Recently, there’s been a lot of chatter around the Schwab U.S. Dividend Equity ETF (NYSEARCA:SCHD), and whether the fund is still an attractive way to allocate capital in today’s market.

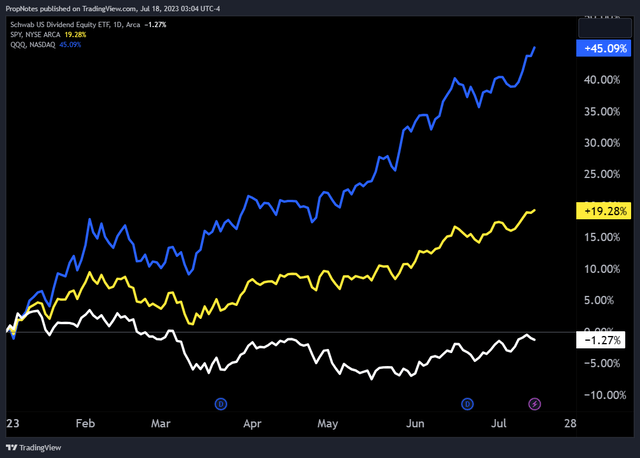

The fund has significantly underperformed the indices this year, as a result of the AI driven big tech rally, something that has chafed current investors:

(Blue = Nasdaq 100) (Yellow = S&P 500) (White = SCHD) (TradingView)

As a result, today, we’re going to examine the lagging fund and its future prospects to see whether or not it’s still worth your hard-earned cash. We’ll also take a look at another fund that may be a better option for those that are focused on investing in high-quality companies.

Is SCHD Still Investable?

Before we tackle that question, it’s important to first get an understanding of how SCHD allocates capital, and why its strategy has underperformed the market so spectacularly in 2023.

Here’s what the fund says about its investing strategy:

[The fund] invests in stocks of companies operating across energy, materials, industrials, consumer discretionary, consumer staples, health care, financials, information technology, communication services, utilities sectors. [The fund] invests in growth and value stocks of companies across diversified market capitalization. [The fund] invests in dividend paying stocks of companies. It seeks to track the performance of the Dow Jones U.S. Dividend 100 Index, by using full replication technique.

In short, the fund tracks the Dow Jones Dividend Index, and invests into the 100 or so companies that comprise it.

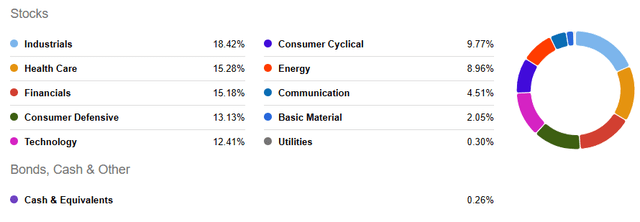

As a result, the fund has ended up with a strong weighting in Industrials (XLI), Healthcare (XLV), and Financials (XLF):

Seeking Alpha

This makes sense, as these industries, broadly, are home to businesses that are more mature and have the ability to more readily return capital to shareholders in the form of dividends.

This stands in comparison to sectors like Technology (XLK), where upstart companies are in no position to pay dividends, and more established companies still have to invest significant amounts internally to maintain their competitive advantages.

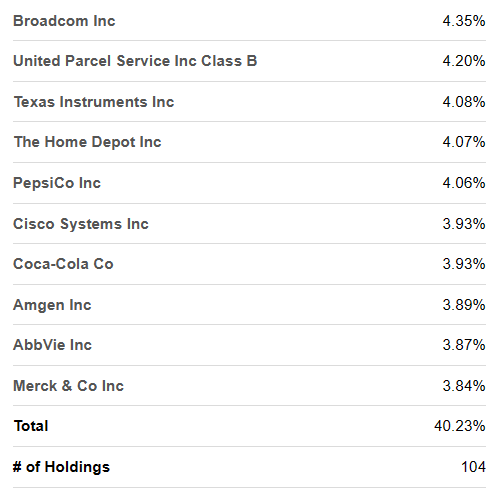

In fact, only 2 out of the fund’s top 10 holdings – Broadcom (AVGO) & Texas Instruments (TXN) – are in the Technology sector:

Seeking Alpha

This underexposure to technology is the primary reason for the fund’s underperformance over the last 6 – 9 months.

