Introduction

Hims & Hers Health (NYSE:HIMS) is a digitally-native, fully-verticalized telehealth platform that provides consumers access to high-quality medical care.

The company’s mission is to help the world feel great through the power of better health, by connecting patients to a highly-qualified provider network as well as enabling access to treatments for a broad range of conditions mainly in the general wellness, sexual health, skincare, and hair care categories.

H&H just posted Q2 earnings results with a triple beat on analyst estimates. The stock responded well at first, surging 15%+ at the open.

However, the stock turned for the worse, reversing all its gains, and ended the day ~6% in the red.

Triple beat and yet it’s down 6%?

That’s unjustified.

This article discusses why HIMS stock is stupid while H&H, as a business, is far from that. In fact, it’s the complete opposite.

That said, here’s the main takeaway of this article:

While H&H continues to outperform expectations and deliver excellent financial performance, the stock is going in the other direction. This divergence between fundamentals and valuation provides a wonderful opportunity for investors to buy shares of a fast-growing, high-margin, and well-managed telehealth giant in the making.

Growth

Growth has been just phenomenal.

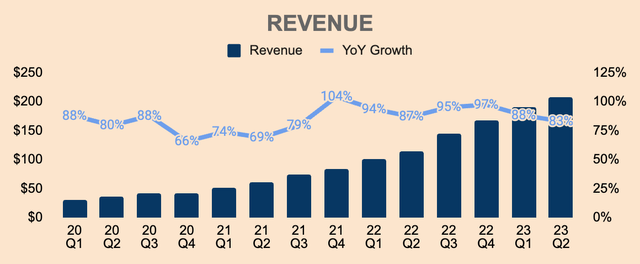

Q2 Revenue was $208M, which is up 83% YoY. This is a beat on analyst estimates by $3M.

Author’s Analysis

As you can see, time after time, quarter after quarter, Hims continues to grow at high double digits with no signs of slowing down.

However, I don’t expect the company to keep on growing at these rates indefinitely. In fact, I expect growth to slow down over the next few quarters as the company grows over a larger base.

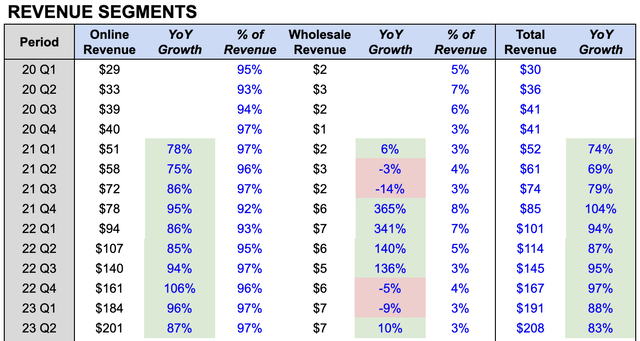

With that said, strong Revenue growth was in large part due to robust performance in Online Revenue, which increased 87% YoY to $201M, driven by the growth in Subscribers, Average Order Values (AOV), and Net Orders.

Author’s Analysis

The beauty of the H&H business model is that the company focuses on treating conditions that require medication on a recurring basis and ongoing care from healthcare providers, and that is why over 95% of Revenue comes in the form of recurring Online Revenue.

On the other hand, Wholesale Revenue remained stable with no material growth but that’s not a concern since it only makes up about 3% of Revenue as of Q2.

I wouldn’t worry too much about the fluctuation in Wholesale Revenue as this segment only makes up less than 5% of total Revenue. Besides, I’m more interested in the growth of Online Revenue as it has higher margins and stability due to the recurring nature of Revenue from subscriptions.

As mentioned earlier, Online Revenue growth was due to the increasing number of Subscribers on the platform.

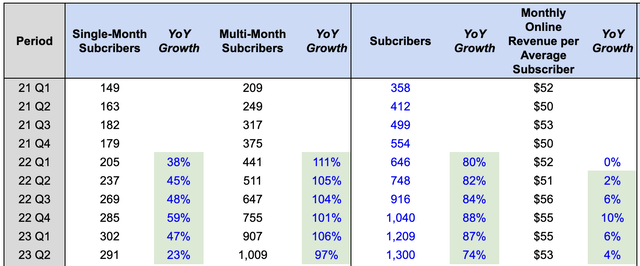

As of Q2, the number of Subscribers was 1.3 million, which is up 74% YoY.

