SoFi Technologies (NASDAQ:SOFI) has been a battleground stock throughout the investment community. On May 15th, Wedbush downgraded SOFI when shares were trading at roughly $4.77, citing the fair value accounting model and reducing its price target from $5 to $2.50. The downgrade didn’t age well as Andrew Jeffrey from Truist Financial Corporation (TFC) and Mizuho’s Dan Dolev made CNBC appearances discussing their bull cases for SOFI. Anthony Noto (SOFI CEO) delivered a 34-minute fireside chat at the JPMorgan (JPM) Technology, Media, and Communications Conference that was a changing point for many and has made several appearances on CNBC discussing how SOFI will become a top-10 financial institution. Since the selloff after Q1 2023 earnings, shares of SOFI have rallied over 100%, and there is a lot to be excited about going forward. I can’t time the markets perfectly, and I have been bullish on SOFI the entire way down, and while SOFI has jumped over 100% from its lows, it’s still significantly lower than the $25 level it reached in 2021. I expect another triple beat on Monday morning and for shares of SOFI to continue higher.

Seeking Alpha

SOFI has navigated a treacherous environment and becomes stronger in the process

In business, you see what a company is made of when facing adversity. I will put the fact that I am a shareholder and bullish on SOFI to the side and be as neutral as possible. As a long-term investor, I accept the responsibility of diminishing returns when things don’t go as planned. I am not a trader, and I rarely invest for short-term opportunities. I invest in what I believe are long-term opportunities, and no matter what company it is, from Apple (AAPL) to SOFI, declines in share prices are part of investing. Unless my investment thesis has changed, I won’t exit a position, and I am likely to dollar cost average into periods of weakness. How companies respond to adversity, and unforeseen obstacles become a testament to management’s ability to handle stress, make critical decisions, and deliver solutions to problems. Nothing goes perfectly to plan in life, and the same is true in business. For me, many long-term opportunities were built upon the decisions made in periods of adversity.

By now, everyone knows the story about SOFI’s largest revenue and profit center being impacted by the student loan moratorium implemented more than 3 years ago. This was an event that was outside of SOFI’s control, and it put management in a sink-or-swim situation.

Steven Fiorillo, SOFI

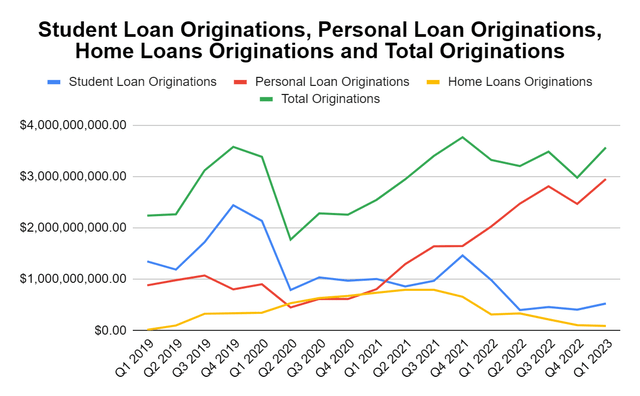

Going into the pandemic, student loan originations were SOFI’s largest component of loan originations, accounting for 68.23% of total originations in Q4 of 2019. Student Loan originations steadily grew from Q2 2019 to Q4 2019 as it surpassed $2.4 billion, then dropped off a cliff, declining -67.89% from $2.44 billion of originations in Q4 2019 to $788.69 million in Q2 2020. Student loan originations came in over $1 billion per quarter for 5 consecutive quarters from Q1 2019 – Q1 2020 and had 2 consecutive quarters of over $2 billion in originations. Since Q1 2020, over the next 12 quarters, the $1 billion level was passed only 3 times, and the lowest amount of student loan originations came in Q2 2022 with $398.72 million.