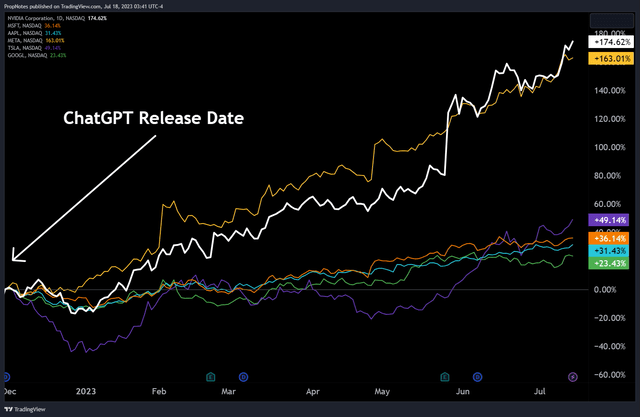

Since ChatGPT’s release, a few major AI beneficiary stocks have been on fire:

TradingView

For example, seven stocks alone (AAPL, NVDA, GOOG, MSFT, TSLA, META, AMZN) account for 90% of the S&P 500’s overall performance in 2023.

Thus, any fund without exposure to this massive speculative growth driver has, of course, underperformed. This is what has happened to SCHD.

However, does that mean that SCHD is a bad place to invest going forward?

We don’t think so.

As we discussed in recent articles on Nvidia and Apple, we think the rally in these seven stocks is getting a bit long in the tooth:

However, as [Nvidia] shares continue to climb to dizzying heights, we’re beginning to get concerned about the valuation, especially against the broader macroeconomic backdrop.

Apple remains a highly profitable company, but the stock is currently overpriced and set to drop due to market saturation for its products and an extremely overbought technical condition.

At the same time, we’re bearish on the market overall:

Considering that things are mostly still getting worse from a rate of change perspective (including the U.S. PMI diving to ~46!), we’re not ready to buy…

Combined with a pricey overall valuation environment, and the risk seems firmly to the downside at this point. We think that trimming positions here and waiting for a clearer macro-outlook is the best course of action.

Given that expensive, cyclical stocks are the most susceptible to underperformance in a downturn, we think it’s likely that capital will begin rotating back to the sectors that SCHD holds large positions in.

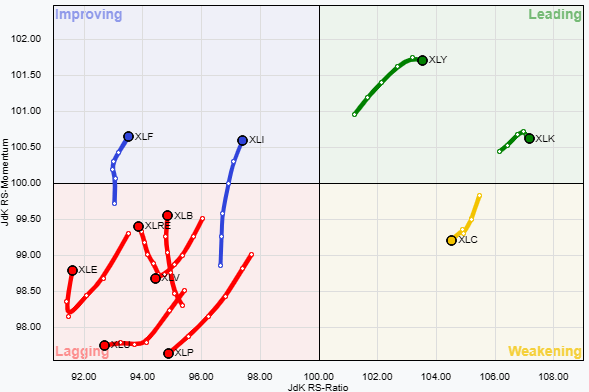

In fact, it appears that it’s already happening:

StockCharts

Financials and Industrials are firmly in the “improving” quadrant of the RRG graph above, which suggests that a bid is building in two of SCHD’s top three allocated sectors.

Healthcare remains in the “lagging” camp, but the other side of the market, Technology is finally showing signs of weakness and Communications has firmly earned a “weakening” rating.

Taken together, and we think that SCHD could outperform the market in the medium term due to these macro market dynamics.

However, just because SCHD may be well positioned for outperformance through the rest of 2023 doesn’t mean that it’s the best place to allocate capital.

Enter: MOAT

If you’re invested in SCHD because it’s a great way to gain exposure to mature, high-quality businesses, then it might be worth considering the VanEck Morningstar Wide Moat ETF (BATS:MOAT) as an alternative.

First off, we’ll state the obvious. If you’re invested in SCHD for the income, then MOAT probably isn’t worth a look. SCHD’s yield is more than 3.5%, while MOAT’s stands at a measly 1%.

