Investment Overview

Waltham, Mass.,-based Viridian Therapeutics (NASDAQ:VRDN) shares have sunk by ~14% in trading today as the company announced “positive” topline clinical data from a low dose cohort of an ongoing Phase 1/2 clinical study of its candidate VRDN-001, an anti-insulin-like growth factor 1 receptor (“IGF-1R”) antibody, in patients with active thyroid eye disease (“TED”).

Viridian was founded in 2010, but joined the Nasdaq in January 2021 after completing a merger with miRagen Therapeutics, a troubled company that abandoned its entire RNA therapeutics program in favor of a full pivot to Viridian’s clinical programs, which are primarily focused on TED, although Viridian states in its Q321 10Q submission (quarterly report) that:

We target under-competitive disease areas where marketed therapies often leave room for improvements in efficacy, safety, and/or dosing convenience.

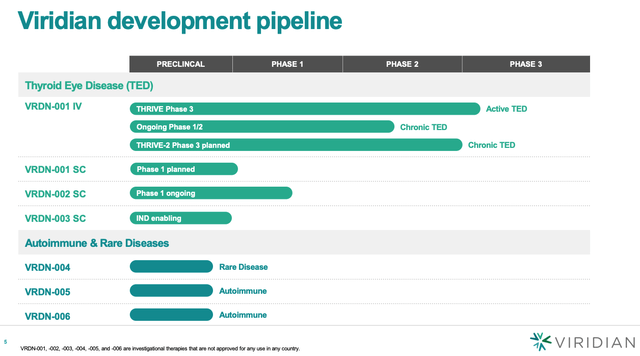

Viridian pipeline (Viridian investor presentation)

As we can see above, however, Viridian’s TED program – consisting of lead candidate VRDN-001 intravenously administered, which is currently progressing through 1 Phase 3 clinical trial, in active TED, with another planned in Chronic TED, plus a subcutaneous version of VRDN-001, and two further candidates – is the company’s only clinical program, and the key valuation driver.

What is TED? According to rarediseases.org:

Thyroid eye disease is a rare disease characterized by progressive inflammation and damage to tissues around the eyes, especially extraocular muscle, connective, and fatty tissue.

Thyroid eye disease is characterized by an active disease phase in which progressive inflammation, swelling, and tissue changes occur. This phase is associated with a variety of symptoms including pain, a gritty feeling in the eyes, swelling or abnormal positioning of the eyelids, watery eyes, bulging eyes (proptosis) and double vision (diplopia).

The active phase can last anywhere from approximately six months to two years. This is followed by an inactive phase in which the disease progression has stopped. However, some symptoms such as double vision and bulging eyes can remain.

According to Viridian, TED has “an annual incidence of approximately 19 in 100,000 people, which corresponds to over 60,000 patients in the United States.” The disease was typically treated with steroidal therapies off-label, until in 2020, when the Food and Drug Agency (“FDA”) approved Horizon Therapeutics’ candidate teprotumumab-trbw, which is marketed and sold as Tepezza. In its 2022 10K, Viridian discusses its chief competitor as follows:

At launch, Horizon Therapeutics plc announced a price of approximately $16,300 per vial of Tepezza which translates to a list price of approximately $375,000 based on patient weight for a six-month course of therapy. In the first three years following launch, Horizon Therapeutics plc reported full-year 2020, 2021, and 2022 net sales for Tepezza of $820.0 million, $1.66 billion, and $2.0 billion, respectively, in the first three years of launch.

The success and potential of Tepezza, which drove >50% of Horizon’s revenues in FY21, scarcely two years post launch, led to pharma giant Amgen (AMGN) launching a $28bn takeover bid for Horizon. Although the deal is subject to an FTC investigation, it speaks to the enormous revenue generating potential of a successful TED therapy.

No wonder, then that all eyes were on Viridian today as the company read out its latest study data.

What Did Viridian’s Thyroid Eye Disease Data Reveal

Viridian released its latest data – from its smaller, low-dose, Phase 1/2 study of just six patients, after six weeks – last night, but despite the apparently positive results, the market reacted negatively, and the company’s share price fell from ~$24.5 per share, to $20.5 (at the time of writing).

