The Australian mining giant BHP (NYSE:BHP) released its full-year (year ending June 30, 2023) results yesterday. Suffice it to say, they aren’t pretty. When I wrote about the company in late June, with just the slightly dated first half (H1 FY23) numbers, the revenue outlook looked challenged even as there was more hope for earnings.

Price Chart (Source: Seeking Alpha)

On balance, I believed it’s best to go with a Hold rating, and its price performance since, with an almost 8% decline, hasn’t given me any reason to think otherwise. Here I take a closer look at the latest results to assess if the future looks better for it than the recent past.

Revenue decline worsens

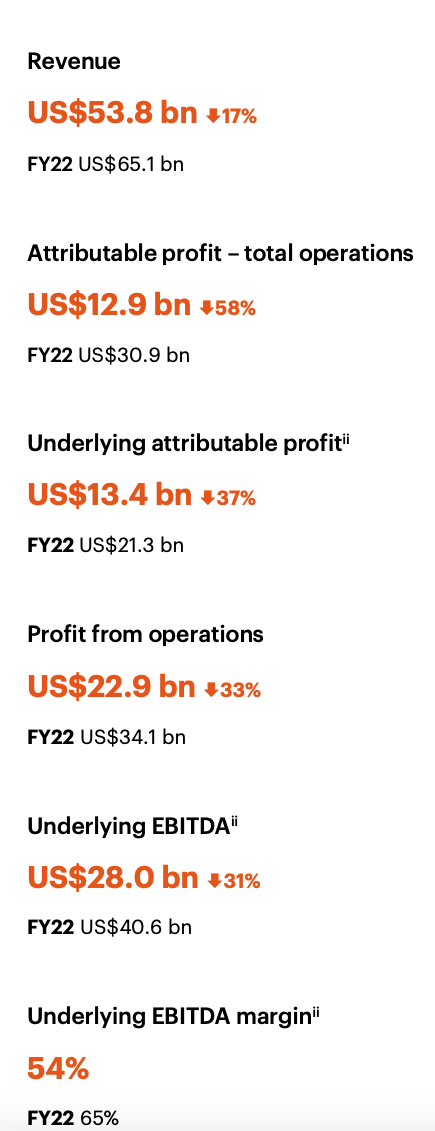

BHP’s Revenue declined by 17% in FY23, as prices of both iron and copper, its two key revenue generating commodities fell. While the realised price of iron fell by 18%, that of copper declined by 12%.

Key Financials, FY23 (Source: BHP)

There’s more to note here. One, the revenue decline for the full year is slightly higher than the 16% fall seen in H1 FY23. This is in contrast with the company’s own somewhat optimistic outlook on account of the return in China’s demand.

BHP mentions that while the recovery in China was strong in the first quarter of 2023, raising hopes of continued demand expansion, “that momentum did not carry over fully to the June quarter”, a weakness from China was to be expected, going by the recent industrial activity data.

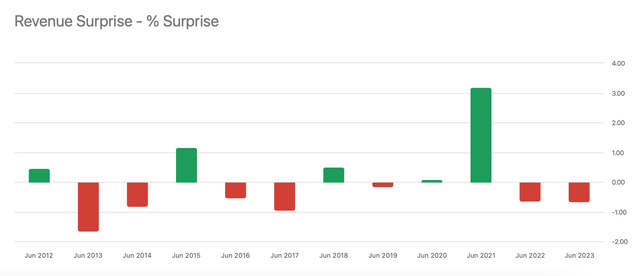

Two, the decline is actually just slightly higher than the 15.7% drop expected by analysts, resulting in a negative revenue surprise for the second consecutive year (see chart below). In other words, BHP’s revenue performance worsened not just from its own past figures, but also as compared to the outlook.

Source: Seeking Alpha

Earnings and dividends crash

The fall in profits was even worse, by 58% at the reported level for total operations. It did slightly better on the underlying attributable profit and earnings per share [EPS] front, with a 37% decline each, but even this was bigger than the 32% contraction seen in H1 FY23. However, it’s some small comfort that the actual EPS was higher than analysts’ estimates by 5.7%.

