Compagnie Financière Richemont (OTCPK:CFRHF), the owner of worldly renowned brands like Cartier, Montblanc, Van Cleef & Arpels, and Piaget, trades at a discount compared to the top tier of the luxury industry, and at a premium compared to the bottom tier.

The company has been relying on the strength of its signature Maisons to reach record revenues and profits in FY23 and has been focusing on improving its group after the LVMH (OTCPK:LVMHF) takeover threat has dwindled.

I find Richemont to be on a tier of its own in luxury, not as high as LVMH and Hermès (OTCPK:HESAY), and not as low as Kering (OTCPK:PPRUF) and Burberry (OTCPK:BBRYF). With decent growth prospects and a reasonable valuation, I rate the stock a Buy ahead of earnings.

—

With the end of July approaching, almost every luxury house in the world is set to report its financial results for the first half of 2023. For those interested in reading previous articles I wrote about companies in the industry, here are the links:

- LVMH: 2023 Should Be Another Stellar Year, It’s A Buy

- LVMH: Q1 Numbers Show No Sign Of Slowing Down

- Capri Holdings: It’s A Value Trap, But A Likely Takeover Candidate

- Tapestry: It’s Not Luxury, But It Is An Attractive Investment

- Hermes: Unjustified Historically-High Premium Over LVMH

I plan to write a pre and post-earnings article on every luxury house. Stay tuned.

Company Overview

Richemont is one of the world’s leading luxury goods groups. The Group’s luxury goods interests encompass some of the most prestigious names in the industry, including Buccellati, Cartier, Van Cleef & Arpels, A. Lange & Söhne, Baume & Mercier, IWC Schaffhausen, Jaeger-LeCoultre, Panerai, Piaget, Roger Dubuis, Vacheron Constantin, Alaïa, AZ Factory, Chloé, Delvaux, Dunhill, Montblanc, Peter Milar, Purdey, Serapian, and Watchfider & Co.

Richemont Group Presentation, May 2023

The group was founded by Johann Rupert in 1988, as a spin-off of his father’s Rembrandt Group, which was founded in 1940. Almost four decades later, 73-year-old Johann is still the chairman of the group, holding 9.1% of the company’s equity, and controlling 50% of the company’s voting rights.

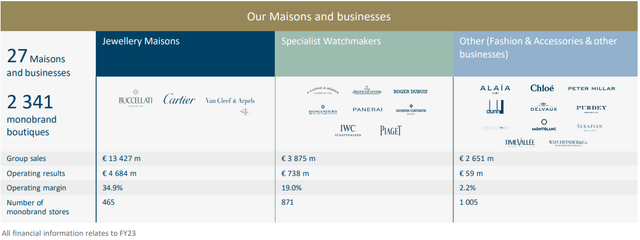

Today, Richemont employs over 33,000 people, across 27 maisons, with more than 2,341 mono-brand boutiques in over 150 markets.

Richemont Company Snapshot, May 2023

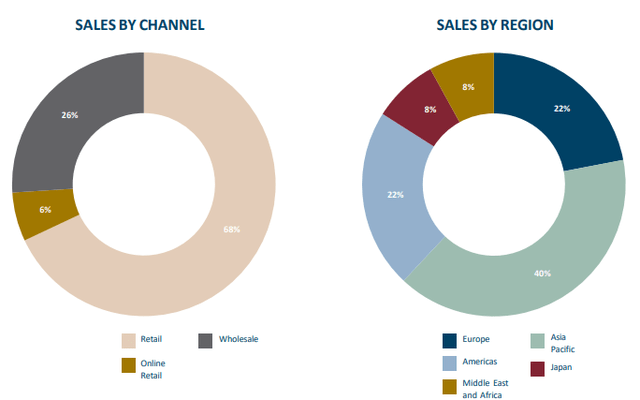

As we like to see, most of the group’s sales are derived from its owned and operated retail stores, with only 32.0% of sales coming from wholesale and online. This is one of the first foundational metrics to look at with a luxury group, as it’s directly linked to the company’s profitability, and brand value.