The increase in Subscribers was primarily due to increased marketing expenses, higher traffic to its platforms, as well as higher conversion rates as a result of improved onsite and customer onboarding experience.

Online Revenue growth also benefited from higher Monthly Online Revenue per Average Subscriber, which was up 4% YoY to $53. This not only shows strong brand loyalty but also customers’ willingness to spend more on the platform.

Author’s Analysis

I also want to point out that even though Multi-Month Subscribers make up the larger proportion of the total Subscriber base, their growth is much faster than Single-Month subscribers. This is important as it means that the company is not growing because of one-time buyers, but instead, because of more serious buyers who depend on H&H products for a longer period of time.

In addition, notice that the number of Single-Month Subscribers dropped sequentially from Q1, to about 291K Subscribers. This is due to more consumers signing up for Multi-Month Subscriptions as a result of price cuts that management initiated “across longer duration and sexual health and Hims hair loss subscription plans.”

As such, Multi-Month Subscribers grew 97% YoY, to just over 1M.

The price changes also negatively impacted Online Revenue by $5M in Q2, which is why Monthly Online Revenue per Average Subscriber also dropped 4% QoQ, to $53.

The rationale behind the price cuts was that management wanted to pass on the savings it achieved from economies of scale to consumers, as well as to make longer-duration subscriptions more attractive for users.

That said, I believe this move will drive even more high-quality, loyal Subscribers to the platform.

Already, we have received several strong signals that these changes have the potential to accelerate adoption of personalized solutions, across a broader set of users on our platform. Over 35,000 existing subscribers, switched to a longer duration or personalized offering in the second quarter. We believe personalized solutions combined, with our overall strong value proposition, will enable us to retain our users for decades.

(Yemi Okupe – Hims & Hers FY2023 Q2 Earnings Call)

The shift to Multi-Month Subscriptions, in my opinion, has three major benefits for H&H:

- Higher AOVs than Single-Month Subscriptions, which are paid upfront, which H&H can use to reinvest into the business.

- Subscribers automatically stay longer on the platform, which increases their exposure to other H&H products, which increases cross-sell potential.

- Additional cost savings from product packaging and shipping as there’s a lesser need to ship out products every single month.

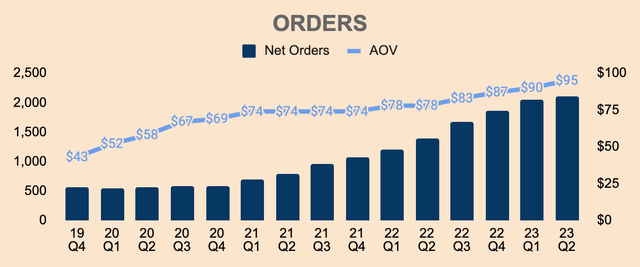

As a result of this dynamic, we can see that AOV accelerated in Q2 to $95, which is up 22% YoY, as compared to Q1’s 15% growth. The increase in AOV was driven by higher price points from higher-priced items and longer-duration Subscriptions.

Conversely, Net Orders decelerated in Q2 to 2.1M, which is up 52% YoY, versus Q1’s 70% growth.

Author’s Analysis

In short, H&H is growing at an incredible pace, growing high double-digits consistently for the past few years. This is a testament to the company’s unique value proposition as well as management’s high-level execution.

Not only is the company acquiring more Subscribers, but the company is also retaining higher-quality customers in the form of Multi-Month Subscriptions. I believe management’s change in pricing strategy and focus on longer-duration plans will pay off in the long run.

Profitability

Looking at profitability, Q2 Gross Profit was $170M, which represents a record Gross Margin of 82%.

Gross Margin has been improving over the last few quarters due to:

- lower product costs

- increased efficiency across its provider base

- the shift to longer-duration plans

- higher order fulfillment volume from Affiliated Pharmacies

- a greater share of Online Revenue relative to Wholesale Revenue

Despite the already high Gross Margins, we could expect margins to continue to improve moving forward. As it stands, H&H fulfills 70%+ of its orders through Affiliated Pharmacies. Thus, as H&H transitions to 100% in-house fulfillment, I expect incremental improvement in Gross Margins in the next few quarters.

Hims & Hers FY2023 Q2 Investor Presentation

Having said that, the high Gross Margin is a major reason why H&H has ample room to cut prices without putting unnecessary pressure on its bottom line. And despite cutting prices, Gross Margins actually improved sequentially, which displays solid efficiency gains within the business.

