Co-authored with Treading Softly.

It’s amazing how a little shift in perspective can completely reorient how you look at something. Have you ever seen the famous picture where, when you first look at it, it looks like a rabbit, but when you look again it is a duck? How you look at that picture and the way you orient it completely changes your perception of what the picture looks like.

A little shift in perspective can change everything.

When it comes to the market, so many are obsessed with certain numbers or certain ways of investing that they completely miss a world of other opportunities. What amazes me is that the longer I’m an investor and the longer I’m an author, the shorter the timeframe people seem to want to hold investments. If they hold an investment for a week and it goes down in price, suddenly, it was a terrible idea. I’ve heard investors proclaim an investment “good” or “bad” based on the price action of a single day.

This is one way that we are completely different than most investors. We have a long horizon, and when we buy something, we want to hold it for at least 2 to 3 years before we even consider selling it. As such, we often find ourselves at odds with other people’s perspectives because we are willing to be in it for the long haul.

Today, I want to look at two dividends that so many people are wrong about and take a look at their earnings that were recently released.

Let’s dive in!

Pick #1: AT&T – Yield 7.7%

The first quarter of 2023 was at best a mixed quarter for AT&T Inc. (T). While it hit EPS expectations and many segments did well, free cash flow (“FCF”) at $1 billion was weak. The market panicked and started selling it off.

In Q1, Management kept annual guidance unchanged, stating:

“Free cash flow for the quarter was $1 billion. This was consistent with our expectations and accounts for several seasonal and anticipated working capital impacts. We remain confident in our full year outlook for free cash flow of $16 billion or better. This expectation is largely due to the timing of capital investments, device payments, incentive compensation, which all peaked in the first quarter.”

Then in the Q&A period, there was this exchange:

Philip Cusick

“Let’s start with free cash flow. Given the 2Q free cash flow guide down last year, what can you add to your comments already to get investors comfortable that we aren’t walking into another one of those?”

John Stankey

“Phil, thank you for the question. Overall, our — we came in exactly as we anticipated. Remember, in my commentary on at the year-end when we gave guidance, we said that Q1 was going to be the low watermark for free cash flow for several reasons. One, it’s the highest quarter of device payments.

Recall, Q4 holiday sales is the heaviest volume for devices we pay for those in Q1. You saw our capital spend is elevated relative to the annual guidance that we gave. And Q1 is the quarter we pay incentive comp. When you factor all those things in, along with our expectations that we will continue to grow EBITDA, we feel really good about delivering $16 billion or better.”

So the first thing that the earnings report needed was to show better FCF numbers. Q2 FCF didn’t disappoint and was reported at $4.2 billion. It is very typical for T’s FCF to increase as the year goes on, and guidance was reaffirmed at $16 billion.

Management expects FCF to accelerate in the second half, and we agree that is likely. Here are the factors driving this acceleration of free cash flow relative to the first-half performance.

- We expect capital investments to be about $1 billion lower in the second half of the year after peaking in the first half.

- We anticipate device payments to be about $4.5 billion lower than the first half of the year.

- The first half of the year included more than $1 billion of annual incentive compensation payments that won’t repeat in the second half.

- As I mentioned earlier, we expect full-year adjusted EBITDA growth of more than 3%.

- We expect other working capital improvements of roughly $1 billion in the second half of the year relative to the first half of the year, including higher non-cash amortization of deferred acquisition costs.

That adds up to $12.7 billion in increases not including the increase in EBITDA. This will be offset by some headwinds, for example, management also identified some $1.5 billion in lower payments (more taxes and less cash from DirecTV).

Overall, that leads us to the $11 billion or so FCF needed in the 2nd half to hit the annual target, with a chance to do even better.

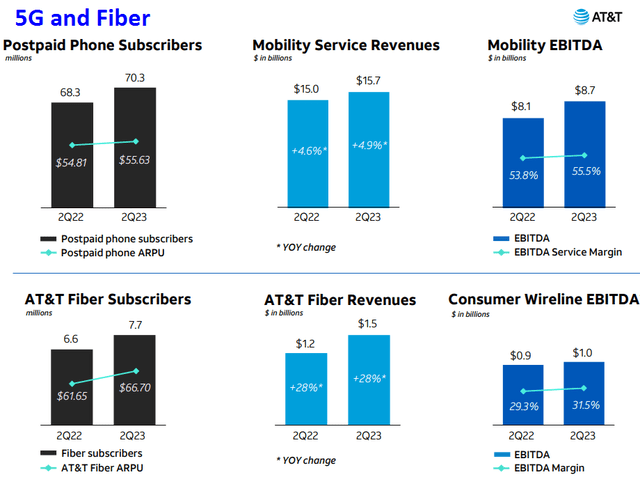

T also enjoyed year-over-year growth in both its mobility and consumer wireline segments. Source.

AT&T Q2 2023 Presentation

With a telecom like T, we are looking for an investment that is going to be slow and steady. For decades, T was recognized as a dividend-paying “cash cow” that provided a good dividend that grew slowly over many years. Its foray into empire-building, buying up Time Warner and Direct TV put stress on that model, as the businesses it bought failed to provide the consistency needed. Hence why T has spent the past several years spinning off those businesses and returning to its telecom roots, focusing on the infrastructure. A more “boring” business, but one that is a lot more consistent and can support a stable dividend. Once debt is back under control, T can go back to its dividend-raising ways.