Regarding geographic exposure, 48% of the company’s sales are generated in Asia (including Japan). This is more than LVMH, which generated 37% of its sales in Asia, and less than Hermès, which generates almost 58.0% of its sales in the region. One thing to take in mind here is that Richemont’s fiscal year ends in March, which means its numbers are not perfectly comparable to the French giants, but we’ll have to make due.

Operating Segments

Richemont aggregates its results under three reported segments: Jewellery Maisons, Specialist Watchmakers, and Other. Previously, the group had a fourth Online Distributors segment, which included YNAP and Watchfinder. After announcing plans to divest YNAP, it was reclassified as discontinued operations and Watchfinder is now aggregated under Other.

Richemont Company Snapshot, May 2023

As we can see, Jewellery Maisons is by far the largest segment, generating 67.0% of sales, and more than 85.0% of operating profit. Second, comes Specialist Watchmakers, responsible for 20.0% of sales, and 13.4% of operating profit. Last is Other, with 13.0% of sales and only 1.0% of operating profit.

It’s important to note that in reality, the Jewellery Maisons and Specialist Watchmakers segments are separated mainly based on the strength of the business, and not because of a materially different product mix. For instance, Cartier is one of the most successful watchmakers in the world, and Piaget is a jewelry brand just as much as it is a watch brand.

Jewellery Maisons

The Jewellery Maisons segment aggregates businesses whose heritage is in the design, manufacture, and distribution of jewelry products. These comprise Buccellati, Cartier, and Van Cleef & Arpels. This segment operates a retail network of 465 stores, of which 272 belong to Cartier, 150 to Van Cleef, and 43 to Buccellati.

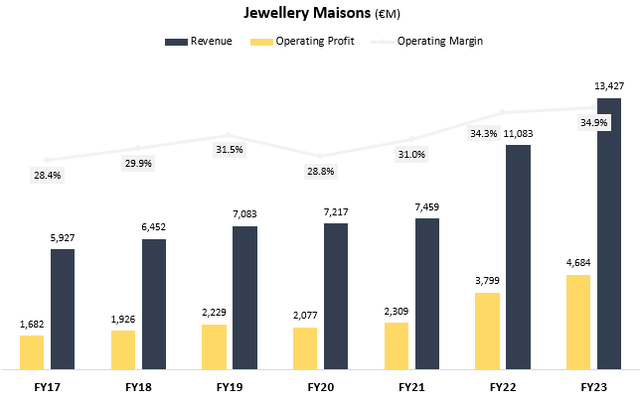

Created and calculated by the author using data from Richemont financial reports.

Jewellery Maisons is by far the top-performing segment of the group, growing at a 14.6% CAGR between FY17-FY23, and achieving all-time high operating margins last year, with 34.9%. In FY23, the segment generated €28.8M in sales per store. Within the segment, Cartier is the major contributor and should continue to outperform with its vast retail network.

Specialist Watchmakers

The Specialist Watchmakers segment includes businesses whose primary activity includes the design, manufacture, and distribution of precision timepieces. The Group’s Specialist Watchmakers comprise A. Lange & Söhne, Baume & Mercier, IWC Schaffhausen, Jaeger-LeCoultre, Panerai, Piaget, Roger Dubuis, and Vacheron Constantin. This segment operates a retail network of 871 stores.

Created and calculated by the author using data from Richemont financial reports.

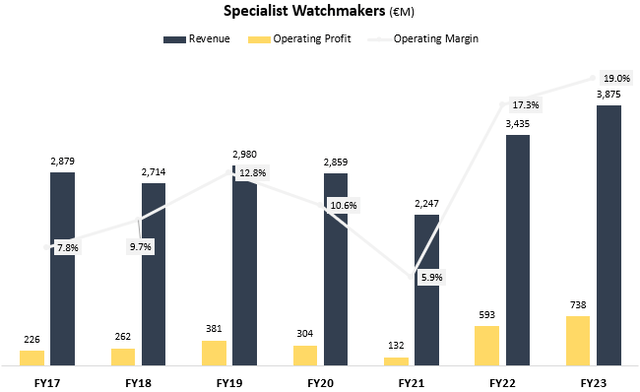

As we can see, Specialist Watchmakers lags behind its Jewellery Maisons, as watches, in general, are a less profitable business compared to jewelry. With a 19.0% operating margin, Richemont’s watch businesses are in line with LVMH’s Watches & Jewelry, reflecting the strength of the Richemont group.