Given elevated Gross Margin levels, I expect H&H to cut prices across its entire product portfolio, which increases affordability, and should consequently enable H&H to gain even more market share.

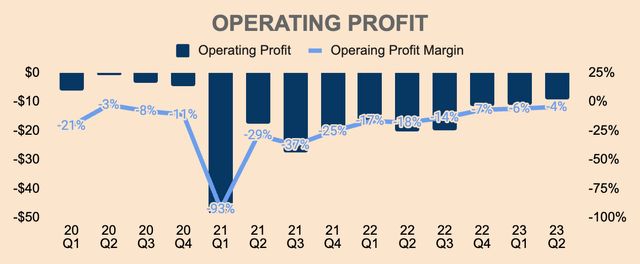

Moving on, Operating Loss for Q2 was $(9)M, which is a (4)% Operating Margin. As you can see, Operating Margin is trending in the right direction.

Author’s Analysis

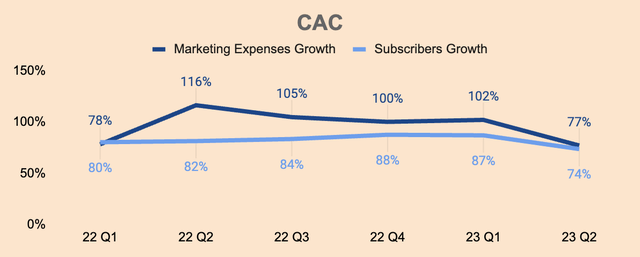

Although Operating Margins have been improving over the last few quarters, I do want to point out that Marketing Expenses increased 77% YoY, which means a great deal of growth depends on elevated marketing spend.

This reflects management’s priority to increase brand awareness and maximize new Subscriber growth. Part of the reason why management is maintaining high Marketing Expenses is due to the fact that the company has a payback period of less than a year, which enables H&H to quickly reinvest the proceeds back into the business for growth.

Nonetheless, you can see how much the company has to spend on Marketing to acquire new Subscribers. As of Q2, YoY Growth in Marketing Expenses remains higher than Subscribers Growth, which is 77% and 74%, respectively. Ideally, we want to see the opposite, as seen in Q1 last year.

Author’s Analysis

Management did mention during the earnings call that customer acquisition was slower than usual:

Marketing, as a percentage of revenue was flat quarter-over-quarter at 51%. And Marketing investments were more heavily weighted toward the back end of the quarter, as a result of the timing of new product launches, strategic pricing actions and large brand campaigns.

Customer acquisition was slower at the start of the quarter, as a result of those dynamics in a somewhat more challenging marketing environment, relative to the first quarter. We expect that investments made at the end of the second quarter, will provide meaningful customer acquisition tailwind in the third quarter.

(Yemi Okupe – Hims & Hers FY2023 Q2 Earnings Call)

As highlighted by management, we could see stronger net new Subscriber growth moving forward as Marketing investments pick up in the next few quarters – but again, it’ll be nice to see Revenue or Subscribers growing faster than Marketing Expenses.

Whatever it is, given the growth of the business as well as the market opportunity ahead, maintaining high Marketing Expenses to acquire as many customers as possible seems prudent.

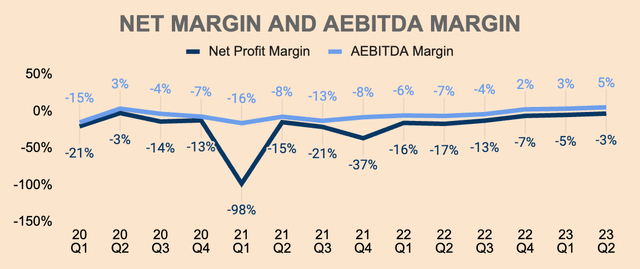

With that being said, the path to sustained profitability is well underway for H&H as the company achieves AEBITDA profitability.

In Q2, Adjusted EBITDA was $11M, which is a 5% AEBITDA Margin.

As you can see, AEBITDA margins have been improving over the last few quarters, which shows operating leverage for the company.

Net Margins should follow suit – it won’t be long before H&H achieves GAAP profitability. As of Q2, Net Loss was $(7)M, which is a (3)% Net Margin.

Author’s Analysis

That said, there are two things that I really like about H&H’s business model:

- Gross Margin of 80% is exceptionally high, indicating high earnings potential.

- Profitability metrics across the board are all improving, which shows operating leverage.