Viridian stated in a press release that it had observed:

Significant and rapid improvement in both signs and symptoms of TED after two infusions of 3 mg/kg, generally consistent with prior 10 and 20 mg/kg results

– Among 3 mg/kg VRDN-001 treated patients, 67% were proptosis responders, 56% were overall responders, 67% achieved a Clinical Activity Score (“CAS”) of 0 or 1, and 20% had complete resolution of their diplopia –

– Across all 21 VRDN-001 treated patients to date, 71% were proptosis responders, 67% were overall responders, 62% achieved a CAS of 0 or 1, and 54% had complete resolution of their diplopia, with a favorable safety profile seen across all dose levels –

Trial investigator Roger Turbin, M.D., Professor of Ophthalmology and Visual Science within the Department of Ophthalmology of Rutgers New Jersey Medical School, commented that the:

low dose of VRDN-001 reinforce previously reported findings in this trial, and suggest that VRDN-001 may offer a differentiated efficacy profile… The data also support development of VRDN-001 as a patient-friendly low volume subcutaneous injection, which could reduce the burden of care for patients suffering from TED.

The market’s issue with the data was based on Viridian’s not sharing data from the placebo arm of the study, which makes it harder to compare VRDN-001’s results against Tepezza, and made the market jittery – if the results vs placebo had been statistically significant, for example, Viridian would almost certainly have made that clear in its announcement.

With that said, the reductions in proptosis, or eye bulging, observed apparently compare favourably with Tepezza the same six-week time point, but it was also the case that 2 patients in the placebo arm of Viridian’s study met criteria for response in proptosis, while in an equivalent Tepezza study, the drug outperformed placebo in terms of mean reduction in proptosis, and proptosis responder rate.

Why Viridian Investors Don’t Need To Panic – Yet

Pharma and biotech investors are often kept largely in the dark by the companies they hold shares in, partly to protect them, and partly to protect the company’s share price. The problem with this approach is that when data is released, the market often overreacts, as may have been the case with yesterday’s data release.

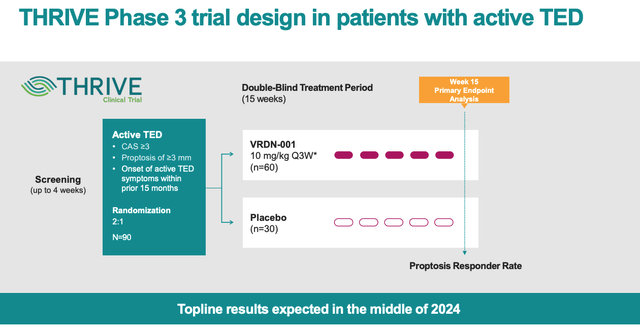

The reality is that there are much more significant data readouts to come – for example from the Phase 3 THRIVE study, which is enrolling 120 patients with active TED across 50 clinical trial sites in North America and Europe.

Nevertheless, Viridian did announce yesterday that it had amended the THRIVE study from an eight-infusion regimen to a five-infusion one, which management says “reflects our confidence in a 5-dose regimen and key stakeholder feedback.”

THRIVE Phase 3 study design (Viridian results presentation)

As we can see from the above slide from yesterday’s results presentation, however, topline results from this study will not be available until mid-2024. Meanwhile, data from the THRIVE-2 Phase 3 study – evaluating VRDN-001 in chronic TED – will not be initiated until next quarter, and topline data will not arrive until YE24.

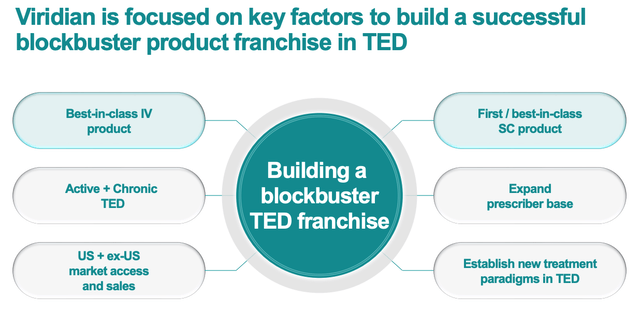

Viridian focused on TED franchise (Viridian presentation)

It’s also important to remember that Viridian wants to build a TED franchise, and while VRDN-001 is focused on intravenous administration, the rest of the franchise is focused on a subcutaneous version of the drug, which presents a much more convenient dosing regime.