Still, this segment’s performance is way behind Jewellery Maisons, with revenue growing at just a 5.1% CAGR between FY17-FY23. Furthermore, the segment generated €4.4M in sales per store, which is 15% of Maison store.

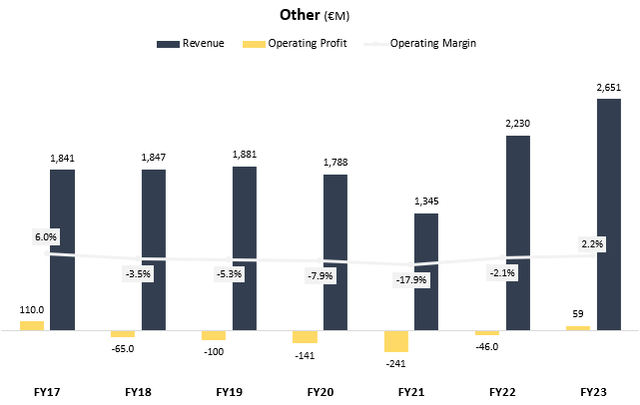

Other

Other operating segments include Alaïa, AZ Factory, Chloé, Delvaux, Dunhill, Montblanc, Peter Millar, Purdey, Serapian, Watchfinder, investment property companies, and other manufacturing entities. This segment operates a huge retail network of 1,005 stores, of which 563 belong to Montblanc and 218 belong to Chloe.

Created and calculated by the author using data from Richemont financial reports.

As we can see, the Other segment is the ugly duckling in the group and has been operating at a loss for the majority of the last 7 years. And while the group is trying to improve the businesses which are piled under this segment, the efforts have been underwhelming.

The segment generates a miserable €2.6M in sales per store, with barely any profit. We can see the company is slowly shutting down locations, but not at a significant pace. Thus, I wouldn’t have high hopes for the Other segment to improve in the foreseeable future.

The Turnaround Story

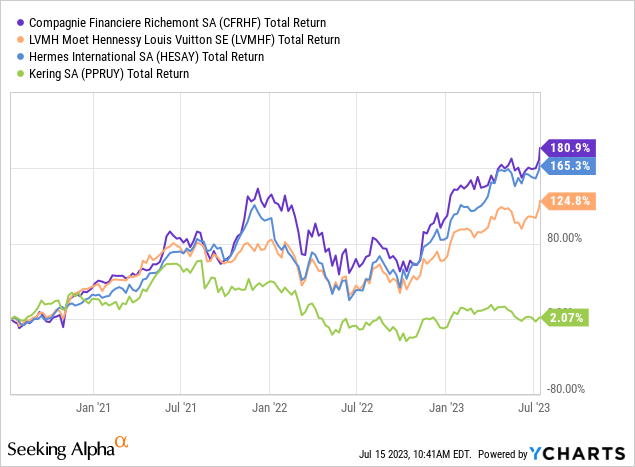

Over the last three years, Richemont has outperformed its luxury peers with a 180.9% total return. While such performance could suggest it has performed better, in reality, the outperformance is the result of a way lower starting point, as the company experienced a major selloff three years ago due to a combination of the Covid outbreak and its YNAP business generating significant losses.

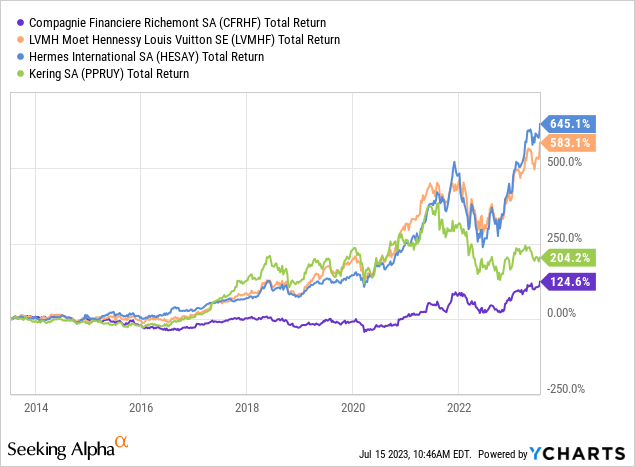

At a longer time horizon, we can understand that Richemont has actually been a very poor investment over the last decade, trailing even the notorious Kering group.