However, given that a 3.5% yield right now remains rather uncompetitive, we think there may be a significant chunk of investors that could benefit from considering something else.

Here’s the basics about MOAT.

First, the fund’s objectives differ slightly from SCHD:

The fund invests in public equity markets of the United States. It invests in stocks of companies operating across diversified sectors. The fund invests in growth and value stocks of companies across diversified market capitalization. The fund seeks to track the performance of the Morningstar Wide Moat Focus Index, by using full replication technique.

In short, while SCHD looks to invest in mature dividend paying stocks, MOAT looks to invest in high-quality businesses that have “wide moat” status.

The difference is actually more subtle than it seems.

Sure; mature, dividend paying companies remain profitable. We know this is the case, because they continually pay these profits out to shareholders in the form of dividends. If they don’t, they get kicked out of the index, and out of SCHD’s holdings.

However, MOAT’s approach of seeking out companies that have a qualitative advantage first is, in our opinion, a better way of selecting equities.

Instead of selecting companies that produce profits (but may be past their prime), MOAT’s first objective is to invest in companies that have a proven, durable competitive advantage. This leads to a longer lifespan for potential alpha generation.

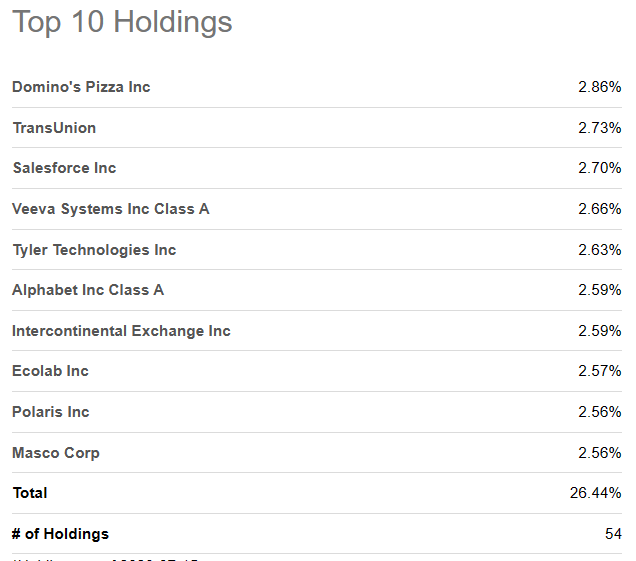

Here’s a breakdown of the fund’s top holdings:

Seeking Alpha

VanEck, the fund issuer, outsources this competitive advantage analysis to Morningstar, but we’re happy with the results overall. Let’s take a look at a couple of MOAT’s top holdings to see this dynamic in action.

Top Holdings

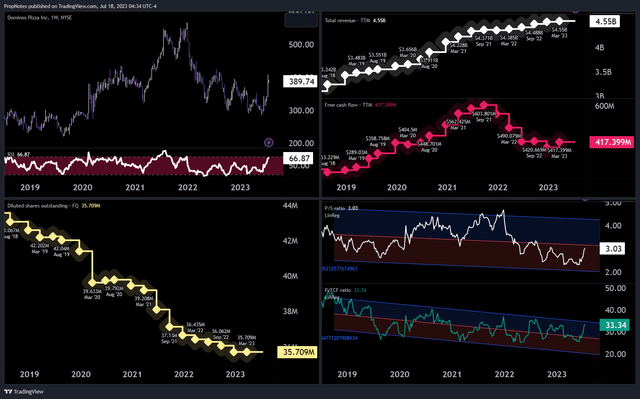

First up, we have Domino’s Pizza (DPZ).

Domino’s Pizza has a durable business advantage due to its strong brand recognition and customer loyalty built over several decades.

They have established a widespread delivery network and efficient operations, allowing them to consistently provide convenient and timely service to their customers.

Additionally, Domino’s has also invested heavily in technology, including online ordering and tracking systems, which enhances the customer experience and sets them apart from competitors. Competitors in individual markets are still often mom-and-pop operations that lack these advantages.