With these two elements, I believe H&H has a truly scalable business model and that should reward shareholders in the long run.

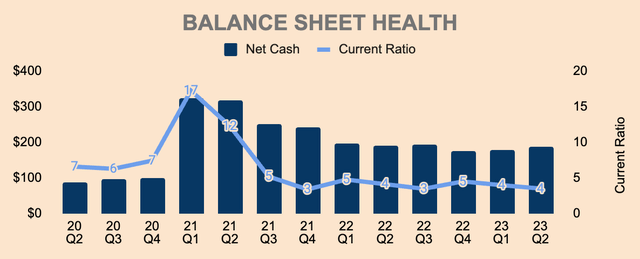

Financial Health

H&H has a strong balance sheet. The company has $193M of Cash and Short-term Investments with virtually zero debt. In addition, its Current Ratio is at 4x which is liquid and healthy.

Author’s Analysis

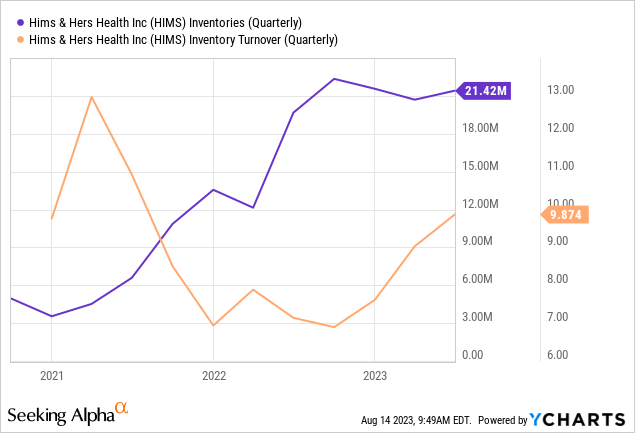

Inventory looks healthy as well with Inventory pretty much flat QoQ. As you can see, Inventory has grown over the last few years – this is expected as the company scales.

But notice that Inventory Turnover Ratio is nearly 10 and is increasing over the last few quarters. This means that the company is selling Inventory faster, which also means strong demand for H&H products.

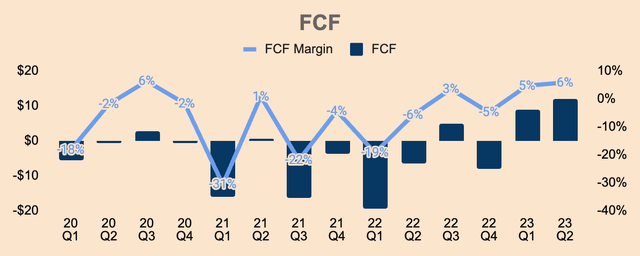

Moreover, H&H is now focusing on profitability and cash flow positivity, which is why we see a Free Cash Flow of $12m in Q2, which is a 6% FCF margin. In my opinion, I think we’ll see FCF continue to improve from here as the company achieves economies of scale and operating leverage.

Author’s Analysis

All in all, H&H has a solid balance sheet. And now that H&H is FCF positive, the company is essentially self-sufficient with no need for equity or debt raises, which eliminates the risk of major shareholder dilution.

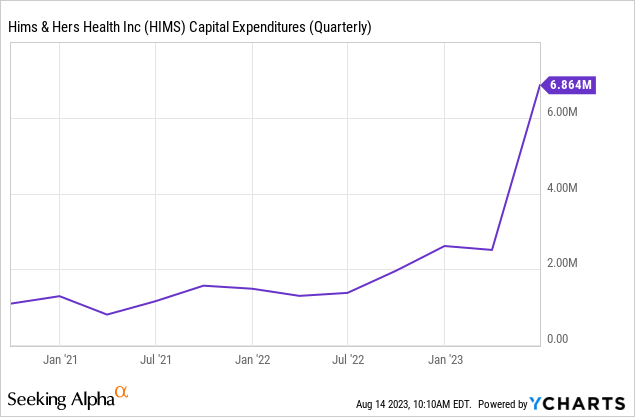

The company is also allocating capital just as it should, reinvesting all its sales and profits back into the business in order to capture the fast-growing telehealth market.

With a pristine balance sheet and an improving FCF profile, I expect Capex to pick up over the next few quarters as the company invests in additional fulfillment centers and Affiliated Pharmacies to be able to fulfill orders faster as well as gain full control of distribution and order fulfillment. In fact, it’s already happening.