Steven Fiorillo, SOFI

From Q1 2019 – Q1 2020, the lending segment accounted for more than 96% of SOFI’s revenue per quarter, with student loan originations accounting for more than half of their total originations in each of these quarters. I want that to sink in for a moment; going into Q2 2020, lending accounted for more than 96% of SOFI’s revenue, and student loans, which accounted for more than 60% of total originations, was impacted by the moratorium, freezing payments of federal student loans.

I will speculate that some management teams wouldn’t have been able to handle the pressure and come up with solutions quickly enough to mitigate the damage. Management put SOFI in a position to significantly grow its personal loan and home loan book to offset the impacts from student loan originations operating at half mass. Both were trending upward, then the Fed started to aggressively raise interest rates which correlated to higher mortgage rates which stopped home loan originations dead in their tracks. SOFI was still able to grow its originations by growing the revenue this segment generated, consistently achieving new all-time quarterly records.

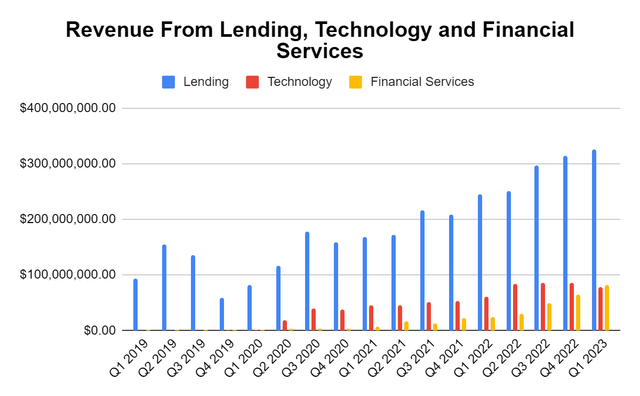

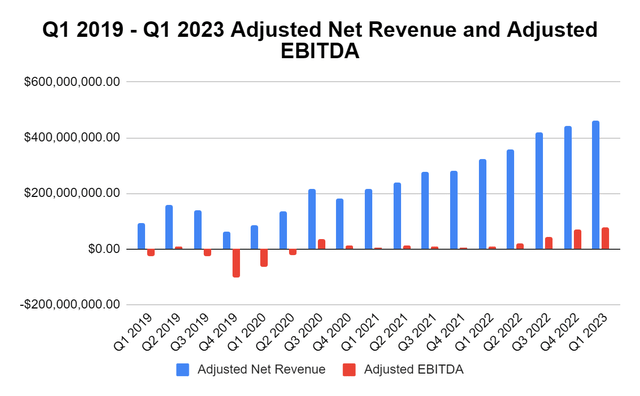

In addition to growing revenue from originations with student loan activity capped, SOFI grew its technology and financial services segments. Since Q1 of 2020, when the pandemic started, SOFI grew the combined quarterly revenue generated by technology and financial services by 4,945.64% from $3.15 million to $158.99 million in quarterly revenue. Keep in mind SOFI is a young company that just received its national banking charter in the winter of 2022. Since the pandemic started in Q1 2020, SOFI has grown its quarterly revenue by 434.26% ($374.24 million) by diversifying its business offerings and building a platform that does much more than student loans. This has led to a $141.84 million swing in Adjusted EBITDA as SOFI generated -$66.15 million in Q1 2020 compared to $75.69 million in Q1 2023.

I went into my SOFI investment knowing that it would take years for their story to unfold, and while I couldn’t have predicted the student loan moratorium being extended for more than 3-years, SOFI overcame every hurdle. Those who have been and are still bearish on SOFI are simply not paying attention to the accomplishments and aspects SOFI is getting right. Member numbers, products used, and deposits wouldn’t increase QoQ if the product suite didn’t satisfy the end-user needs. People vote with their dollars; in this case, more people use SOFI to get their money right every quarter. The end judge isn’t me or Wall Street Analysts, it’s the end users who utilize the SOFI ecosystem. The end user is speaking loud and clear. As memberships and deposits grow, there is no reason not to believe this management team won’t deliver on their goal of becoming a top-10 financial institution in the United States.