As a result, the company has been able to churn out revenue growth, along with stable free cash flow:

TradingView

It’s used this cash flow to return capital to shareholders and buy back stock.

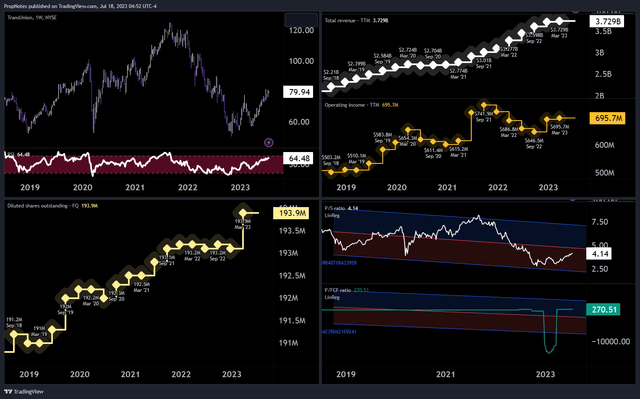

Another top holding is TransUnion (TRU).

TransUnion has a wide moat due to its position as one of the leading global credit reporting agencies.

It possesses an extensive database of consumer credit information, which is difficult for new entrants to replicate. Additionally, TransUnion benefits from strong relationships with financial institutions and other data providers, creating barriers to entry for potential competitors.

These high-moat advantages allow the company to offer a wide variety of value-add services to other businesses, like fraud detection, customer acquisition/marketing, and tenant screening, which has translated into solid revenue growth and operating income over the years:

TradingView

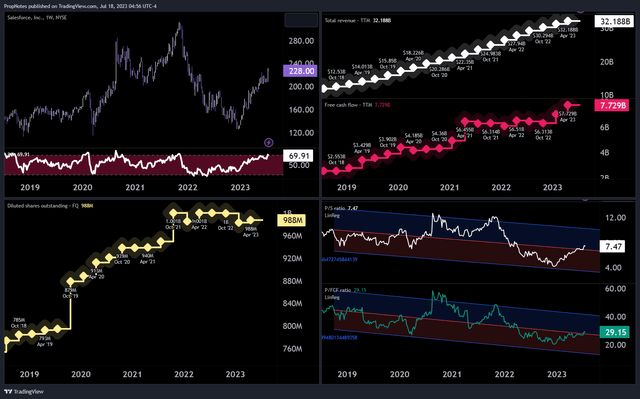

The third largest holding is Salesforce (CRM).

Salesforce has a durable business advantage due to its dominant position in the customer relationship management software market.

The company has built a strong brand and established long-term relationships with a vast customer base, creating high switching costs for clients.

Solidifying their position, Salesforce’s main product also boasts an extensive ecosystem of third-party applications and integrations enhances its value proposition and makes it difficult for competitors to replicate. On top of all of that, the company continues to spend billions on R&D.

These advantages have compounded over time, allowing the company to grow revenue and free cash flow like clockwork:

TradingView

While the company has diluted its shareholders over the last 5 years to some degree, the company remains attractively valued at under 30x FCF.

We could go down the line with each of the ETF’s holdings, but suffice it to say that they all maintain a similar level of durable advantage in their respective industries.

We’re happy with MOAT’s stock selections, and expect that the fund’s rebalancing strategy, which focuses on moat status and valuation, will keep it optimally positioned well into the future.

Historical Performance

All of this is good in theory, but how has the fund actually performed? Do the philosophical underpinnings of MOAT’s strategy work when the rubber meets the road?

We’re happy to report that the answer is a resounding yes.

