DLH Holdings (NASDAQ:DLHC) is a company that specializes in digital health and national security solutions. The company’s customers mostly consist of the federal health services market. The company also bought out a cyber security company called GRSi, that should bring the company’s revenues and earnings to a new level. With the sizable acquisition in the company’s recent history, I believe the stock is an interesting prospect. Although the company is levered, at $10.30 per share I believe the stock is undervalued, which is why I have a buy-rating for the stock.

DLH’s capabilities are explained on the company’s website:

DLH’s Offering (DLH)

Acquisition

In Q1/FY23 DLH bought GRSi, an information technology company that develops could-based cyber security solutions mostly to government agencies such as the National Institute of Health, the U.S. Navy and Marine Corps. GRSi was bought with $185 million of which cash was the overwhelming majority. The deal was financed with a term loan of $190 million and a credit facility of $70 million, being the reason behind DLH’s currently highly leveraged balance sheet.

Grove Resource should have an EBITDA of around $18.5 million, as CEO Zach Parker mentioned the pro-forma purchase multiple to have been around 10x. The company should generate revenues of around $140 million in FY23 according to CFO Kathryn Johnbull.

I believe the acquisition is a good opportunity for the company’s investors. GRSi’s acquisition had a modest price of a 10 EV/EBITDA, an amount that is further lowered to 8.7 due to tax benefits related to the purchase. DLH’s earnings should continue to grow for the time being as GRSi is integrated into the company.

Financials

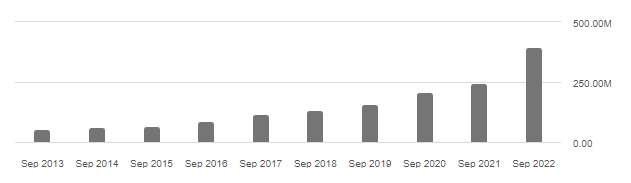

DLH’s revenues have grown very well historically, as the company’s historical compounded annual growth rate has been near 25% for the past nine years:

DLH’s Revenue (Seeking Alpha)

Last year’s revenue was greatly boosted by a FEMA task order in Alaska, where DLH got a large one-time deal related to Covid-19, and revenues have sharply declined from the previous years as the deal isn’t ongoing anymore. This seems to investors as stopped growth, but I believe the underlying business is still growing quite well. For example, in Q2 of FY23 revenues were $99.4 million compared to last year’s $68.9 million, if the Alaskan task order is subtracted from FY22’s revenues. The company’s pro forma revenue for FY23 should be around $420 million, as told in the company’s shareholder call for the acquisition. As this revenue is fully realized in FY24, the company should grow a good amount in the year.

DLH has scaled its margins throughout the years, with the company’s current trailing operating margin being at 7.1%. I believe the margin could be further leveraged as the company continues to grow and realizes some synergies between the old company and their newest acquisition.

DLH’s balance sheet is very leveraged, as the company holds $196 million of debt with almost no cash. This was caused by the recent acquisition. The company’s plan is to pay back debts as they generate cash flow from operations. This should start deleveraging the company slowly. I don’t think the company should run into liquidity problems, as the company has a credit facility of $70 million and should quite constantly generate free cash flow.

Valuation

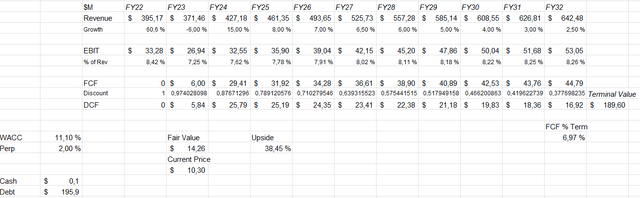

DLH trades at a trailing EV/EBIT ratio of around 16.6, which seems like quite a fair ratio for a company with some growth. I believe the current valuation to be on the low side, as demonstrated by a discounted cash flow model:

DCF Model of DLH (Author’s Calculation)

The DCF model shows an estimated fair value of $14.26, a 38% upside from the stock’s current price. For FY23 and FY24 I’m quite nearly mimicking the company’s analysts’ expectations for revenues and EBIT – in the rest of FY23 the company grows rapidly because of the acquisition, after rough comparison numbers in H1. Some of GRSi’s revenue is only realised in FY24, which is why the company should still grow revenues quite rapidly in the year. After that, I believe the company should continue to grow modestly and fade slowly into a nominal growth rate of 2%.

I believe that DLH’s margins should scale a bit as the company grows, as I’ve mentioned before. This is represented in the model as margins grow with about a percentage point from FY23’s 7.25% to FY32’s 8.26%. The company should have quite minimal capital expenditure needs going forward, as told in the acquisition’s special investor call by Johnbull:

“As always, we anticipate strong cash flow generation going forward with minimal CapEx requirements and significant potential for top line growth going forward through expansion of current contracts, growth in current markets as well as cross-selling into each other’s respective markets.”

DLH has been generating a very strong free cash flow amount priorly too, as the company’s CapEx needs have been very low for a long time, being well below a million dollars on most years. This is why I believe the company should probably convert more than its accounting net income into free cash flows.

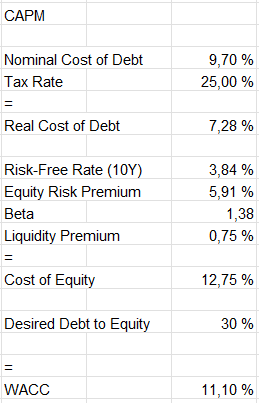

The DCF model used a weighted average cost of capital of 11.1%, that is crafted with a capital asset pricing model:

CAPM of DLH (Author’s Calculation)

In their latest quarter DLH had $4.77 of interest costs. As the company has $196 million in debt, this corresponds to an annual interest rate of around 9.7% – a very high rate. The company has a really high current debt-to-equity ratio, and I believe it should eventually come down to around 30%, as DLH does like to use debt to finance its operations.

I use the United States’ 10-year bond yield, that is currently at 3.84%, as the risk-free rate on the cost of equity side. The equity risk premium of 5.91% is taken from Professor Aswath Damodaran’s latest estimate for USA. The company’s beta is 1.38 according to Yahoo Finance. Finally, a liquidity premium of 0.75% is in my opinion fair as the company is quite illiquid on the stock market.

These expectations put the cost of equity at 12.75%, and the WACC at 11.1% for the company, used in the DCF model.

Risks

As DLH serves public clients, they are quite concentrated in revenues – if a competitor undercuts DLH’s offering in price, the company’s revenues could be at risk. I do believe that DLH’s offering is competitive enough to overcome such challenges. Also, often public service providers are quite sticky.

Another risk is the company’s large debt balance, which has been mentioned before. If the company lost a large federal client, its cash flows could be negative for a period of time, creating a risk that the company isn’t able to pay back its debt. Of the company’s almost $200 million in outstanding debt, around $33 million is in short-term debts and need to be paid within a year’s period. This shouldn’t be too big of a risk as the company still has unused credit facility.

Closing Remarks

I believe DLH is a noteworthy investment opportunity at the current price – although it is very leveraged, the newly formed company should generate a good amount of free cash flows to equity holders. If the company manages to dig itself out of the expensive debt in a reasonable time, the company seems to me to be cheap. This is why I have a buy-rating for the stock at current levels.

Read the full article here