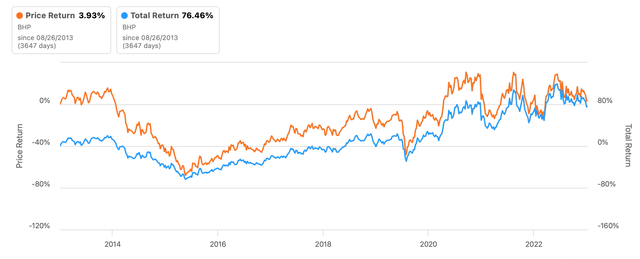

The dividends for the year commensurately fell by almost 48% year-on-year (YoY) in FY23. This is particularly disappointing since BHP is more a dividend stock than anything else. As I pointed out in my last article, over the past decade the dividends increased returns on it by 5-fold compared to just price returns. The increase is now almost 20-fold (see chart below), as price returns now look even smaller.

Returns (Source: Seeking Alpha)

Weak outlook

While BHP is positive on the long-term outlook on factors like “population growth, rising living standards, and the infrastructure required for decarbonisation”, in the short-term, less so.

Essentially, it says that the outcome for commodity prices hangs in balance with an “uncertain” outlook for the developed world on the one hand and China and India serving as “relative sources of stability for commodity demand” on the other. This suggests that revenues can go either way. Analysts, however, tilt towards the downside, with a 2.5% expected decline in revenues for FY24.

Further, the company also expects cost inflation due to the “lag effect of inflation peaks observed in FY23” and “continued labour market tightening”. In effect, this means that earnings could stay impacted. Analysts concur with expectations of a 11.6% EPS decline in FY24.

What about dividends now

This, of course, is likely to continue spilling over into dividends. BHP’s forward dividend yield is at 6.4%, compared to the 9.4% trailing twelve months [TTM] yield. Interestingly though, the forward yield actually looks better than the 5.4% levels it was at when I last checked, which wasn’t bad to start with.

This still makes BHP a good dividend stock to invest in. And going by its past history is likely to remain so. In the last 10 years, the compounded annual growth rate [CAGR] for dividends has been 10%, which is healthy in itself, but it’s an even higher 24.8% over the past five years.

The market valuations

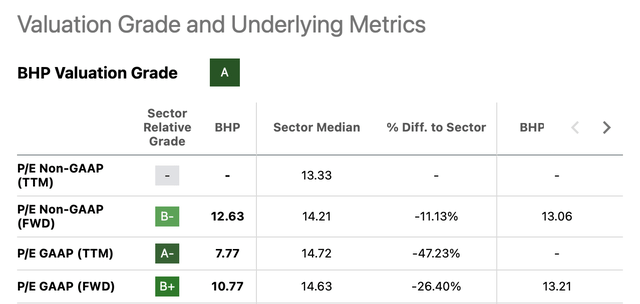

BHP’s valuations too look improved from the last time I wrote on it, with all price-to-earnings (P/E) ratios now lower than the average for the materials sectors and also its own five-year averages. The TTM GAAP P/E comes in the lowest of the lot at 7.8x, down from 8.3x in late June and significantly below the 14.7x for the sector.

But even the forward GAAP P/E has come off (see chart below) compared to the sector and its 13.6x level in June. I’m more inclined to draw an investing conclusion from the non-GAAP forward P/E, though, considering that it tends to be more predictable. While the number is also well below the sector, it’s just slightly lower than BHP’s own five-year average, indicating that the stock is still fairly valued.

Source: Seeking Alpha

What next?

BHP’s latest results are undoubtedly bad. A decline in revenues and an even bigger fall in earnings reflect the weak commodity price and macroeconomic environment. But there’s no way of saying if the situation can improve in FY24. In fact, analysts expect an ongoing softening in the company’s financials next year.

This of course has a bearing on its dividends, which is really the big reason to buy BHP in the first place. Still, the forward dividend yield isn’t bad. Added to this is the fact that the company has on average seen healthy dividend growth over the past decade. So, as the commodity cycle turns, passive income from the stock can improve in absolute terms.

BHP’s market valuations are also improved from late June when I checked last. They aren’t just competitive compared to the sector but also their own past average levels.

However, I’m not convinced right now if it’s a buy based on just the potential price returns. And the reason is China. While the company expects relative stability from the market, the incoming data shows some continued weakness. I maintain a Hold rating on it, with the exception that it’s a buy for dividend investors only.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here