Please note, this article recommends the MAIN bonds, not the common shares. CUSIP: 56035LAE4

Main Street Capital (NYSE:MAIN) is the best-in-class business development company. For those of you who are unfamiliar with BDCs, they were created 50-plus years ago as a means for regular investors to gain access to middle market company investments. They’re similar to venture capital funds.

Congress created the BDC concept in 1980 in an effort to stimulate economic growth. BDCs provide ordinary investors a chance to buy shares that contribute to the growth of middle market companies. In turn, middle market companies are able to deploy the capital from BDCs. They use this capital to expand their businesses, finance capital projects, and create jobs.

BDCs fall under the regulatory authority of the 1940 Act. Accordingly, there are a number of restrictions on BDCs. For example, a BDC’s board must have a majority of independent directors. However, BDCs are also exempt from many of the regulatory constraints of the 1940 Act.

The BDC Council oversees the industry. They attempt to create reforms that strike a balance between facilitating growth of the BDC industry and ensuring adequate investor protections exist.

In all, there are 49 publicly-traded BDCs and a host of non-traded and private BDCs. The largest BDC is Ares Capital, worth over $10 billion. It’s also one of the most conservative.

They’re close cousins of closed-end funds since they trade on major exchanges, come to market via IPO, and have strict rules as to how much leverage and certain risks that are taken.

The BDC must invest at least 70% of its assets in private or public U.S. firms with market values of less than $250 million. They also must provide managerial assistance to the companies in its portfolio.

Main Street Capital

MAIN is one of the most popular BDCs because of its strong management team and track record. Most consider MAIN a “best in breed” as its history of navigating market turmoil has been stellar. BDCs can use leverage to enhance returns. Typically, this is a benefit in most markets, especially when the yield curve is steep or upward sloping. In a lot of ways, they’re like a bank that lends to small, private companies.

Because of that, it trades at a huge premium to the NAV. The company will provide a quarterly NAV that’s the market value of all the loans in the portfolio on a per share basis. Typically, the share price trades near that NAV.

In the case of MAIN, it trades well above because of that great track record that we talked about. The yield is based off of the price you purchase the shares at, not off of the NAV. That means when the share price is above NAV, your yield is less than it would be if it was a based off of NAV – like in a mutual fund. A discount would enhance the yield.

The current share price is just over $40 per share, while the NAV is $27.23. The dividend per share is $2.76 so when you calculate that off the share price, your yield is 6.94%, while off of NAV it is 10.1%. So if the premium was gone, you would earn more than three points of additional yield.

Timing is everything: When you buy the underlying common shares is extremely important for your overall return. Paying a large premium typically doesn’t result in favorable results.

Main Street Capital 3% 2026 Notes (56035LAE4) – BBB-, YTW: 7.46%

Today, the better deal is in the notes. These are the bonds that the BDC issues to provide the funding for their leverage. Some key stats:

- Maturity: 07.14.2026

- Coupon Rate: 3.0%

- Last Traded Price: $88.16

- Last Trade Yield: 7.46%

- Call Date: 06.14.2026

- Rating: BBB-

The ratings agency slaps a BBB- rating on most of the top managers. The ratings are almost meaningless, but the notes are investment grade. For the most part, it appears that they do not know how to analyze and rate the BDCs, at least like BDC Buzz can on Seeking Alpha.

However, some BDCs are better than others, hence the differences in yields, track records, management teams, and valuations (premiums or discounts of the shares to NAV). If they were equal in terms of quality, they would have the same yields and same valuations.

The market clearly believes in MAIN, and MAIN has not let them down. Even in the Financial Crisis of 2008, they did not cut their dividend.

As the bondholder, you are at the top of the food chain. As the interest payments come in, they pay the administrative costs and then the investors.

MAIN produces significant cash flows and their due diligence on whom they loan money to creates a lower default profile than most other BDCs. They look for lower middle market (“LMM”) businesses with enterprise values between 4.5x – 6.5x EBITDA.

They target 8%-12% gross yields.

Main Street Capital

Most importantly, the bondholders (i.e., if you buy the notes which we recommend) have a ton of protections before you have to take losses. Essentially, you would need a recession worse than that of 2008- likely much worse – in order to even see the common shares see a dividend reduction.

The dividend per share has been stable and growing since 2008. The company can always cut the common shares dividend in order to avoid default and continue to pay interest on the bonds. This is a key consideration.

Main Street Capital

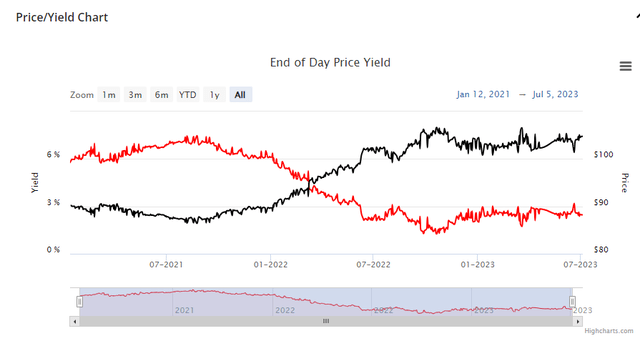

Here’s a chart of the price vs. yield of the bond:

FINRA

The recent increase in interest rates has pushed up the yield as the low coupon means investors rather put their money elsewhere. The bond matures in approximately three years, so the bond will return par ($100) at that point. So you capture that variance between the bond price ($88.16) and par over the next three years. In the meantime, you also collect the 3% coupon semi-annually.

Low coupon bonds are trading at a discount because investors rather invest in a 6% coupon bond that’s trading near par rather than a bond priced well below par with a low coupon. Income > cap gains to most investors.

For those investors who are indifferent between income return and total return (part income and part capital gain), you can earn slightly better returns in low coupon discount bonds relative to high coupon par, or premium bonds since investors favor the higher income with no capital gains versus low income plus capital gain.

Concluding Thoughts

The investment grade bond space is offering up a generational opportunity for investors to collect a 6%-plus return with lower risk. That lower risk, investment grade debt, was giving you less than 3% just two years ago. Today, many issues are yielding over 6% and in some cases, in the lower end of the investment grade space, you can find 7%-plus yields. That’s competitive with equities in terms of returns but with far less risk.

Read the full article here