Introduction

Manufacturing activity is slowing down. Does it make sense, then, to be invested in companies related to this sector?

Even though the economy may be slowing down, over the long-term, the need for freight and transportation is forecasted to grow.

In this article, I want to go over the most recent earnings report of Daimler Truck (OTCPK:DTRUY), which I think is an interesting play in the truck manufacturing industry, given its recent spin-off and the need to reach best-in-class margins in a few years.

Summary of previous coverage

So far, Daimler Truck has been performing well, with increasing margins (though still at high single-digits) and record revenues. So far, it seems like the most probable candidate to reach the two current industry leaders, Volvo (OTCPK:VLVLY) and Paccar (PCAR). In fact, it must not be forgotten that Daimler Truck is the industry leader in terms of total sales, with strong brands both in North America (Freightliner, Western Star and Navistar) and Europe (DAF). I think the company is still going unnoticed by more than one North-American investor interested in the industry. While Paccar is clearly more popular, I don’t think a company whose main market is North America (38.7% of total unit sales and 43.5% of total revenues in 1H 2023) could go long unnoticed, especially given the growth prospects it has since the spin-off.

Earnings

A few days ago, Daimler Truck reported its 2Q 2023 and 1H 2023 earnings. I was expecting strong results in terms of sales and revenues. In fact, most machinery manufacturers are still producing to fulfill the huge demand surge of last year. With the supply chain much more under control, these companies are finally able to deliver unfinished vehicles, thus cashing in big margins and boosting up total sales. Let me report here a few of the 1H 2023 highlights from the most recent report

Daimler Truck 1H23 Report

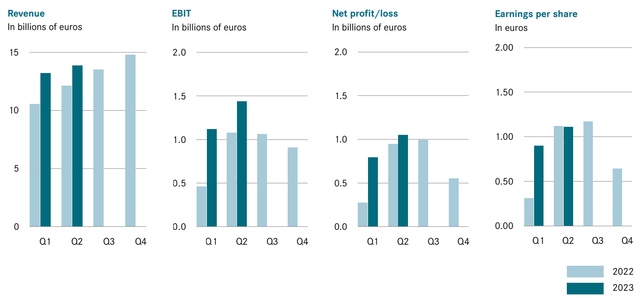

- Unit sales grew 12% to 257,060 vehicles

- Revenue grew 20% to €27 billion, showing a pricing power that outpaces the growth in unit sales

- Group-EBIT came in at €29.5 billion, a 63% increase YoY (in Q2 YoY EBIT growth was 50%)

- Return on sales is now at 9.3% for the first half, while in Q2 it reached 10%

- Return on capital employed is now at 43.3% vs. 24.7% of the prior year

- Net profit reached €1.8 billion, a 47% increase YoY

- Free cash flow of the Industrial Business was €549 million versus the prior year when it was in the negative by €683 million

- Daimler’s outlook for 2023 now sees its unit sales between 530k and 550k and a revenue between €56-58 billion. Return on sales of the Industrial Business should come in between 8.5% to 10%

Market share

As the report presentation shows, Daimler Truck still has a 40% market share in North America, being the market leader in the on-highway large/mega fleets and small fleets segments. Mercedes-Benz is now the number one brand in Europe with a 21% market share and the second brand in Brazil with a 26% market share. Asia still needs to improve, but in China the company already has a market share around 11%. Daimler Buses is back in profitable territory, though with a RoS just above 3%, and is the leader in key markets such as Europe, Brazil and Mexico (26%, 47%, 43% market share respectively).

Zero-emission trucks and buses

As we have had the chance to consider in the past, Daimler Truck is among the leaders when speaking of the electrification process. The company reported 1,793 orders Ytd vs. the 1,280 of the prior year. At the same time, unit sales are 670 Ytd (446 in 1H 2022). The company is pursuing a dual strategy with BEV and hydrogen-based vehicles. At the same time, it is investing in the development of autonomous solutions