The bad performance didn’t go unnoticed, and rumors have surfaced about an LVMH takeover. Furthermore, a person closely associated with LVMH, and specifically Bernard Arnault, was close to getting a seat on Richemont’s board, an effort that was blocked by the group’s founder in a very straightforward letter to shareholders prior to the 2022 Annual General Meeting.

In 2023, with the combination of the takeover rumors resurfacing, the announcement of the YNAP divestiture, and double-digit growth in most geographies, the stock surged and now trades at all-time highs.

Now What?

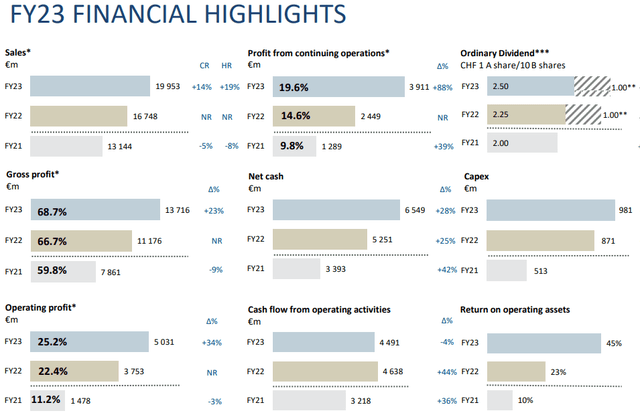

In FY23, Richemont’s revenues grew by 19.1%, and operating margins came in at 25.2%, which is an all-time high. Excluding discontinued operations, Net Income amounted to €3.9M, reflecting a 19.6% margin, near all-time highs as well. Clearly, the company’s performance has been impressive and demanded a rerate in the stock’s price.

Richemont Fiscal 2023 Results Presentation

But, that belongs to the past. The question is whether Richemont has more room to grow, and is there still room for upside for shareholders.

Growth Prospects

Richemont has a different value proposition compared to other luxury giants in LVMH and Hermès. For Hermès, the mono-brand prestige and unattainability is what drives immense demand. For LVMH, it’s unparalleled marketing, partnerships, and creativity, as well as mono-brand prestige.

For Richemont, the Jewellery Maisons segment is similar to Hermès in the way that it’s not creative marketing that drives performance, rather than mono-brand desirability, specifically in Hermès. For the other segments, it’s a mixture, but they are clearly not of the same quality from an investment perspective. Therefore, when assessing the group’s growth prospects, we have to acknowledge the differences between its segments.

In Jewellery Maisons, I expect continued growth at a double-digit pace, with operating margins remaining at current levels of 34%-35%. This will be driven by continued store openings, recovery in China, and market growth.

In Specialist Watchmakers, I expect growth to decelerate moderately, and margins to remain high, as the over-achieving consumer begins to weaken.

In Other, there are a lot of unknowns. I don’t see a reason why all of a sudden, brands that the company held for decades will see a turnaround under the same management. The YNAP divestiture shows me that management is seeking better focus and efficiency, and the beginning of a narrowing down process in the number of lChloe and Montblanc locations is also a step in the right direction. Still, I wouldn’t expect this segment to achieve better than a mid-single-digit profitability any time soon, and growth should settle around the mid-to-high single-digit range.

Relative Valuation

So the turnaround growth spurt is behind us. From now on, I expect the group to steadily accumulate value, as its growth prospects materialize. Let’s try to understand if the stock is still undervalued with respect to its improved fundamentals.

Created by the author using data from Seeking Alpha and the author’s projections; Data as of July 15th, 2023.

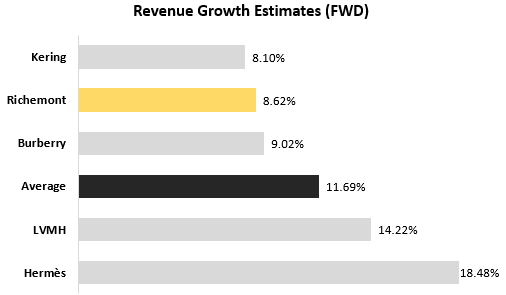

Regarding future growth, current analysts’ estimates put Richemont in the bottom tier in terms of revenue growth, expecting 8.6% growth in CY24. My estimates are a little above that, but they are still way below the likes of LVMH and Hermès.

