Investment thesis

Enbridge (NYSE:ENB) offers a stellar above 7% forward dividend yield. My analysis suggests that the dividend is safe and sustainable. Amid the softening momentum in the oil and gas industry, the company suffers a substantial YoY decline in revenue. But ENB is a value stock, and sustaining profitability is the most important for the company. The company’s profitability metrics demonstrate impressive resilience in the unfavorable environment; to me, it is a solid bullish sign. Lastly, my valuation analysis suggests the stock is very attractively valued.

Company information

Enbridge Inc. is a leading North American energy infrastructure company. ENB has six operating segments: Liquids Pipelines, Gas Transmission & Midstream, Gas Distribution & Storage, Renewable Power Generation, and Energy Services.

The company’s fiscal year ends on December 31. According to the latest 10-K report, revenue from commodity sales comprised about 54% in FY 2022, while the transportation and other services portion comprised approximately 34%.

Financials

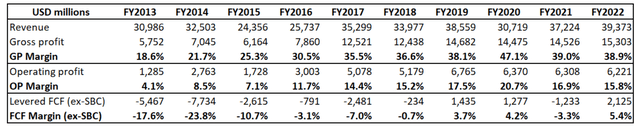

Due to the company’s well-diversified business, the company demonstrated solid profitability metrics even during hard times for the oil and gas industry as a whole. I like that over the past decade, profitability metrics have improved significantly. The business is very capital intensive, and the company invested heavily in CAPEX in the first half of the past decade, which is why the levered free cash flow [FCF] was consistently negative.

Author’s calculations

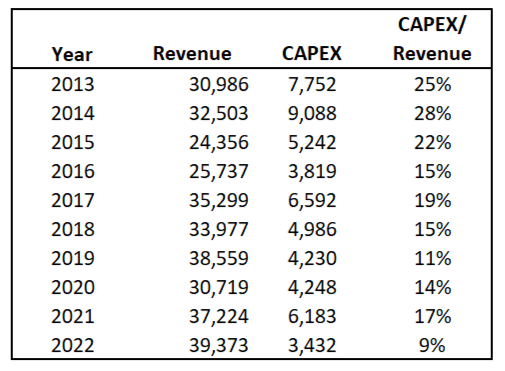

Below you can see that in FYs 2013-2015, the company reinvested into CAPEX about every fourth dollar it generated in sales, which is a massive level. But since then, the CAPEX to revenue ratio has moderated, I believe that the above 7% dividend yield the stock offers is safe and sustainable.

Author’s calculations

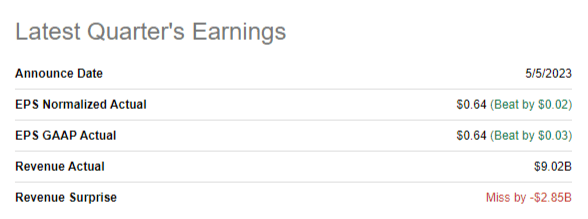

This year, the company’s earnings weakened notably after a massively successful FY 2022 for the whole Energy sector. The latest quarterly earnings were released on May 5, and the company substantially missed the top-line consensus expectations. Revenue demonstrated a 23% YoY decline. The weaker-than-expected performance reflected weaker results in the Renewable Power Generation business, lower commodity prices, and losses on foreign exchange hedges. All these unfavorable factors did more than offset more robust results in the remaining lines of business.

Seeking Alpha

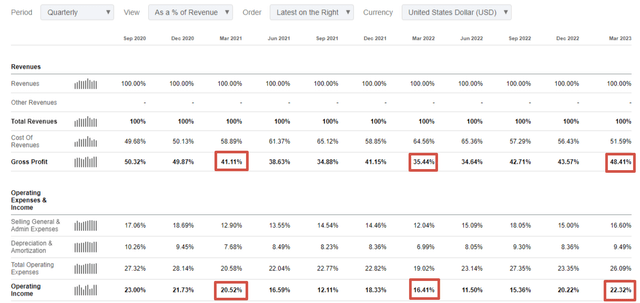

Investors were very disappointed by the company’s massive revenue miss, which led to a stock selloff. I think the market overreacted because the company’s performance in managing the weakening revenue was stellar. Despite significantly weakening revenue, Enbridge demonstrated a stellar improvement in profitability metrics.

Seeking Alpha

It is also crucial that the management reiterated its guidance with an adjusted EBITDA of $16.2 billion at the midpoint of the provided range. It is better than the past fiscal year with its $15.5 billion adjusted EBITDA. To me, this looks very impressive amid the softening Energy sector.

Enbridge’s balance sheet looks below average, with a substantial leverage ratio and liquidity ratios notably lower than one. On the other hand, the nature of business requires vast capital resources, and high leverage with low liquidity ratios is typical. It is essential to underline that the company’s debt has an investment-grade rating from all the most prominent credit agencies.

The upcoming quarter’s earnings will be released on August 4, with revenue expected to decline 15% YoY. The Energy sector is cyclical, and the decline in revenue is average, especially given the very high comps. In my opinion, it is crucial that the company sustains profitability levels even with a substantial revenue decline. The adjusted EPS is expected by consensus at $0.51, which is only a cent lower than the prior year’s Q2, with the revenue higher by 15%. ENB is not a growth company; profitability matters most to sustain its high dividend yield.

