High yield investing sometimes gets a bad reputation for being risky. While that may be the case for standard C Corporations that are supporting an untenable dividend, the same isn’t always the case for asset classes such as REITs that are designed for higher yield.

That’s because REITs come with tax advantages considering they are pass-through entities and don’t have to pay a corporate tax so long as they distribute 90% of their taxable income.

This brings me to Ladder Capital (NYSE:LADR), which stands out in the commercial mortgage REIT space for being internally-managed. I last covered LADR here back in March, highlighting its significant discount to book value.

It appears the market has caught onto the unwarranted discount, as the stock has produced a 26% total return since my last piece, far surpassing the AI-driven 12.6% rally of the S&P 500 (SPY) over the same timeframe. In this article, I revisit the stock and discuss why it remains an appealing high yield opportunity.

Why LADR?

Ladder Capital is focused on originating senior secured loans that are backed by institutional quality real estate in the middle market. As mentioned earlier, what sets LADR apart from peers like Blackstone Mortgage Trust (BXMT), and Starwood Property Trust (STWD) is its internal management structure.

While external management comes with benefits in being able to tap a wide-reaching platform, internal management teams remove the overhang for potential conflict of interest. That’s because the compensation of internal management teams is not directly tied to the size of assets under management, as in the case of external teams.

In LADR’s case, management and directors own over 10% of the company and employees get compensated based on profits with a significant portion in stock meaning there is good alignment of interest with shareholders. It also has a deep bench, with management having an average of 11 years at the company and 22 years of industry experience on average.

Ladder has a national presence, having originated 475 loans in 48 U.S. states since inception. At present, it has a $5.9 billion portfolio value inclusive of cash. Somewhat similarly to Starwood Property Trust, LADR’s portfolio contains more than just loans, with CRE Securities and physical net lease properties as well.

Nonetheless, commercial loans still make up the bulk (82%) of LADR’s asset base. This segment is carefully constructed with 99% senior secured first mortgage loans with average loan-to-value of 68%, implying a significant 32% equity buffer in the event of a borrower default.

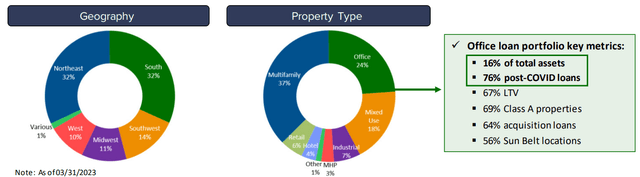

Moreover, the growing multifamily segment makes up 37% of the commercial lending portfolio with office comprising nearly a quarter at 24%. Three-quarters of the office loans were generated post-COVID with majority being Class A properties and over half located in Sunbelt locations, as shown below.

Investor Presentation

According to Hoya Capital, office properties in the Sunbelt have seen a far lower down turn in office leasing this year at -13% below 2019 levels compared to -37% for coastal-focused offices. This is driven by net population growth, shorter commute times, and a more favorable industry mix across the Sunbelt region.

Meanwhile, LADR demonstrated a strong return on equity of 12.3% during the first quarter, driven by its majority floating rate loan portfolio. This enabled LADR to out-earn its $0.23 quarterly dividend by a wide margin with $0.38 in distributable EPS, equating to a 61% payout ratio. This also goes a long way in enabling LADR to pad its CECL Reserve by an additional 25% to $25.5 million in preparation for potential losses down the line.

Importantly, LADR’s balance sheet is in good shape, with no debt maturities until October of 2025, and a debt to equity ratio of 1.8x, sitting below that of peers BXMT and STWD, which carry leverage in the +3x and +2x range, respectively. It also has $950 million worth of same day liquidity to address any immediate cash needs should they arise.

Risks to LADR include a worse than expected recession, which may pressure borrowers’ ability to repay. This may also have an outsized effect on the office segment, as this property type is more vulnerable than others to a severe economic downturn.

This risk is partially offset by other more durable asset classes such as multifamily as well as LADR’s securities portfolio, of which 84% are AAA rated securities, and 99.5% carry investment grade credit ratings. Plus, 73% of the 156 net lease property portfolio have investment grade tenants with long lease durations, sitting higher than Realty Income Corp (O), which carries 41% investment grade rated tenants.

Lastly, LADR remains materially undervalued at the current price of $10.94, representing a 20% discount to undepreciated book value of $13.64. LADR also appears cheap from a forward earnings standpoint (note: PE and not P/FFO is applicable for commercial mortgage REITS) with a forward PE of 8.2. Investors could see potential double-digit total returns in the high teens including the 8.4% dividend yield, should LADR’s share price bridge just half the current valuation gap to its undepreciated book value.

Investor Takeaway

Ladder Capital represents an attractive high yield play at present, with a solid internal management team, carefully constructed asset portfolio and compelling valuation gap to undepreciated book value. Moreover, it carries a strong balance sheet with plenty of liquidity and buffer between its dividend and earnings. As such, high yield investors looking for a company with strong alignment of interest with shareholders ought to consider LADR at current levels.

Read the full article here