Created by the author using data from Seeking Alpha and the author’s projections; Data as of July 15th, 2023.

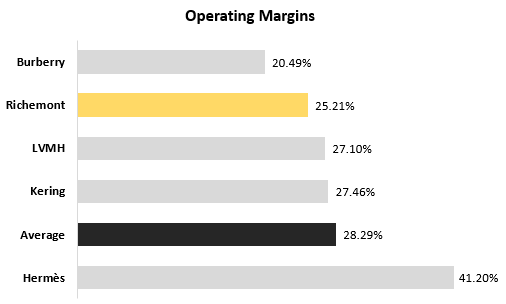

Furthermore, Richemont is lagging LVMH, Hermès, and Kering in terms of operating margin. Now keep in mind that LVMH is involved in lower margin activities like selective retailing, and Kering is more exposed to apparel rather than jewelry, and you get the sense that Richemont’s margins should improve.

Created by the author using data from Seeking Alpha and the author’s projections; Data as of July 15th, 2023.

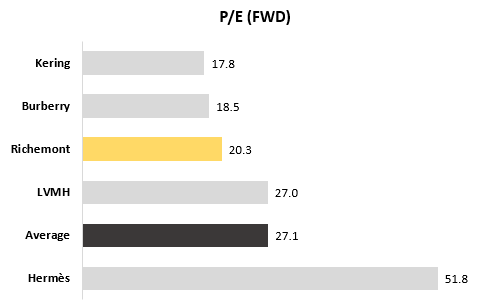

Looking at the current forward P/E multiple, Richemont is trading at 20.3x, which is right in the middle between the top-tier (Hermès and LVMH), and the bottom-tier (Burberry and Kering). In my view, right in the middle is exactly where Richemont should be, as it’s fundamentally better than the bottom tier, but its growth prospects, margins, and overall brand quality is inferior to the top tier.

Valuation & Financial Model

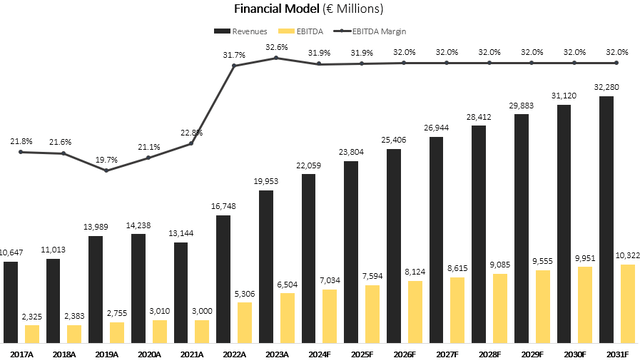

I used a discounted cash flow methodology to evaluate Richemont’s fair value. I forecast the group will grow revenues at a 5.6% CAGR between 2024-2031 due to constant price increases, continued store openings, improved performance of lagging brands, recovery in China, and steady organic growth.

I project EBITDA margins will increase gradually up to 32.0% in 2031. In my view, this is a reasonable projection as the company should be able to improve operating margins of lagging businesses, which will be offset by lower amortization and depreciation as it closes stores and there are its write-offs decelerate.

Created and calculated by the author based on data from Richemont financial reports and the author’s projections.

Taking a WACC of 8.2% and adding its net debt position, I estimate Richemont’s fair value at €171.8 per share, which amounts to $199.7 per CFRHF ADR based on the current USD/EUR ratio. This represents an 11.6% upside compared to the market price at the time of writing.

Conclusion

Richemont’s turnaround story is over, as the company discontinued its unprofitable YNAP business, and fully recovered from Covid. The next leg up will be fueled by continued execution in its Jewellery Maisons and Specialist Watchmakers segments. On the contrary, Improvement in the lagging Other businesses is doubtful, as the company owned them for years and had shown no ability to revive them.

I find the company’s growth prospects not as impressive as peers like LVMH and Hermès, and thus believe it’s lower valuation is reasonable. That being said, I estimate there’s still decent upside, and rate the stock a Buy.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here