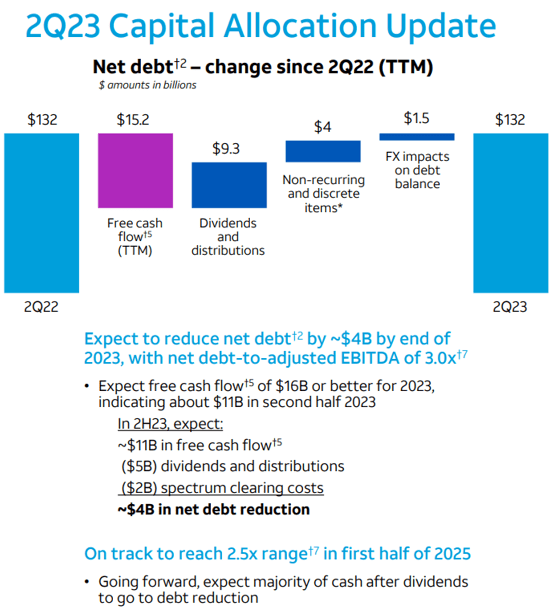

Over the past year, T’s debt has been roughly flat. T does expect that in the back half of the year, it will be able to repay approximately $4 billion, and bring debt-to-adjusted EBITDA down to 3.0x.

AT&T Q2 2023 Presentation

As expected the earnings report did not give many new details on the lead-lined cable issue. According to this article, AT&T has halted its efforts to replace such cables until it has run tests to see how much lead is actually leaking from them. As various court cases get filed and develop, one should expect some price swings as more details come to light. Management did make a statement that they were doing testing and so far the testing hadn’t revealed any lead leaks. They continue to work with the EPA to identify and resolve any issues.

This report shows significant progress toward management’s goals. Debt reduction looks good, and FCF looks like it can reach management’s $16 billion goal.

Pick #2: AM – Yield 7.5%

Some folks might say we are “obsessed” with dividends here at HDO. I agree and am somewhat confused when people say it like it is a bad thing. Yes, we are obsessed with dividends. Guilty as charged!

So it might seem a bit odd that we bought into a company immediately after the dividend was slashed. Yet that is what we did when Antero Midstream Corporation (AM) cut. The reason was that management laid out a fantastic plan that would make AM a much stronger company, allow for a much safer distribution, and will lead to growth of the distribution.

In our first article on AM, we wrote:

“In 2021, management saw an opportunity to ramp up growth for future demand for natural gas and increase cash flow. Instead of seeking bank financing or increasing share count, it decided to reduce the distribution payout.

As a result of the new investment opportunity:

- The company will be self-funded for all current and backlogged projects until the year 2025.

- It will see sustained growth during that period, without the need to increase leverage for the next 5 years.

- The forward distribution yield of 10% will be fully covered until the year 2025, and some more.

- AM will end up with excess cash generated from this new growth. It will use it to reduce leverage and re-purchase its own shares. This will eventually result in lower financing costs and higher stock prices.”

Fast forward two years later, and management is well on the path to achieving the goals it laid out. In the first half of 2023, AM saw $76 million in FCF after all cap-ex and dividends. Q2 was the fourth straight quarter of positive FCF after dividends and adjusted EBITDA was up 10% year-over-year. AM is firing on all cylinders.

Management said the first priority with FCF was to reduce leverage, and that is exactly what AM is doing. AM reduced long-term debt by $56 million in the first half, and management reiterated their expectation to reduce debt to 3.0x Adjusted EBITDA in 2024.

Once the leverage goal is achieved, we can expect AM to start returning more capital to shareholders, through a combination of distribution hikes and buybacks.

We’ve held AM for over two years, these changes didn’t occur overnight. It takes time and patience. Over the past couple of years, there were quarter-to-quarter variations. Some quarters saw negative FCF as cap-ex was higher and we saw the market sell off shares. This is what we mean by paying attention to management, and the long-term plan that is laid out. We’ve watched as AM took one step after another toward the goals that management laid out. Now, the stock is trading at the highest prices since before COVID, and AM is a vastly superior company and investment compared to what it was pre-COVID. Other MLPs like Enterprise Products Partners (EPD) have shown the path to long-term success in the sector comes from having a conservative balance sheet and self-funding all cap-ex.

It is a model that is extremely successful and leads to an MLP becoming a “blue chip” in the space. When dealing with something as volatile as commodities, the ability to fund expansion without needing to raise capital or issue debt provides a significant competitive advantage. AM created the ambitious goal to achieve a conservative balance sheet and be self-funding two years ago. It has achieved self-funding, and is now using excess capital to improve its balance sheet.

There is still some work to go, but AM is on the path to being one of the best midstream investments in the market.

Conclusion

I’ll be the first to admit that there are countless opinions on the quality of dividends from T and from AM. When seeking high-yield income from the market, there are going to be times when the companies you own are excellent, and there are going to be times when those same companies stumble and hit a foul ball. At the end of the day, I’m looking for companies that hit more single-base hits than home runs, because nobody can sustain an endless string of home runs.

When it comes to my retirement, I want it to be funded by the dividends that arrive in my portfolio from the companies that I hold. They don’t need to be world-class companies that pay a pittance of money to you as a trite “thank you” for being a shareholder, but they do need to be quality companies that have the ability to continue to grow their company and pay me excellent dividends in the meantime. That way, as any income investor would want, my retirement is completely paid for by dividends.

So thank you for paying your natural gas bill. Thank you for paying your internet or cell phone bill. Thank you so much for reading today. I look forward to seeing more income coming to my portfolio every quarter from companies like these and others that I hold. You can too.

That’s the beauty of my Income Method. That’s the beauty of income investing.

Read the full article here