Valuation

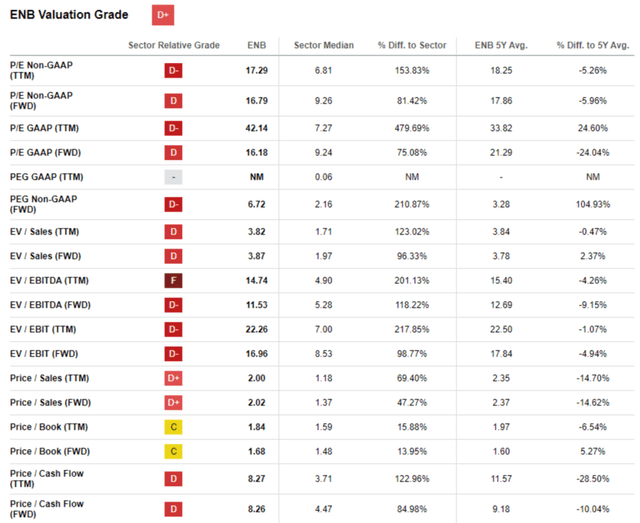

This year, the stock underperformed the broad market with about a 6% year-to-date price decline. The performance was also slightly behind the Energy sector (XLE), demonstrating a 3.5% decline year-to-date. ENB has a poor “D+” valuation grade from Seeking Alpha Quant due to substantially higher multiples than the sector median. On the other hand, across most of the board, current valuation ratios are lower than the company’s 5-year averages.

Seeking Alpha

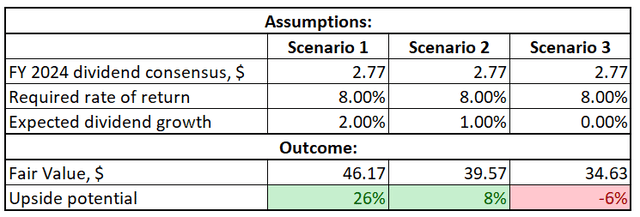

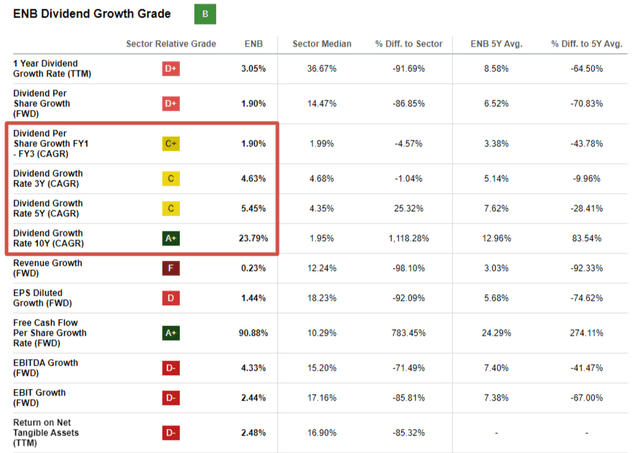

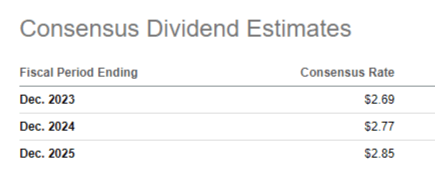

The company’s forward 7.16% dividend yield definitely stands out from peers, and I would like to proceed with my valuation analysis with a discounted dividend model [DDM] approach. Valueinvesting.io suggests that Enbridge’s WACC is close to 8%, which I consider fair. Dividend consensus estimates forecast FY 2024 dividend at $2.77. The dividend growth rate is always tricky, especially for oil and gas companies which significantly depend on the hardly predictable commodities market. The company has the weakest possible “F” dividend history grade from Seeking Alpha, pointing to payout instability. Therefore, I would like to simulate three very conservative scenarios of dividend growth, one of which assumes zero growth.

Author’s calculations

As you see, the model is susceptible to the dividend growth rate. I think the stock is valued rather attractively because a 2% growth rate looks doable for Enbridge if we trace back to the historical dividend growth rate. And even with no dividend growth, the downside potential is limited.

Seeking Alpha

To sum up, Enbridge’s valuation looks attractive even if the company delivers a mere dividend growth rate in the upcoming years. Dividend consensus estimates suggest that the payout will grow between FY2024 and FY2025.

Seeking Alpha

Risks to consider

Apart from a solid dividend yield and attractive upside potential, investors should also be aware of risks related to investing in ENB.

Enbridge’s financial performance heavily depends on fluctuations in commodity prices, which is out of the company’s control. Commodity markets, especially oil and gas markets, are very dependent on political and geopolitical trends which are hard to forecast. Commodity price volatility affects the volumes and tariffs associated with transportation and storage. At the end of the day, this will affect Enbridge’s earnings.

The company faces significant environmental risks, which are inherent to ENB’s operations. Risks relate to potential environmental incidents, which can include oil spills and leaks. This in turn might lead to damage to reputation and litigations with penalties.

The business the company conducts is heavily capital-intensive. Any unforeseen maintenance or repair works might lead to unplanned substantial CAPEX. Capital repairs also will lead to idle time or a temporary decrease in capacity which will ultimately damage the company’s earnings.

Bottom line

To conclude, ENB is a “Strong Buy”. I think an above 7% dividend yield is a gift for a company like Enbridge. The company has a vast, diverse infrastructure, and historical performance suggests that ENB can deliver solid profitability metrics even amid a very challenging environment for the Energy sector. It is also important to emphasize that apart from a stellar dividend yield, the current stock price offers a very attractive upside potential.

Read the full article here