Outlook

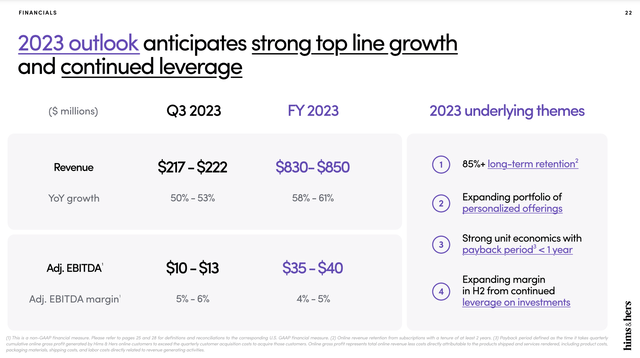

Turning to the outlook of the business, management provided the following outlook:

Hims & Hers FY2023 Q2 Investor Presentation

As you can see, Q3 Revenue is expected to be $222M at the high end, which is a 53% YoY. This is quite a deceleration from Q2’s growth of 83%. I’m guessing tough YoY comps and price cuts as the major contributors to this slowdown.

Similarly, FY2023 growth is also expected to decelerate from FY2022’s growth of 94%. That said, management expects FY2023 Revenue to be $850M at the high end, which is a 61% YoY – still impressive considering tough YoY comps.

It’s also important to note that FY2023 guidance was raised by $20M, which was previously $810M to $830M. At the same time, FY2023 guidance beat analyst estimates of $831M. This beat and raise just goes to show how strong demand and execution have been.

On the other hand, H&H also raised FY2023 AEBITDA guidance by $10M, to $40M at the high end, which is a 5% AEBITDA Margin, due to continued efficiency gains across the business.

Management also provided additional details on Revenue guidance:

No material contributions from Weight Management or Cardiovascular Health are assumed in 2023. Generally, we expect new categories to take at least 12 to 18 months from launch before they meaningfully contribute to the business.

Reflected in our guidance is an assumption that the extremely favorable marketing environment that emerged in the back half of 2022 does not repeat in the back half of 2023.

Additionally, our guidance incorporates a negative impact of between $12 million and $18 million in the second half of the year for both revenue and adjusted EBITDA, as a result of the strategic pricing changes previously discussed.

(Yemi Okupe – Hims & Hers FY2023 Q2 Earnings Call)

With that in mind, if 1) H&H’s new products perform better than expected and 2) the marketing environment turns out better than expected, H&H could once again blow past analyst estimates and internal guidance.

In other words, management is EXTREMELY conservative with their guidance – as they have always been…

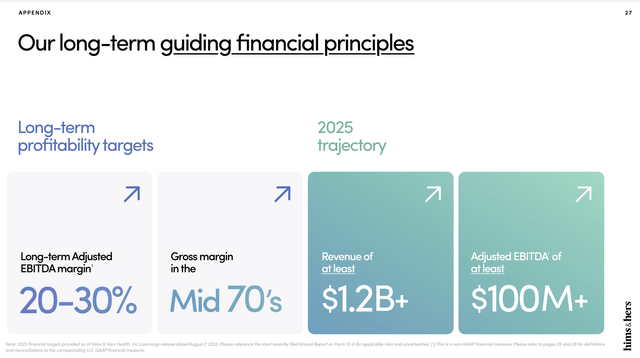

Also of important note, management maintained its long-term guiding financial principles, as shown below. Given its current growth trajectory and countless beats and raises, I’d give a high probability for H&H to achieve these long-term targets.

Hims & Hers FY2023 Q2 Investor Presentation

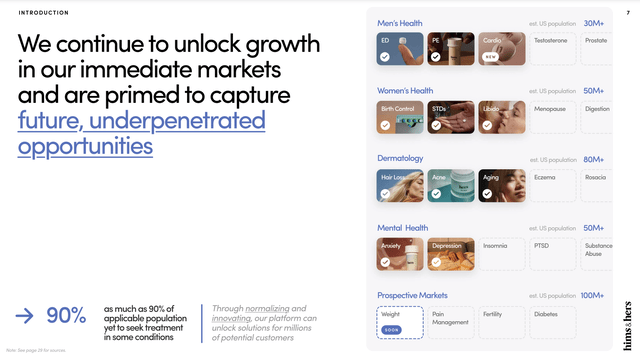

Regardless, H&H has a long growth runway ahead.

