Air Lease Corporation (NYSE:AL) is a name that appears on most value screens. At first glance, it appears cheap, with a market cap of $4.6 billion, a PE ratio of 10, and sporting a not insignificant 1.9% dividend. With life back to normal and air traffic back to pre-Covid highs, many investors might think of Air Lease as a safe bet. However, a closer look at the company’s financials should cause investors to rethink any decision to invest.

The stock is actually a lot more expensive than it first appears when considering the company’s total net debt position of $18.7 billion, giving Air Lease Corporation a total enterprise value of $23.3 billion. Yes, that debt is backed by hard assets (jets and planes), but it is a striking number nonetheless. $18.7 billion of net debt is especially concerning when compared to the company’s negative free cash flow.

In the past 5 years, Air Lease Corporation has managed to generate roughly $1.3 billion per year in operating cash flow, while spending an average of $3.6 billion per year on capex. The net result is free cash flow of negative $2.3 billion per year. As a result, the company is heavily reliant on external financing to stay afloat, having issued $9 billion worth of bonds in the previous 5 years.

Air Lease Corp Financials

| ($millions) | 2018 | 2019 | 2020 | 2021 | 2022 |

| Net Income | 511 | 587 | 516 | 437 | (97) |

| Operating Cash Flow | 1,250 | 1,390 | 1,090 | 1,380 | 1,380 |

| Capital Expenditure | (3,780) | (4,840) | (2,680) | (3,230) | (3,640) |

|

Free Cash Flow |

(2,530) | (3,450) | (1,590) | (1,850) | (2,260) |

| Net Debt Issuance | 2,010 | 2,000 | 2,900 | 451 | 1,590 |

Source: SEC filings

All of this debt issuance might not be a concern if the company was issuing bonds to grow and expand its reportedly profitable business, but it’s not even doing that. The company has reported net income of roughly $500 million per year consistently between 2018 and 2021 (yes, including 2020!), and in 2022 they reported a small loss of $100 million due to the write-down of assets affected by the Russia-Ukraine conflict. In 2023 the company is again set to report approximately $500 million of net income.

I always like to remind myself when researching stocks and looking at financial accounts that accountants can work the numbers and paint as pretty a picture as they like on the income statement, but the cash flow statement is always revealing. The truth at Air Lease Corporation is not great. The best investments are made in the stocks of companies that generate lots of free cash flow, and are able to pay down debts and return money to shareholders in the form of dividends and buybacks – Air Lease Corporation is not one such company.

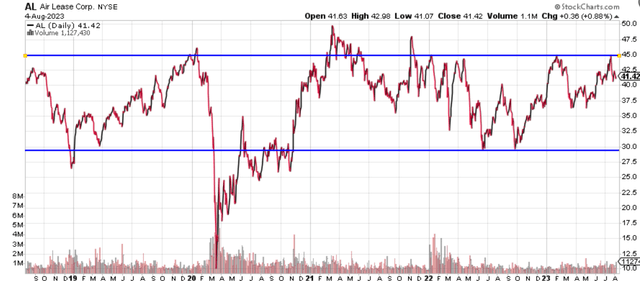

Adding to my concerns regarding Air Lease Corporation is the fact that the stock is approaching the highs of its historic trading range. As shown, the stock currently sits at a price of $41 per share, and investors have rarely bid this stock above $45 in the past 5 years.

Stockcharts.com

Investors who buy now are paying a price for the stock that leaves very little room for error and approaching a full valuation. Consider as well that the operating results are unlikely to improve in the near future as US air traffic has returned to normal and stabilized, leaving little room for growth.

For these reasons, investors should be cautious when considering an investment in Air Lease Corporation’s stock.

While the stock appears cheap at first glance, the company’s high debt burden and negative free cash flow are concerning, especially when operating results are little changed in the past 5 years. The fact that the stock is approaching its historic trading range highs suggests that there may not be much upside potential from here. Investors would be wise to wait for a more attractive entry point before considering investing in this stock.

Read the full article here