Investment thesis

Our current investment thesis for Moncler (OTCPK:MONRF) is that it is a well-managed business on an impressive growth trajectory, driven by brand hype, cultural integration, and successful innovation. Moncler has market-leading margins, with an EBITDA-M of 33%. Industry tailwinds and the acquisition of Stone Island should support the continuation of growth, while economic conditions look to have a mild impact on the business. Moncler looks appropriately priced but we believe upside is present if it continues its current performance.

Company description

Moncler is a renowned Italian luxury fashion brand, specializing in the design, production, and distribution of high-end outerwear and accessories. With a rich heritage and commitment to craftsmanship, Moncler has become synonymous with premium quality, functionality, and style.

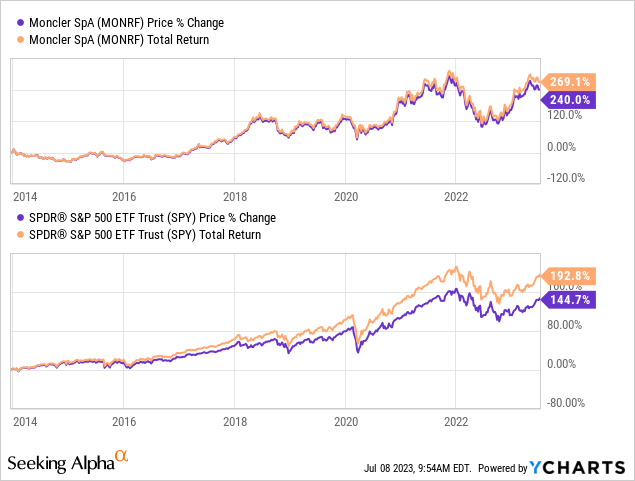

Share price

Moncler’s share price has performed extremely well since the stock was listed, outperforming the S&P. This is a reflection of its strong financial development throughout the period, shaping the business to be a top performer in the industry.

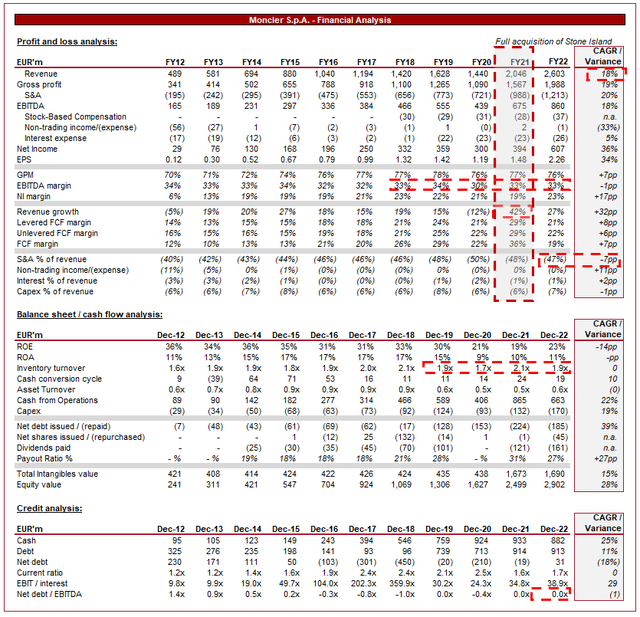

Financial analysis

Moncler financials (Capital IQ)

Presented above is Moncler’s financial performance for the last decade.

Revenue & Commercial Factors

Moncler’s revenue has grown at a CAGR of 18% across the last 10 years, an incredible achievement that is driven primarily by the Moncler brand. In the last 10 years, only Covid has contributed to a revenue decline, with the other periods in excess of 15%.

Business Model

Moncler’s core business revolves around the creation of luxury down jackets, parkas, and related accessories, blending fashion and performance. The company’s focus has been on the production of high-quality products, alongside fashion-forward designs to cater to a younger generation.