Were Viridian’s Share Price Losses Today Justified?

Announcing its Q123 earnings results, Viridian reported a loss from operations of $72.5m, up from $25.89 in the prior year period, and a cash position of $374m – at this rate, the company’s funding runway may be exhausted by the end of 2024, leaving the company needing to raise further funding for a marketing push, assuming VRDN-001 is approved, which is far from certain.

Nevertheless, despite the possibility of dilutive at-the-market fundraisings coming Viridian investor’s way, analysts remain bullish on the stock – RBC Capital markets set a price target of $44 as recently as May, while BTIG believes Viridian stock at current value presents an “attractive entry point,” and carried a price target of $46.

The company’s current market cap is $884m, which is a far cry from the $23.5bn market cap valuation that Horizon enjoys, although it should be noted that Horizon is subject to an M&A deal and has a variety of other commercialized assets besides Tepezza, as well as a strong pipeline.

Viridian is not the only rival to Horizon – in its 2022 10K submission the company evaluates its competition as follows:

•ACELYRIN, INC. is developing Lonigutamab (VB-421), a subcutaneously delivered anti-IGF-1R currently being evaluated in a Phase 1 study for TED.

•argenx is developing efgartigimod (Vyvgart®), an antibody fragment to target the neonatal Fc receptor (FcRn) expected to be evaluated in a registrational Phase 3 trial in patients with TED.

•Immunovant and Harbour BioMed are developing batoclimab (IMVT-1401/HBM9161), a monoclonal antibody targeting FcRn currently being evaluated in an ongoing Phase 3 trial in patients with TED.

•Sling Therapeutics, Inc. is developing linsitinib, a small molecule IGF-1R inhibitor currently be evaluated in an ongoing Phase 2b LIDS clinical trial in patients with active, moderate-to-severe TED.

On the one hand, Viridian may be within two years of commercializing a rival to a >$2bn per annum selling drug that analysts believe could generate >$4bn in peak annual sales. If Viridian is successful, it’s hard to see how its share price does not rise substantially to meet peak sales expectations – a $3 – $5bn market cap valuation would not flatter a company with a seemingly nailed on blockbuster in its product portfolio.

On the other hand, the market is clearly discounting Viridian’s share price on account of the risks in play. Data has been inconsistent, with management drip-feeding investors as opposed to presenting full data sets. Money is relatively tight given the high costs of pivotal studies, and if VRDN-001 does not deliver the data required to secure an approval – likely in late 2025 – the value of its remaining assets tumbles, and its share price is likely to drop by substantially more than 50%.

Concluding Thoughts – Could Be Better, Could Be Worse – Only Time Will Tell

One of the excitements of investing in biotech companies developing new drugs is that valuations have tremendous upside, and downside potential, given the market always factors the risks of both failure and success into valuations.

If VRDN-001 is approved, then of course Viridian’s share price will skyrocket given TED is a multi-billion market in which Viridian’s drugs could take meaningful market share. If the drug does not deliver the data required by the FDA, the European Medicines Authority (“EMA”), or any other regional authority, to gain approval for commercial use, the company will have wasted billions of dollars of investors’ money and its portfolio will scarcely be worth $100m, let alone >$1bn.

Today’s price movements reflect that reality – with investors using every data readout – no matter how small of guarded – to make adjustments to their bets and try to beat the market.

Would I bet my hard-earned savings on Viridian succeeding with VRDN-001 and creating a multi-billion dollar TED franchise? In all honesty, I would likely not, as I would be concerned about the focus on a single disease indication, and the length of time to a likely approval when there is so much competition. I also do not like the look of Viridian’s finances, and frankly, I simply believe there are plenty of opportunities out there with a superior risk / reward profile.

That doesn’t mean that a positive THRIVE Phase 3 data readout will not send Viridian’s stock price soaring however – it undoubtedly will – if you are betting money you cannot afford to lose, however, the odds on that happening may not be favorable enough to take the plunge. Only time will tell.

Read the full article here