Steven Fiorillo, SOFI

Holding Loans vs Selling loans

There are several of us that follow SOFI closely and do a weekly podcast. In the recent episode, we debated holding vs. selling loans. Part of the bear case has been that SOFI is holding loans on its books because there isn’t a market to sell them. In the JPM fireside chat, Anthony Noto decimated the bear case around this idea, and I debated a SOFI bull on holding vs. selling loans.

The fact is that in Q1, SOFI reported charge-off rates of 2.97% and factored in a 4.5% loss in its marks which is below its actual tolerance level of 7-8%. When SOFI marks a loan based on held for sale on its books, they assume a loss for the loan and actualizes it over time. SOFI discussed a loss rate of 2.97% at the end of Q1 but built a 4.5% loss rate into its model to account for losses in the economy. When a loan in SOFI’s book is delinquent for 10-days they write it down by 35%, and once it hits 30-days, it gets written down by another 35%. After the first month of delinquency, the load is written down by 70%, and once 90-days is reached, SOFI writes it down by 90%, and the loan is completely written off at 120 days.

SOFI has $3 billion in equity, $5 billion in unused warehouse lines of $8 billion, and $10 billion-plus of deposits that can fund its loans. Management’s job is to create the largest amount of return on equity for its shareholders. The fact that SOFI wasn’t selling loans doesn’t mean there wasn’t a market to do so. Management made the decision to generate a 6% return by holding loans on the books rather than selling loans at a 4% return. By doing so, holding loans places SOFI’s return on equity at roughly 43% vs. the high 20% area if they sold loans. This has allowed SOFI to increase its interest income from $50 million a year ago to $200 million from lending, which will continue to grow from lending and holding loans.

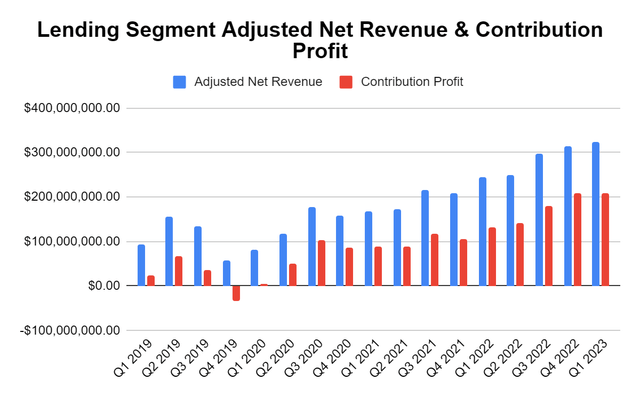

I went back to Q1 2019 and mapped out the lending segment’s adjusted net revenue and contribution profit on a quarterly basis. When I look at the overall growth, I am pleased. On a quarterly basis, SOFI has grown its adjusted net revenue in the lending segment by $231.09 million (245.85%) and its contribution profit from lending by $187.03 million (817.99%) since Q1 2019. The contribution profit margin has also increased from 24.33% to 64.57%. SOFI has a team of actuaries building their internal models, and currently, holding loans falls within their risk profile, and SOFI doesn’t need to sell loans. Management has discussed their selective loan process at length, and they see roughly 70% of applicants get declined that apply. Management has a mandate to generate value for shareholders, and if they can generate 6% from holding rather than 4% from selling, I want them to hold loans. Management has not given me a reason not to trust their judgment, and if they feel holding loans provides additional ROE, that’s what I want them to do.

