Investment Thesis

Matterport (NASDAQ:MTTR), the spatial data company, provides technology for creating 3D models and virtual tours of physical spaces. It offers a seductive story about bringing technology disruption to an overly physical industry that demands it.

And yet, I argue that putting aside Matterport’s alluring narrative, its outlook doesn’t inspire much hope that this business can in the near-term return to its former glory days of strong revenue growth rates.

Ultimately, I argue that Matterport is expensive for what it offers investors and is best avoided.

Rapid Recall

In my previous bearish analysis, I said:

Matterport’s share price has started to move higher in the last few weeks. This means that investors are more inclined to get involved and pay up for Matterport. However, as I analyze Matterport’s near-term prospects, I’m struggling to get behind its story and pay 6x sales for this unprofitable business.

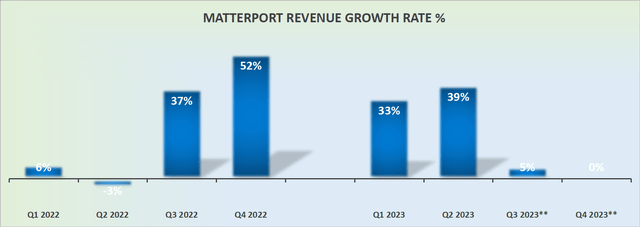

[…] it’s important to recall that Matterport acquired VHT back in Q3 2022. This led to a massive bump in revenue growth rates, starting in Q3.

However, after Q2 2023, the current quarter ending in a few days, Q3 will be lapping against that period with a significant amount of inorganic growth.

This short background illustrates what’s at play. This is a business that saw very strong growth rates in the past, but looking ahead, there’s little under its hood to reignite its revenue growth rates higher.

Outlook, Delivering Single-Digit Growth, Nothing More

MTTR revenue growth rates

In my previous analysis, I said:

Think of it as this, H1 2023 growing at 30% CAGR, and H2 2023 growing at 18% CAGR.

Consequently, however we consider Masterpoint, this is a business that’s growing around 20% CAGR and no more.

Turns out that my estimations of Matterport were woefully inaccurate and too high. The outlook for H2 2023 points to low single-digit revenue growth rates. Yes, Matterport is up against tough comparables with the prior-year period, but the message here couldn’t be clearer, Matterport is not a growth business.

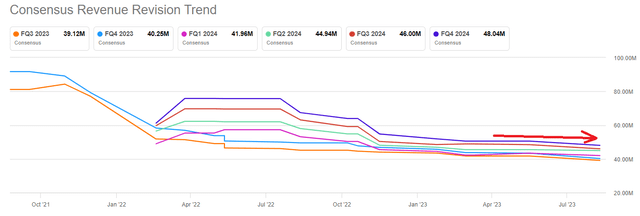

And as such, it should not be valued as a growth business. I maintain resolute in my assertion that sell-side analysts are being too flat-footed in downwards revising their revenue estimates for Matterport for 2024.

SA Premium

I now believe we can state that Matterport’s 2024 revenue growth rates are not going to come in the mid-teens CAGR.

SA Premium

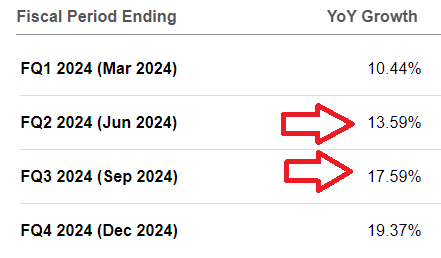

I find that I have a particular issue with analysts’ consensus revenue estimates for fiscal Q2 2024 and fiscal Q3 2024. Why?

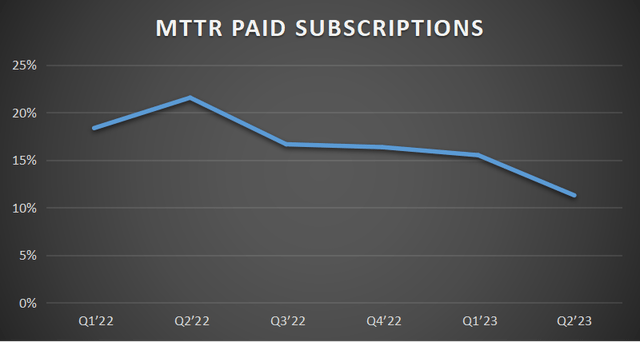

Because Matterport’s paid subscriber growth is moving in the wrong direction.

MTTR paid subscriptions

Followers of my work will know that I assert tremendous weight to customer adoption curves. In fact, I’ve regularly stated that I put more emphasis on customer adoption curves than I do on revenue growth rates. And the message in the graphic above is clear, this is not a growth company.

Why MTTR is Too Expensive?

Matterport is not a growth company. It’s a highly cyclical business that has a compelling narrative, but I believe that in the next twelve months, its fundamentals will in time catch up with its narrative. Not the other way around.

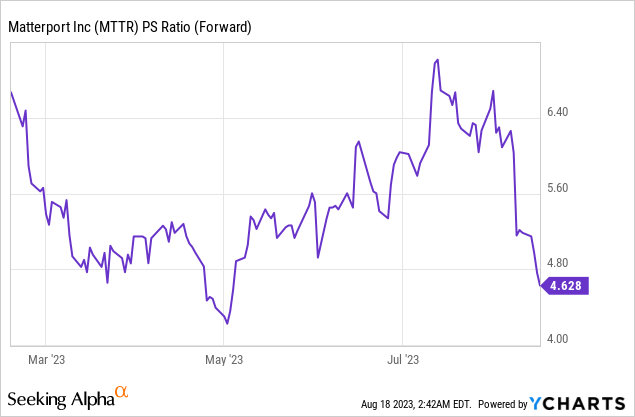

In the past 6 months, Matterport’s multiple expanded as investors sought riskier opportunities. And even though its multiple has compressed down lately, this stock is still being valued at 5x forward sales. And there’s no justification for this elevated multiple.

This is a cash flow-burning business with mid-single-digits growth rates. Stocks that trade at 5x forward sales are typically secular growth companies, with stable fundamentals, and strong and resilient growth rates. Even if they are not highly profitable, they shouldn’t be burning through cash flows every quarter. Matterport matches none of these criteria.

Are There Any Good Considerations?

Matterport’s bull thesis focuses on its debt-free balance sheet. Matterport’s cash balance stands at $440 million. This equals 60% of its market cap. Many investors may consider this to provide the business with a margin of safety.

And indeed, its balance sheet undoubtedly provides the business with ample staying power. However, I argue that is not what investors buying Matterport are thinking about, even if that is a positive consideration.

Investors are being asked to pay for a growth business and are paying a growth multiple on its stock, for what is an unprofitable business with lackluster revenue growth rates.

The Bottom Line

Looking closely at Matterport’s narrative of technological disruption in a traditionally physical industry, I find it alluring but ultimately lacking in the promise of near-term success.

Despite the initial appeal, the company’s outlook fails to instill confidence in its potential to return to the robust revenue growth rates it once enjoyed.

Viewing Matterport’s current valuation, I’m inclined to argue that its price tag outweighs the benefits for investors, making it a less favorable choice.

With the outlook indicating single-digit revenue growth rates, the narrative of Matterport as a growth business dissipates. The company’s paid subscriber decline compounds this issue, signifying a shift away from growth.

Though Matterport boasts a debt-free balance sheet, its current valuation of 5x forward sales seems unjustified for a cash-burning entity with lackluster growth. In the end, the allure of Matterport’s narrative is overshadowed by its financial realities, making it a cautionary choice for investors seeking true growth potential.

Read the full article here