Co-authored with “Hidden Opportunities”

In today’s dynamic and uncertain economic climate, it isn’t enough to only work hard to earn a paycheck. Studies show that younger generations are less likely to have loyalty to employers, with the lowest average length of time spent at a specific company. Source

Yahoo Finance

So if you are a business owner/operator, you will have a hard time keeping essential and hard-working staff.

Loyalty isn’t one-sided from the employers either. Resume Builder surveyed 1,000 employers, revealing significant workforce reduction or constrained hiring in 2023.

-

61% of the surveyed business leaders expressed the possibility of layoffs in 2023

-

57% of business leaders estimate that these layoffs will involve 30% or more of their workforce

-

70% of the surveyed companies mentioned a high likelihood of a hiring freeze in 2023

Rising rates aren’t the only excuse in the book for employers to reduce staff. During the zero-interest environment in 2014, Microsoft laid off 14% of its workforce, affecting 18,000 employees. Call it integration synergies or simplified structuring; employees are losing their jobs, potentially impacting their lives in profound ways.

Whether you are a business owner or an employee, it is critical to constantly seek reliable strategies to increase your sources of income to secure your financial future. Dividend investing is one of the most time-tested approaches to achieve this.

Calculate a desired income based on your expenses and requirements, and multiply this number by 10 and 11. This is the essence of the Income Method at “High Dividend Opportunities”. The number you get establishes a range of portfolio values that will let you live off dividends. If you seek $40,000 in passive income, a $400,000 to 440,000 portfolio can provide it by adopting the HDO Income Method.

While you think about this, we will introduce two dividend picks to brighten your passive income. Let’s quickly dive in.

Pick #1: UTF – Yield 8.2%

The infrastructure sector provides essential services that are critical to the functioning of the economy and society as a whole. The utilization of these services doesn’t change whether the economy is booming or is going through a recession. In general scenarios of weak economies, the government ramps up funding to stimulate the economy and create jobs. Moreover, the assets owned by these companies typically have long lifespans to provide services over extended periods. This makes it a sector with long-term stability, capable of delivering attractive returns to investors through economic cycles.

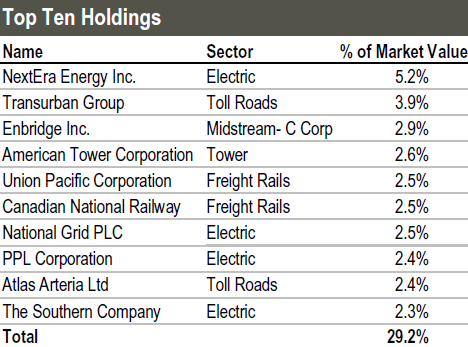

We will now look at Cohen & Steers Infrastructure Fund (UTF), a CEF that is built with 254 global infrastructure-focused companies. With 57% of its portfolio companies based in the United States, UTF is an excellent way to own assets that are being beefed up through massive government dollars.

UTF’s top portfolio companies are formidable and well-established names in the industry. Source

UTF Fact Card

As of March 2023, UTF reported a ~30% portfolio leverage with 85% fixed-rate financing. This portion is fixed at a weighted average rate of 2.1% with a 3.26-year weighted average term on financing. This positions the fund well to ride out the hawkish rate cycle and refinance at attractive rates down the road. The weighted average cost of the total leverage is 2.6%. Leverage boosts the dividend income, and UTF is actively managed to meaningfully and sustainably realize portfolio gains to issue our distributions.

The CEF pays monthly distributions of $0.1550/share, an 8.2% annualized yield. YTD 2023, UTF has paid 7 distributions to shareholders, composed of 44% Net Investment Income, 3% Capital Gains, and 53% Return of Capital.

The trillion-dollar infrastructure law will strengthen the tangible assets of American private-sector companies. These modernized and more efficient assets will power the economy for decades, and we will sit back and collect our fees through the income method with UTF in our portfolio.

Pick #2: DFP – Yield 6.9%

In the Federal Reserve’s annual stress test, all 23 of the participating U.S. banks continued to exhibit the ability to continue lending to consumers and corporations in a severe recession scenario.

Typically, these annual stress tests dictate how much capital the industry can return to shareholders via buybacks and dividends while maintaining lending. In this year’s exam, the Fed simulated a severe recession scenario with unemployment surging to 10%, a 40% decline in commercial real estate values, and a 38% drop in housing prices. Following the results of the stress tests, leading financial institutions raised their dividends to shareholders, indicating overall strength in their business and execution.

You only find out who is swimming naked when the tide goes out. – Warren Buffett

Due to broader economic uncertainty and our income objectives, we like to collect big dividends through exposure to the preferred securities of this beaten-up sector. As we have repeatedly said, this is a now-or-never opportunity for fixed-income investors. These big yields from quality preferreds trading at deep discounts have a time limit, and we are grabbing them before the sale ends.

