the prior year period.

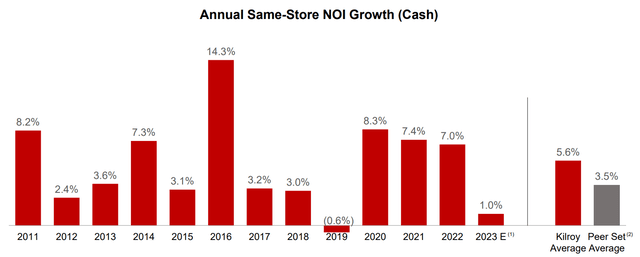

Recurring same-store NOI was up by 9% YoY, driven by top line revenue growth, and this translated to the bottom line, with FFO/share growth of 5.2% compared to Q1 of last year. As shown below, KRC has produced same-store NOI growth in nearly every year since 2011, with average growth outpacing the peer average.

Investor Presentation

Of course, what is top on everyone’s mind is what the outlook for the office market will look like in the near to medium term. The good news is that KRC has the youngest portfolio among its office REIT peers, with an average property age of just 11 years, sitting well below the 34 year average.

Plus, a number of companies like Meta (META) have mandated that their employees spending more than half of their workweek in the office. This is on back of comments from CEOs such as Marc Benioff from Salesforce (CRM) stating that new employee work-from-home productivity was lower than that of existing employees. From an office space standpoint, it doesn’t really matter whether if an employee is in the office 3 days a week versus 5 days, because the same amount of space must be allotted to that employee in both scenarios.

As shown below, other big companies in KRC’s markets such as Starbucks (SBUX), Amazon (AMZN), Disney (DIS), and Apple (AAPL) have mandated employees in the office for 3 or more days per week.

Investor Presentation

Moreover, KRC is well-positioned to ride the AI-boom, as 40% of AI companies are based in the San Francisco Bay Area, where KRC has a presence. KRC also continues to make a strong push into the burgeoning Life Science segment, which involves plenty of lab work that’s simply not possible to perform at home.

Life Science has a number of attractive attributes, not least of which includes the need for a larger pipeline of drugs to be developed to address the growing adult senior population, the fastest growing demographic in the U.S. Plus, tenants tend to be clustered together, as in the case for life sciences REIT Alexandria Real Estate Equities (ARE).

Clustering of tenants makes sense for life science, as they tend to draw from the same talent pool, thereby making established clusters all the more valuable. KRC’s Oyster Point development is well-positioned for this. Management expects life science to represent 20% of company NOI by the time KOP Phase 2 is complete, and grow to 30% with future life science projects.

Notably, KRC maintains a strong balance sheet for the current environment, with $1.6 billion in liquidity. 95% of its debt is unsecured, giving it balance sheet flexibility and it has no significant debt maturities until December of 2024. KRC also carries a safe net debt to EBITDA ratio of 5.7x, sitting below the 6.0x mark generally regarded as being safe by ratings agencies, and supporting its BBB investment grade credit rating.

This lends support to KRC’s 6.8% dividend yield, which is well-protected by a 49% payout ratio. Management stated on the last conference call that it feels comfortable with at least maintaining the current dividend rate.

Risks to KRC include higher than expected interest rates in the near term, and the potential for a recession, which may temporarily reduce tenant demand for office space. Also, executive transition also introduces uncertainty to the enterprise, with aforementioned pending retirement of John Kilroy and the search for a new CEO currently underway.

Lastly, KRC remains heavily undervalued at the current price of $31.79 with a forward P/FFO of just 7.2. At this low of a valuation, KRC is essentially priced for a perpetual decline. I simply don’t see that as being the case, considering all of the aforementioned discussion.

While near-term headwinds around office space may mute growth, I see KRC getting back onto its footing and growing its FFO/share annually in the mid-single digit range within the next 2-3 years. As such, I see potential for KRC to get back to a P/FFO of 10x, which could equate to potentially strong double-digit returns.

FAST Graphs

Investor Takeaway

Kilroy Realty has seen its share price take a beating over the past 12+ months but that doesn’t reflect reality in terms of the company’s performance. KRC is well-positioned to ride the AI-boom and benefit from its growing presence in burgeoning Life Science segment. Moreover, its strong balance sheet and well-protected high dividend yield make it attractive for income investors. With a low valuation and high yield, KRC makes for an appealing opportunity for value investors.

Read the full article here