For one, as much as 90% of the population has yet to seek treatment for some conditions, which means that the healthcare market is highly underpenetrated, – I’m not surprised given how disfigured the legacy healthcare industry has been. That said, inefficiency within the healthcare system is a massive opportunity for H&H.

In addition, H&H can expand to other categories, including testosterone boosters, insomnia, weight management, and so on, and this should not only expand the company’s market opportunity but also encourage existing Subscribers to spend more on the platform, which should increase Revenue per Subscriber.

Hims & Hers FY2023 Q2 Investor Presentation

Another thing worth mentioning is that there were a few phrases that management emphasized during the earnings call:

- Personalized treatments

- Multi-category treatments

On the first point, over 35% of Online Revenue in Q2 came from personalized treatments, reflecting consumer desire for customized treatments.

On the second point, H&H is focusing on developing “single pill treatments for multi-category conditions”. This is evident from its recently launched Heart Health by Hims, which aims to address cardiovascular health and erectile dysfunction with one pill.

Combining those two points with H&H’s move to 100% in-house order fulfillment through its Affiliated Pharmacies, we have H&H’s ultimate growth story: providing high-quality, personalized, multi-category medical care at the click of a button.

Here’s a short example to help you visualize.

Perhaps you’re a first-time H&H customer looking for treatments for hair loss, erectile dysfunction, and anxiety.

Instead of having three separate pills, you can have an H&H licensed provider prescribe you a single pill that treats all three conditions, fulfilled by none other than H&H… on demand.

Although this is a long shot, it could be where H&H (and the future of healthcare) is heading. Here’s CEO Andrew Dudum to elaborate:

Our mission is to make the world feel great through the power of better health. An often underappreciated aspect of this mission is the necessity of ensuring our platform can reach as many people as possible.

The level of scale that we have combined with the efficiency of our affiliated pharmacies enables us to orient users to a model with a treatment-based construct versus a pill-based construct at exceptional value to them.

This will continue to become more meaningful, as we move further away from subscribers with one treatment to subscribers with multi-category treatment.

(Andrew Dudum – Hims & Hers FY2023 Q2 Earnings Call)

Valuation

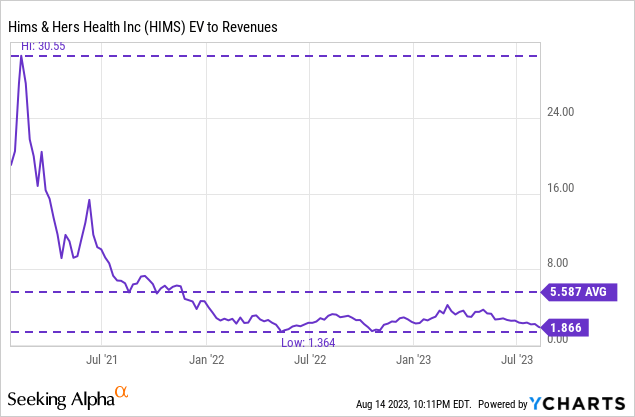

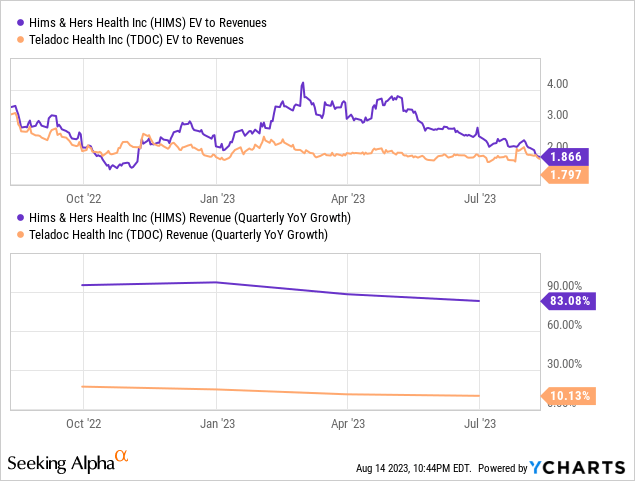

Turning to valuation, HIMS trades at an EV/Revenue multiple of just 1.9x, which is way below its peak of 30.6x and its average of 5.6x.

In essence, HIMS is trading cheaper than it was back when it went public 2.5 years ago (Q1 2021), despite

- Growing Revenue by 297%, from $52M to $208M

- Growing Subscribers by 263%, from 358K to 1.3M

- Improving Gross Margins by 500bps, from 77% to 82%

- Turning AEBITDA Profitable, from $(9)M to $11M

Two years ago, investors wanted HIMS at $20 a share.

