Following its IPO in June, CAVA Group’s (NYSE:CAVA) share prices have soared almost 90% above the initial offering price of $22, and I believe there’s still room for further growth. CAVA demonstrates robust unit economics alongside its rapid expansion. The company’s framework and operational expertise underpin confident expansion into new and existing markets.

CAVA is primed to benefit from shifting consumer trends favoring health, wellness, and ethnic diversity and an increased focus on quality and convenience. CAVA’s well-crafted operating platform and broad consumer appeal position it to progress from its 263 locations into a national brand of high-ROI, company-operated restaurants.

Company Overview

CAVA, a fast-casual Mediterranean restaurant chain, has distinguished itself in the food industry through its “Endless Customization” strategy, offering customers an extensive selection of 38 ingredients, resulting in over 17 billion combinations. CAVA’s assembly line system enables customers to choose from various combinations, providing a balanced blend of healthful and indulgent options catering to a diverse consumer base.

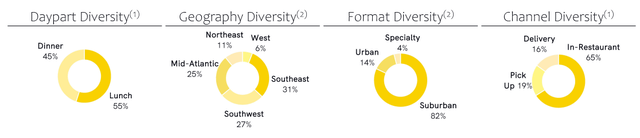

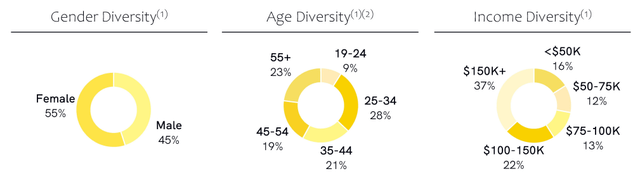

As of April 2023, CAVA’s footprint spans 263 units spread across 22 states and Washington, D.C., with the most material presence in the south and suburban locations. Notably, the brand primarily attracts higher-income customers, with about 60% of its customers from the $100k+ income bracket. Its client base is evenly distributed across genders and age groups. CAVA’s customers show no specific preference for either mealtime, with a near-equal distribution between those who order lunch (55%) and those who opt for dinner (45%).

Company Reports

Company Reports

The brand operates under a multi-channel framework, incorporating In-Restaurant Dining, Digital Pickup, Drive-Thru Pickup, Delivery, Catering, and Consumer Packaged Goods (CPG). With 35% of its 2022 sales generated from off-premise dining options (delivery and pickup), CAVA caters effectively to a multi-channel market, balancing its service between in-store and remote customer experiences.

In 2018, CAVA acquired Zoe’s Kitchen, which enabled them to quickly enter new markets and strengthen their presence in existing ones by transforming Zoe’s Kitchen outlets into CAVA restaurants. This strategic shift has propelled CAVA’s growth, heightened brand visibility, and facilitated economies of scale. From the acquisition to 2022, CAVA has successfully transitioned 125 Zoe’s Kitchen locations into CAVA-branded establishments.

CAVA brand products, such as its proprietary dips and spreads, are sold domestically in over 650 grocery stores, with about 50% of those in Whole Foods. Additionally, CAVA is exploring new strategies, such as digital and hybrid kitchen formats, to cater to evolving market demands. The company anticipates having 34 to 44 new restaurant openings in the remainder of the fiscal year 2023.

Key Performance Metrics

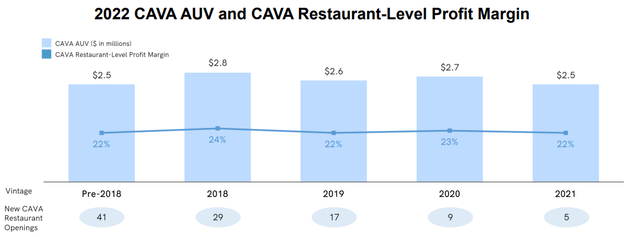

Key performance indicators such as average unit volumes (AUV) and restaurant-level profit margins signal a robust growth strategy for CAVA. The company consistently exceeds $2.0m in AUV and operates restaurants with a 22% restaurant-level profit margin.

Company Reports

CAVA’s growth strategy includes enhancing AUV and restaurant-level profit margins as brand awareness rises. Factors impacting AUV include guest traffic, menu prices, and product mix. The company uses daily sales data, regular traffic, and product mix analysis to guide pricing, food offerings, and promotions.

Digital orderings are pivotal to CAVA’s success, with about 35% of orders being digital and 80% being customized during 2022. Due to additional pricing, digital orders generate 27% higher revenue than in-restaurant orders. CAVA saw a 63% increase in users on its app. During the first half of 2022, it became the third fastest-growing quick-service restaurant app in terms of monthly active users. Additionally, CAVA has a strong loyalty program, with 3.7 million members contributing 25% of Q1 2023 sales and growing 56% year over year.

Risks

Investing in CAVA Group also comes with certain risks. The company’s growth strategy heavily relies on enhancing its current ~35% digital mix and boosting the drive-thru pickup format. If these channels fail to perform as expected, the company’s AUV)and margin goals may be jeopardized, potentially impacting stock performance.

The pricing of CAVA’s offerings, which currently command a 15-20%+ premium over similar offerings from competitors like Chipotle, maybe a concern as the company transitions from a multi-regional to a national brand. As CAVA’s customer base normalizes to include mid-higher income brackets over time, the higher pricing could limit its competitiveness and impede transaction and frequency growth.

CAVA’s growth targets involve a >15% annual increase in new store openings. Following the acquisition of Zoe’s Kitchen, conversions have accelerated development, accounting for >75% of openings from 2019 through Q1 2023. As CAVA completes these conversions in 2H23, maintaining this pace of development will be crucial to reaching its target of 1,000 units by 2032. Any decline in new unit volumes or negative shifts in comps could obscure future development visibility, leading to stock underperformance, given that the company’s valuation largely hinges on delivering promised growth.

Final Thoughts

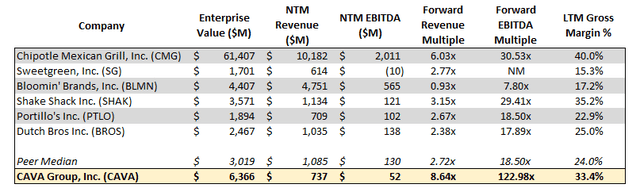

CAVA currently trades at 8.64x Forward Revenue and 122.98x Forward EBITDA multiples, which is expensive compared to its peer median of 2.72x and 18.50x forward revenue and EBITDA, respectively. And when compared to a peer with a track record of success, like Chipotle (CMG), which trades at 6.03x Forward Revenue and 30.53x Forward EBITDA, CAVA’s multiples appear even more elevated. This suggests that the market is pricing considerably higher growth expectations for CAVA.

Capital IQ

Despite the comparatively higher valuation metrics, CAVA’s unique position as a rapidly expanding, high-growth player in the fast-casual dining segment provides a promising investment case. The company’s innovative business model, focusing on digital growth, unique ‘endless customization’ food offerings, and expanding market presence, indicates a solid foundation for future growth.

Investors with higher risk tolerance and a long-term view could see an opportunity in CAVA’s ambitious growth strategy and strong operational metrics. The market’s current valuation suggests that it acknowledges and is willing to pay for CAVA’s potential to scale into a national brand and create a new market segment in the fast-casual dining sector. Therefore, despite a seemingly rich valuation today, CAVA presents an optimistic investment case for forward-looking investors banking on the company’s growth narrative and the evolution of consumer dining trends.

Read the full article here