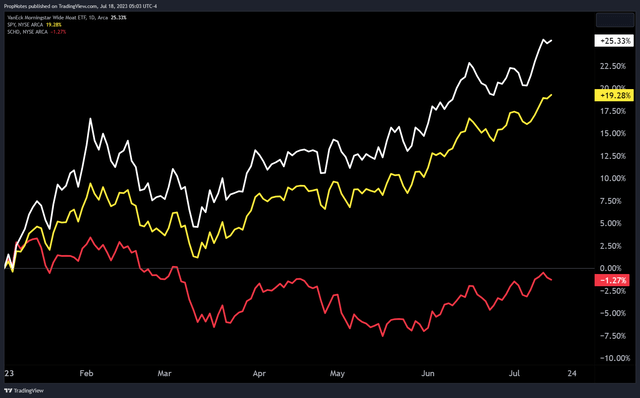

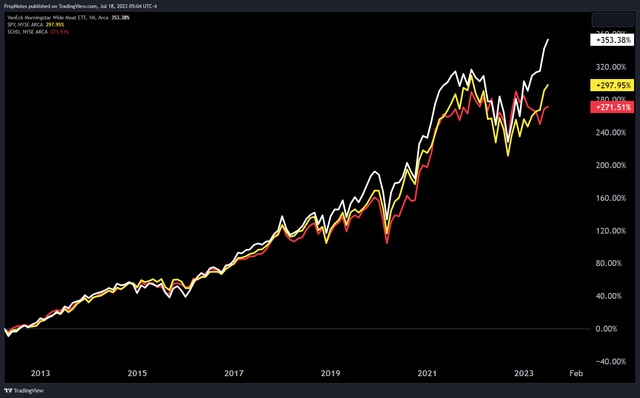

Here’s how MOAT has performed in 2023:

TradingView

Note that MOAT (in white) has outperformed both SPY (in yellow) and SCHD (in red).

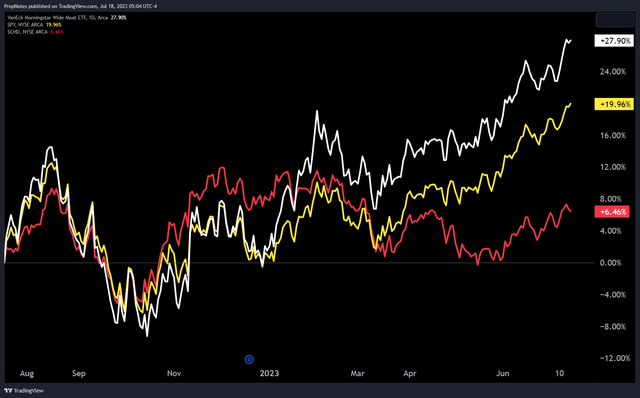

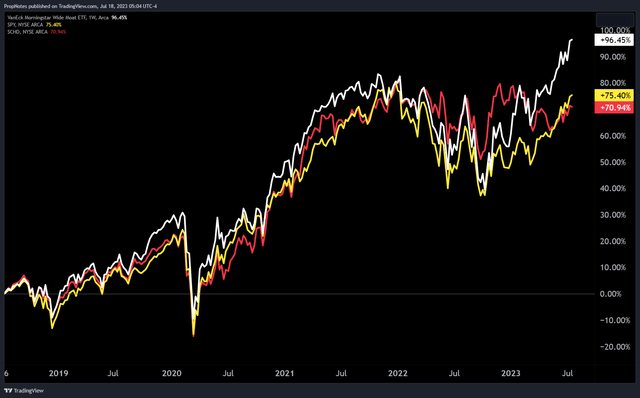

The key here is in the long term performance, though.

Over the last 1, 5, and 11 year (since inception) periods, the fund has outperformed both SPY and SCHD by a meaningful amount:

1 Year (TradingView) 5 Years (TradingView) Since Inception (TradingView)

What you’re witnessing here is alpha generation, plain and simple. Some have remarked that the fund is more volatile than SCHD due to its partial allocation to ‘growth’ as a factor, which is true. However, it’s clear from historical performance that this has been to the fund’s long-term benefit.

Summary

Like we mentioned earlier, MOAT won’t be for everyone. If you’re an income investor, then MOAT’s 1% yield is uncompetitive with SCHD’s 3.5%. However, if you’re invested in SCHD in an attempt to gain exposure to high quality, blue chip, mature holdings, then MOAT may be a more attractive option.

It boasts a better long term track record of alpha generation and total returns, and a stronger stock picking strategy that focuses on the leading cause of outperformance, as opposed to a lagging metric like dividends.

Do you think there’s an even better option for quality investors than MOAT? Let us know in the comments. Cheers!

Read the full article here