Today, investors are dumping HIMS at $7 a share, despite being a much larger, more profitable, and fundamentally stronger company.

Sometimes the stock market just amazes me…

Here’s another.

HIMS and fellow telehealth company Teladoc (TDOC) are basically trading at the same valuation multiple even though HIMS is growing 8x faster than Teladoc.

This is rather perplexing…

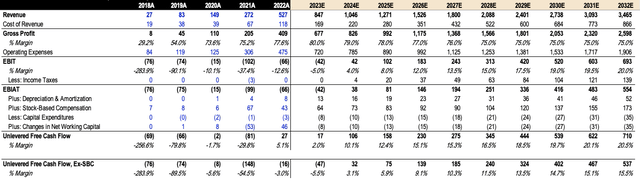

I did a DCF model on HIMS as well and here are my key assumptions:

- Revenue: For the first three years, I follow analyst estimates, and gradually dropped Revenue growth rates to just 12% by 2032 as the company grows over a larger base. By 2025, HIMS will achieve $1.27B of Revenue which is in line with management’s long-term guidance of $1.2B+.

- Gross Margin: I’m going to be pessimistic here – I’m projecting Gross Margins to decline over time from 82% today to just 75% by 2032 due to factors such as competition, product mix, and pricing. Regardless, a 75% Gross Margin is still very high and it is also still in line with the mid-70s level guided by management.

- FCF Margin: I’ll use AEBITDA as a proxy for my FCF projections. In their investor presentation, management estimated a long-term AEBITDA Margin of 20% to 30% – I’ll take the lowest end of the range just to be extra conservative.

Author’s Analysis

With these assumptions, I arrive at a Revenue of $3.5B and an FCF Margin of 20.5% by 2032, which is extremely conservative.

Author’s Analysis

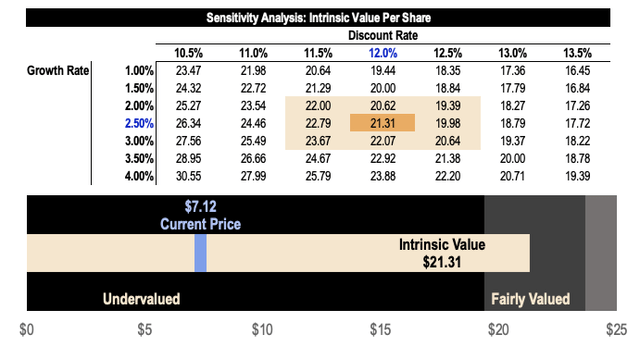

Based on a discount rate of 12% and a perpetual growth rate of just 2.5%, I get a fair value estimate of $21.31 a share for HIMS, which is much higher than the average analyst price target of $12.90.

This represents an upside potential of ~200% based on the current price of $7.12.

Author’s Analysis

Clearly, I have a strong view that HIMS stock is extremely undervalued.

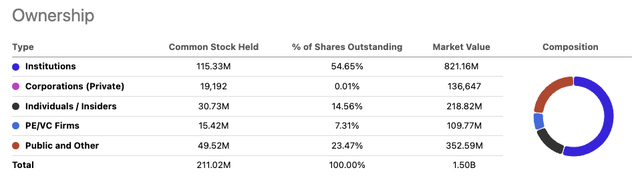

In other news, it’s great to know that insiders own 14.5% of shares outstanding with CEO Andrew Dudum owning ~9.5% of the company, so it’s a great sign that insiders have skin in the game.

Seeking Alpha

It’s also worth noting that there’s a stock option award for the CEO to maintain share prices above $10 a share.

In February 2022, the compensation committee approved a grant of a stock option award to purchase 2,085,640 shares of our Class A Common Stock to Mr. Dudum, with an exercise price of $5.01 per share that vests in four equal tranches. On each annual anniversary date after February 24, 2022, 25% of the shares subject to the option will vest and become exercisable provided that (i) Mr. Dudum is still employed on the anniversary date and (ii) the closing price of our Class A Common Stock is more than $10.00 per share in 20 of the 30 trading days prior to each anniversary date. Vesting of a performance condition can be achieved in subsequent years during the performance period if it was not previously met. If the stock price target is not achieved by February 24, 2026, then the performance option would not vest.