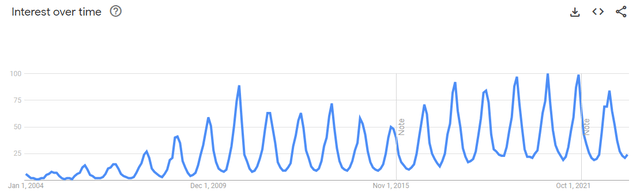

Moncler has benefited heavily from its strong engagement in the hip-hop and streetwear communities, with many rappers and public figures seen sporting their jackets. During the historical period, both hip-hop and streetwear experienced an impressive upward trajectory, becoming mainstream leaders in their respective industries. Moncler’s alignment has allowed it to enjoy growth while positioning the business for long-term success. As the following illustrates, Moncler’s brand has slowly improved its global interest, peaking in recent years.

Moncler (Google Trends)

Given the hype around the brand is built on its jackets, Management has correctly identified the need to innovate, expanding its product range to include knitwear, footwear, eyewear, and fragrances, capitalizing on its brand equity and customer loyalty. Management has been intelligent with the development of these products, creating “Moncler Genius”, a separate clothing line purely comprising one-off collaborations. This creates buzz around its various clothing products through scarcity, improving the marketing of its apparel.

In the last year, Moncler has increased its focus on footwear, launching several products including the Trailgrip GRX and Gaia Pocket Mid. This has seen strong interest, developed with extreme conditions in mind, with the Trailgrip GTX representing its most successful launch ever and has been awarded the best footwear release of the year by Techunter.

Moncler operates through a combination of company-owned stores, concessions, and wholesale partnerships to reach global customers. This is vital for its ability to efficiently reach consumers, given its relatively small size in the fashion industry. The strength of the brand in recent years has allowed the business to focus on its own channels, curating the customers’ experience.

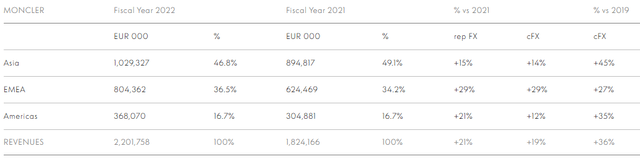

Moncler generates the majority of its revenue from Asia, a common occurrence for luxury brands. We believe the level is healthy, although any further could pose a risk of over-reliance. Demand from countries such as China has grown rapidly in the last decade but it is uncertain as to whether this can sustainably increase over the coming years, we are hesitant.

Sales by region (Moncler)

Management’s diversification efforts are not just in products but also brands. In 2021, Moncler acquired the remaining 30% of Stone Island for $419m. Stone Island has experienced a similar rise to Moncler but is far more focused on traditional apparel such as jumpers. We believe the two businesses are highly complementary from an operational perspective, while offering the market a different proposition.

Competitive Positioning

We believe Moncler has three key competitive advantages.

Firstly, and most importantly, both Moncler and Stone Island enjoy a prestigious reputation as a symbol of luxury and craftsmanship. Both have managed to channel their hype into sustainable demand through the creation of equally attractive products and consistent incremental innovation.

Secondly, the company has developed its operational capabilities, enhanced further through the acquisition of Stone Island. The benefits to the company are production scale, global reach through outlets, and design talent for driving innovation.

Finally, we believe Management is very talented. Canada Goose (GOOS) is a comparable business to Moncler, having experienced similar hype to Moncler through its jackets. Canada Goose is struggling with sliding margins and growth as its reliance on jackets is punishing the business. Moncler on the other hand has intelligently diversified its business rapidly and is already increasing the number of brands under its umbrella. Management is clearly acutely aware of the areas of development required, as well as identifying effective ways to achieve its goals.

Luxury Industry

Brands differentiate through design aesthetics, craftsmanship, brand heritage, and marketing campaigns. Moncler currently competes with other luxury fashion brands, such as Canada Goose, Burberry (OTCPK:BURBY), Prada (OTCPK:PRDSY), LVMH (OTCPK:LVMHF), and Gucci (OTCPK:PPRUF), in the premium outerwear segment. Moncler’s key focus has been to develop the first three items listed above relative to peers, having grown through the 4th point.

The luxury apparel industry has been growing well, with increasing affluence and aspirational lifestyles driving demand for luxury fashion and accessories. We are living in a social media era, with individuals increasingly influenced by the lifestyle of others. This looks to be a compounding trend with no real evidence of a slowdown, despite economic conditions.