Flaherty & Crumrine Dynamic Preferred and Income Fund (DFP) presents an attractive way to play this discount through adequate diversification and sizable quarterly distributions. DFP is diversified across 214 holdings with a 79% exposure to the preferred securities of U.S. banking and insurance companies.

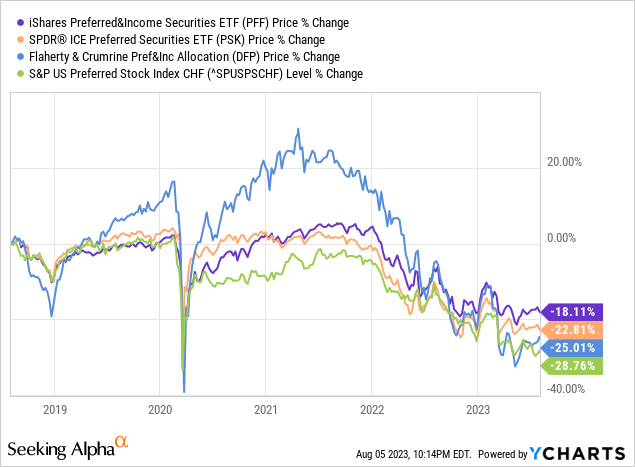

Remember, when the Fed began raising rates last year, their projections were much different than where we are today. Amidst rising rates, investors are worried that DFP has experienced a much more significant drawdown than other preferred ETFs or the benchmark S&P U.S. Preferred Index.

The above picture clearly communicates both sides of the story. Observe how rate cuts in 2019 (after years of slow quantitative tightening) and the near-zero rate climate during the pandemic years caused DFP to soar and deliver substantially better price performance than the benchmark index and ETFs.

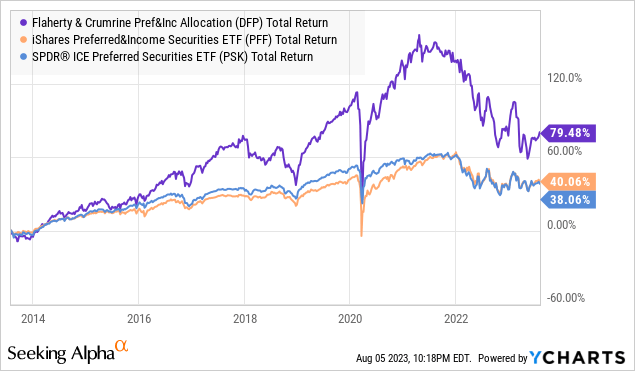

Total return includes distribution income, and this is where DFP takes the prize through significant outperformance over the long term despite recent unnerving and upsetting drawdowns. This shows that patience is an essential virtue for income investors. Not all investments shine at all times; it is healthy to have a balanced portfolio with a few constituents like DFP that potentially offer “short-term pains but long-term gains.”

Being a CEF, DFP is required to pay out a distribution equaling 90% of their taxable income and 98% of capital gains. Amidst this climate that is overall terrible for fixed-income securities, DFP can either cannibalize its portfolio by distributing more than they earn or reduce the payments to better position the fund for market recovery. As DFP chose the latter, investors are seeing short-term pain.

The Federal Reserve is close to the finish line with its monetary tightening, and several individual preferreds have already jumped from their bottom. This trend will continue, and discounts will transform into premiums. Yes, we will be back to a climate where people will pay above-par value for some yield from the same preferreds that are 40-60% discounted today. DFP trades at a mouth-watering 10% discount to par, but I want to note that this CEF has traded at healthy premiums just 18 months ago!

DFP is built with assets of higher credit quality, with 49% exposure to investment-grade preferreds. By staying invested in this asset class that sits higher up in the capital stack, you get paid to wait for better days ahead.

Conclusion

You meticulously plan for your desired retirement age, but your employer may have other plans. According to an Urban Institute study, more than 50% of American workers over age 50 either lost their jobs via layoffs or experienced involuntary buyouts or force-outs.

There is no loyalty in the workplace, either from the employees or the employer. Working towards financial independence is critical; the earlier you begin, the better your quality of life. This is important for both retirement planners and younger generations in their career’s early stages.

You may be wondering where we got the multipliers – 10 and 11 from the introduction of this article. Those represent portfolio yield levels. In our investing group, we target a +9% overall yield across our meaningfully diversified portfolio of +45 securities.

Diversification is the insurance policy on our income stream; we want our income to keep flowing no matter what economy we face. Whether companies are pursuing strategic changes, making acquisitions, or deciding to preserve their cash flows, I don’t want my quality of living affected by those closed-door decisions made by millionaire/billionaire CEOs.

By tapping into the compelling benefits of dividends, investors can navigate market volatility and experience a consistent stream of passive income that has the potential to multiply over time. We discussed two significantly discounted picks that can multiply your income and kick-start your journey toward financial independence.

Read the full article here