(Source: Hims & Hers FY2023 Proxy Statement)

In other words, it is CEO Andrew Dudum’s best interest to keep share prices above $10 a share for at least the next four years, in order for his stock options to be exercisable. That said, I think the downside is quite limited from here.

With that being said, I think there’s a divergence in fundamentals and valuation for HIMS stock – while fundamentals get better, the stock gets worse.

And instead of rallying after its Q2 triple beat, the stock sold off.

In addition, HIMS has a high short interest of nearly 14%, suggesting pessimism among market participants.

For those reasons, I declare HIMS stock stupid.

Not the business though.

And that’s where the opportunity lies for investors – buying shares of high-quality businesses when others are acting irrationally as well as when the stock is detached from its fundamentals.

Risks

Competition

In my view, competition is the biggest risk for H&H.

H&H primarily sells generic drugs with no intellectual property protection. As such, there are low barriers to entry and it’s easy for other companies such as Ro, Teladoc, and Amazon (AMZN) to launch similar products.

Recently, Amazon announced the national rollout of Amazon Clinic, the company’s very own virtual healthcare marketplace.

As it stands, Amazon has three different healthcare offerings:

- One Medical, which Amazon acquired for $3.9B in February this year. One Medical offers primary care in person or via video call.

- Amazon Pharmacy, which is the company’s online pharmacy.

- Amazon Clinic, which provides virtual care for common conditions.

As it relates to H&H, Amazon could leverage its massive scale and network, which could take market share away from H&H. In addition, Amazon can afford to sell prescriptions at lower prices, which could lead to a price war with other players including H&H.

Ro also offers very similar products and services as H&H, which could make it difficult for consumers to choose one company over the other. At the same time, it meant that H&H doesn’t really have a technological or product edge over Ro.

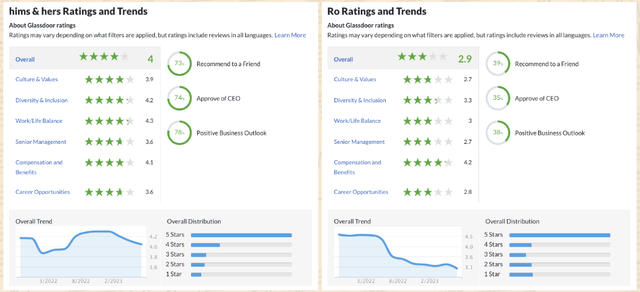

But I do want to point out that Ro seems to be dealing with a lot of challenges internally. As you can see Ro’s Glassdoor rating collapsed from 4.5 stars a few months ago to just 2.9 today.

Culture plays a huge role in the long-term success of a company, and it seems that H&H has a strong culture as seen from its high Glassdoor rating of 4.0 stars, which remained stable YoY.

That said, this could be an opportunity for H&H to grow further while Ro deals with its own company-specific issues.

Glassdoor

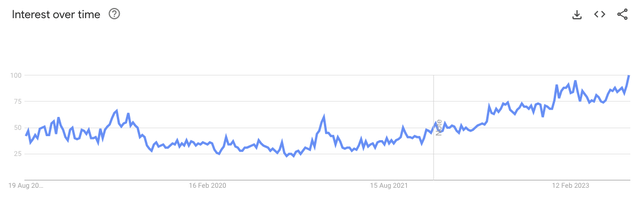

Fortunately, competition – such as Ro and Amazon – has yet to put a dent in H&H’s business. As you can see below, Google Trends show that interest in “Hims” is at an all-time high.

However, it’s still worth considering competitive risks as it could lead to issues such as slowing growth, price competition, as well as health provider supply problems.

Google Trends

Other Risks

- Tightening regulations for telehealth practices

- Lawsuits against H&H

- Unwanted side effects from H&H’s prescriptions

Thesis

H&H is one of those rare companies that is run by great management, growing rapidly in the emerging telehealth sector, and has strong competitive advantages.

I’m confident that H&H is going to be a dominant player in the healthcare space in the next decade, given its innovative telehealth platform, incredible value proposition, and excellent branding.

While the business continues to outperform expectations, the stock is getting crushed, probably due to a change in pricing strategy as well as the intensification of competition such as Amazon.

That being said, HIMS stock is incredibly cheap for a company that is growing 80%+, has a high gross margin profile of 80%+, and is about to turn profitable.

The selloff is unjustified – especially after the Q2 triple beat.

The stock is stupid, the business is not – take advantage of this irrational behavior.

Read the full article here