Shareholder returns

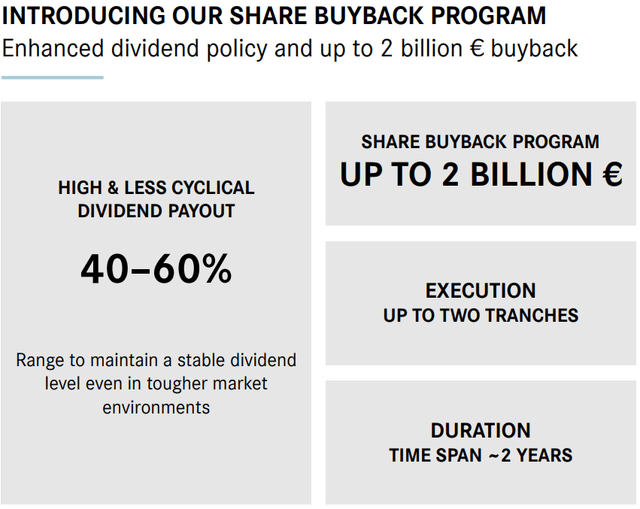

Given the favorable outlook and the improved profitability, the company introduced a dividend and a share buyback program. The company targets to pay out between 40-60% of its earnings while executing a €2 billion buyback in the next two years. This program alone is worth a little more than 7% of the current market cap.

Daimler Truck 1H23 Report Presentation

Incoming Orders

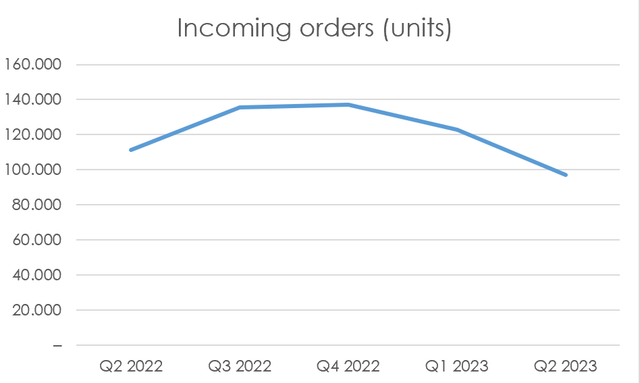

Knowing these strong results are also coming from a particular economic environment we saw in the past couple of years, it becomes even more important than usual to look at incoming orders to understand what situation the company will probably face in the next year or so.

Here we see a certain decline, with Q2 orders this year at 96,936 units vs. 111,412 in Q2 2022. This is a 13% decline in orders.

Author, with data from Daimler Truck 1H23 Report

However, if we look at the mix leading to this drop, we find important information. First of all, North America’s orders are up 7% Ytd.

In Europe, orders are declining steadily, and we are now at -20% YoY with new orders at 79,173 units versus 63,724 of Q2 2022. Trucks Asia is seeing something similar, with an order decline of 18%. Not even Daimler Buses seems to be immune from this drop, with a 32% decline in incoming orders.

Clearly, North America alone can’t offset the slow-down of other big areas. At the same time, an overall decline of incoming orders around 13% is important, but it is not even that big to put such a company in peril. In addition, strong pricing has already proven to be able to generate additional revenue at a faster pace compared to unit sales growth.

Return on sales

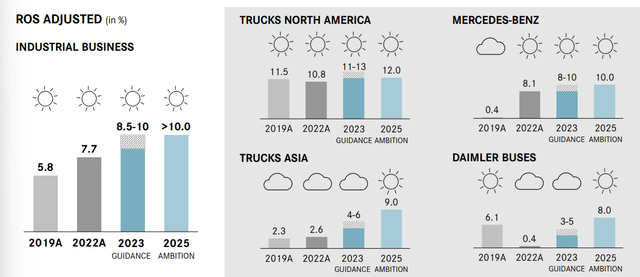

Daimler has said from its day-one as a stand-alone company that in favorable conditions it would have achieved double-digit margins. In North America, where the environment has been more favorable than elsewhere, Daimler Truck has been in that profitability range for many years.

Daimler Truck 1H23 Report Presentation

Mercedes-Benz is improving a lot, as well as Trucks Asia. Daimler Buses still needs work to be done. But this is understandable, since the pandemic gave a big hit to this segment, and it will take time to reach a full recovery. For sure, the encouraging news we are seeing from tourism and travel companies make me think demand for buses will keep on growing in the next few years.

Takeaway

Overall, the report was solid. In particular, it is quite significant the margin achieved during Q2: 10%. This means that the company is being able to increase its profitability organically, focusing on cost management and internal efficiency, rather than just boosting up sales. A decline in orders such as the one we have seen is of course a sign of a slowing economic activity, but it is also a sign of the incredible demand 2022 had. The real point to observe will be if Daimler Trucks will be able to keep up its pricing with an order decline of 10-15% or not. My take is that is probably will because of its enhanced product mix and strong brand recognition in key high-margin markets. However, even though there might be some downward pressure on the stock due to a recession, the buyback program should in part offset it. Therefore, I confirm my buy rating and my previous price target of €39 per share.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here