Steven Fiorillo, SOFI

What I want to see from SOFI In Q2 2023 and in the future to become a top-10 financial institution

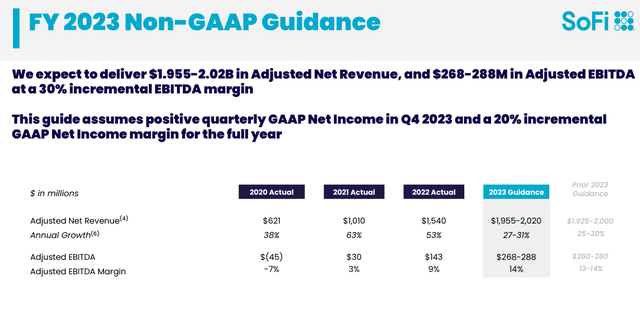

My wish list for Q2 2023 is a triple beat, Galileo Accounts to exceed 133 million, members to exceed 6.07 million, and deposit inflows to exceed $2.25 billion. On the triple beat, I want to see $485+ million in revenue, $65+ million in adjusted EBITDA, and 2023 guidance raised again. Anthony Noto has declared that SOFI will be GAAP profitable by Q4, and in Q1, they lost -$34.4 million, so I would like to see this metric improve to at least -$20 million. I have a suspicion that SOFI will deliver on everything I have outlined.

SOFI

SOFI has made tremendous progress getting to this point, but the work is not done. To become a top-10 financial institution, SOFI will need to expand its product mix further. These are some of the products and services I want to see discussed as part of their long-term plan:

- Establish a Business Segment

- Business Checking and Savings

- Business Credit Cards

- Business loans

- Overhauled Investing Platform

- New platform to compete with other brokerages

- 529 Plans

- Asset Management Arm

- Wealth Management

- Retirement Plan Sponsorship

Business Segment

SOFI already has the banking charter and is a national bank. SOFI needs to expand outside of personal banking and venture into business checking, savings, credit cards, and business lending. To compete with the large money centers, this is something that must be done. I would like to see SOFI start with small businesses, then move into medium and large-size businesses. I have talked to several business owners, and they would all be interested in utilizing SOFI as their primary bank, especially with their attractive interest rates. This will increase deposits, and SOFI will generate additional net interest income by offering business loans in addition to corporate credit cards.

Investing Platform

I want to see SOFI overhaul and expand its investing platform. To compete with Fidelity, eTrade, Ameritrade, Schwab, and other brokerages, SOFI will need to build a full product with in-depth analysis, research, analytics, and functionality. SOFI is in a position to capitalize on Liz Young being a member of the CNBC team and making many appearances on Risk Reversal Media and other outlets by making SOFI a household name in the investing space. I think SOFI should take Anthony Noto’s knowledge of Twitter and build a 2.0 platform with an interactive community with discussion groups, Q&A, and short-form media produced the way Josh Brown and Ritholtz Wealth Management have taken over YouTube. The more time people spend on the investing platform, the better.

Asset Management Arm

Once again, I want to see SOFI expand on Liz Young being on CNBC and benefit from that exposure through an asset management arm. Like JPM’s private client status, or Merrill Lynch’s investment advisory program, I would like to see SOFI become a staple in wealth management. This would lead to asset under management (AUM) fees and generate ongoing reoccurring revenue.

In addition to wealth management, I want to see SOFI become a corporate retirement plan sponsor, like Vanguard, Empower, and State Street. I get asset management fees deducted each quarter from my 401K, and it gets deducted like clockwork. Every 2 weeks, my money goes into an S&P index fund, and the institution has yet to hear from me, yet they get their fee every quarter. This would also be a benefit on the business side because companies could have all of their needs from savings, checkings, credit cards, LOCs, loans, and sponsored retirement plans in one place. There is a huge opportunity for SOFI to become a one-stop shop for business as well as personal finance.

Conclusion

I am looking forward to Monday morning because he seems very happy in Anthony Noto’s recent interviews. It’s almost as if he can’t wait to deliver earnings. Mr. Noto is one of the only CEOs that responds to members directly on Twitter and is very engaged in what the members want to see changed. Student loans are set to return, and SOFI is on track to become GAAP profitable by Q4. I think we’re going to get a modest guidance increase with a top and bottom line beat. I have no idea how the market will react, but if things are upbeat, I can see the rally continuing.

Read the full article here