Consumers are more conscious of the environmental impacts of their possessions, influencing purchasing decisions and thus favoring brands with sustainable practices. Moncler has topped S&P Global’s sustainability assessment for 4 years in a row, cementing its position as one of the leading sustainable options in luxury. As the societal value placed on sustainability increases, we believe Moncler will be positioned well to enjoy.

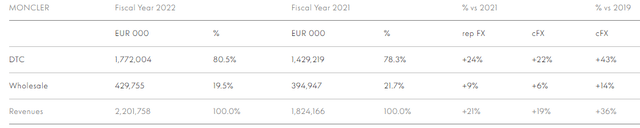

Online sales channels continue to expand, as e-commerce is increasing the favored medium for purchasing. The development of direct-to-consumer capabilities has been crucial for the improvement of sale economics, as brands look to cut out the wholesale middleman. Moncler performs extremely well in this regard, with over 80% of its sales through DTC. This is an impressive achievement for the business given its size. This has been partially supported by the creation and optimization of its app/website, with online members increasing by over 120%. We believe a continuation of this trend will drive further value for the business.

Revenue by distribution channel (Moncler)

We believe Moncler has two key opportunities in the coming years.

Moncler is positioned well to capitalize on the strength of its brands by expanding into emerging markets, which are seeing an ever-increasing middle class looking to buy Western luxuries.

Further, following the acquisition of Stone Island, Moncler is in a position to acquire additional brands to supplement its organic growth. Given the strong operational and commercial capabilities on display, we believe this can be accretive.

Economic & External Consideration

With rising living costs due to high inflation and higher borrowing rates, consumers may be discouraged from making large purchases, particularly on discretionary products such as apparel.

However, we have seen impressive resilience from luxury brands, with most able to increase prices beyond any inflationary pressures. The target market for luxury goods consists of individuals who have the financial means to withstand the current economic conditions, in conjunction with high employment and moderate wage inflation.

Therefore, we are not overly concerned about a significant slowdown in revenue growth, although growth may transition to a mild level, such as low single digits.

Margins

Moncler has quite attractive margins. The company has a GPM of 76% and an EBITDA-M of 33%. Across the historical period, GPM has improved while EBITDA-M has remained flat.

This GPM improvement is due to the rapid increase in scale, allowing the business to benefit from economies of scale. This has been offset by an increase in S&A spending, which has increased from 40% of revenue to 47%.

The increased S&A spending implies the company spent a considerable amount to generate revenue growth, unable to make this accretive. Although looks concerning, its EBITDA-M is so large that flat margins with scale are not overly problematic. The concern will come only if S&A continues to grow while GPM does not.

Balance sheet & Cash Flows

Moncler is conservatively financed, with ND and EBITDA parity. This gives the business sufficient flexibility to fund M&A if required.

Inventory turnover has not materially changed from its pre-Covid levels, implying no material slowdown in demand despite current conditions and price hikes.

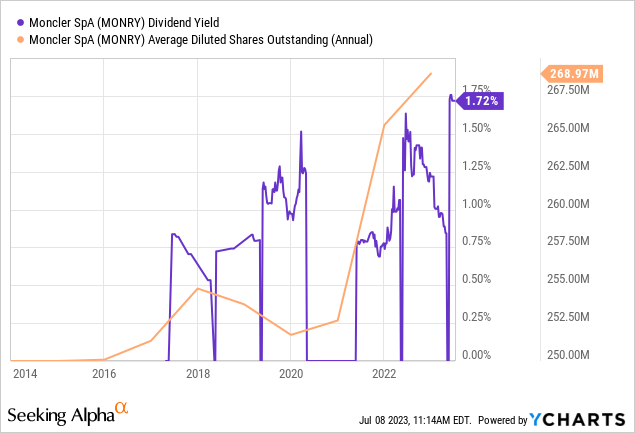

Distributions have been relatively consistent, with a current dividend yield of 1.7%. Given the price action, we consider this an attractive yield.

Outlook

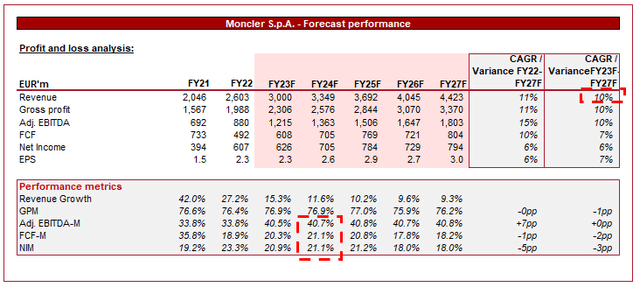

Outlook (Capital IQ)

Presented above is Wall Street’s consensus view on the coming 5 years.

Analysts are forecasting a continuation of its impressive growth trajectory, with a 10% average rate into FY27F. This looks to be a reasonable estimate, especially as Stone Island develops in the group.

Further, margins are expected to improve by a considerable amount, a bullish assessment by analysts. This is likely due to the strong Q1 results, with sales up 23%.

Industry analysis

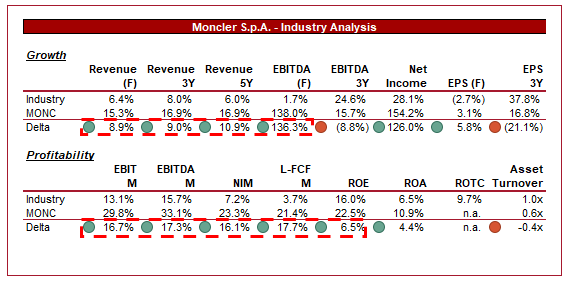

Apparel, Accessories and Luxury Goods industry (Seeking Alpha)

Presented above is a comparison of Moncler’s growth and profitability to the average of the Apparel, Accessories and Luxury Goods industry, as defined by Seeking Alpha (33 companies).

Moncler performs extremely well relative to these businesses. Its growth and margin delta is more than double the cohort, reflecting the superiority of the business.

In order to avoid nitpicking, we can also consider it on a head-to-head basis. LVMH and Kering have an EBITDA-M of 30% and 31%, respectively (Only Hermes (OTCPK:HESAY) has a higher EBITDA-M), while only Lululemon (LULU) has grown its revenue at a faster rate over the last 5 years.

Based on this, we believe Moncler should trade at a premium valuation to reflect its financial performance.

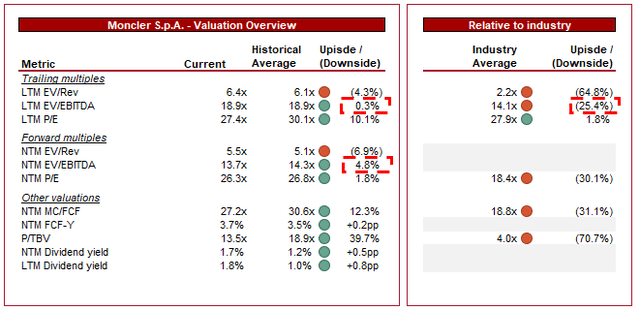

Valuation

Valuation (Moncler)

Moncler is currently trading at 19x LTM EBITDA and 14x NTM EBITDA. This is a discount to its historical average.

Interestingly, Moncler is trading at a small discount to its historical average, likely punished by the lack of margin improvement and economic conditions. This said, we believe there is significant value in the fact additional scale has been achieved, revenue is far more diversified (including by brand), and industry tailwinds continue to be present. Further, with Q1 growth up 23% and analysts guiding 15% on the top-line, we see no reason to be concerned about near-term performance.

Relative to peers, Moncler is trading at a 25% LTM EBITDA premium and a 30% NTM P/E premium. This valuation looks more appropriate compared to its historical trading range, as we would suggest a 25-30% premium is justifiable.

Given the financial improvement achieved thus far and the positive trajectory, we are more inclined to suggest the business is slightly undervalued, especially given the strength of demand in Q1.

Key risks with our thesis

The risks to our current thesis are:

- Diversification. Despite the acquisition of Stone Island and its product development, it remains uncertain as to how diversified the business is. SI currently represents c.17% of revenue and Moncler does not disclose sales by product type.

- Changing trends. Trends in fashion can change quickly, leaving the business susceptible to changing interests.

Final thoughts

Moncler is a well-run business in the process of establishing itself as a leading player in the luxury segment. Growth has been fantastic and margins remain in the top quartile. Our expectation is a continuation of strong growth is ahead, supported by industry tailwinds and innovation.

The company’s valuation is sending slightly mixed signals but given the positive trajectory, we believe a soft buy is warranted.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here