I seem stuck in Safehold (NYSE:SAFE). After recent simplifications, we needed a new thesis for our members. Plan A was to develop a related article as a public one, more focused on some criticisms of our point of view.

Then Safehold announced an equity raise, so I did a short article discussing that. There was some good learning for me from interacting with readers.

I also had a chance to interact at length with a skeptic in the comment section of our investing group. That very useful conversation was mainly focused on identifying the differences in our viewpoints. It will make sense to put some related issues into an article on valuation, but that won’t fit here.

Here I fulfill my promise to address the current and near-term cashflows of Safehold and their G&A costs. So we will focus on that today.

Brief Overview of Safehold

For new readers to this topic, the only purpose of Safehold is to grow a portfolio of ground leases and to profit from doing so. Ground lease landlords own land and lease it for extremely long periods such as 99 years. At the end of the lease or in the event of default they recover the control of the land and ownership of any structures upon it.

It matters essentially to do this with quality ground leases in quality locations. The leases need to:

- Not be too large a fraction of the entire property value.

- Have small enough and steady enough rent escalators to avoid what happened to homeowners in 2007 when their ARMs reset.

- Have provisions that protect everybody involved.

- And so on.

Safehold is organized as a REIT and does deal with real estate. But, in contrast to most REITs, they do not operate any real estate. Safehold has negligible operating expenses and zero capital expenses.

In addition, they do not own revenue-generating components of real-estate, as do the net lease REITs. Significant staff in such REITs is devoted to portfolio monitoring and management. Safehold has almost none of that.

Instead, they are a RINO (Reit In Name Only). So are the billboard REITs, though for very different reasons. Safehold does need more real estate expertise than those, to put together deals involving operating real estate and to monitor the health of their tenants.

Context From My Past Analyses

My research on Safehold has always been concerned with one thing: fair value. For them fair value depends very strongly on discount rates, which correlate with interest rates.

I almost never make predictions about stock prices, though I recently opined that interest rates will come down and in response the price of SAFE will increase.

Similarly, anyone who looked at the graphics in my 2020 and 2021 articles on Safehold would have expected that the price of SAFE would drop if interest rates rose. So while Wall Street analysts may perhaps have missed the boat there, it is not accurate to state that “No one apparently bothered to check what would happen when interest rates rise.”

Those who correctly anticipated that the Fed would produce a historically large and fast increase in interest rates would have known how precipitous this price drop of SAFE would be. My question for those who seem sometimes to think they did that is: where is your yacht?

The fair value of SAFE has almost entirely to do with the value of cash flows that will span a century. But much of the clamor about them has been focused on current-year or near-term cash flows.

So let’s take a look at those cash flows today. Then people can learn or disagree, ideally there will be some good discussion, and in any event I will have a place to send future readers. Then my focus can return to what really matters here.

The Wheat and the Chaff

Unfortunately the cash flows of Safehold have been complicated, in two major ways at least.

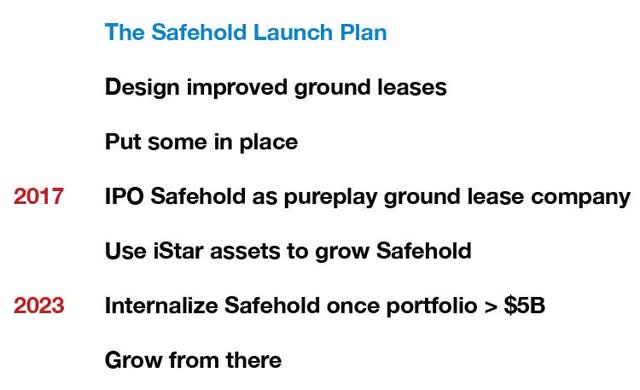

The complications reflected the plan for launching Safehold and taking it to a size that enabled internalization. Management has been very explicit about this for years. Here is my summary:

RP Drake

Safehold was externally managed until Q2 of this year and now is the external manager of Star Holdings (STHO). The job of Star Holdings is to liquidate the few remaining assets of the previous external manager, iStar.

iStar was not taking all owed management fees and was buying stock that Safehold issued. Both aspects were part of using the net value of iStar to launch Safehold.

Then the merger of iStar and Safehold this year added more complexity, costs, and some new items. Today, management fees from STHO and from other sources still add noise to the main story. But we will see that they will provide some welcome help during the early years of independence.

Second, with their very long-term, escalating cash flows (and in some cases, debt payments), there are a lot of noncash elements in the Income Statement. To make matters worse, changes in GAAP accounting over time have created added complexities.

Fortunately, the non-cash items are explicitly labeled on the Statements of Cash Flows and the merger costs are detailed in the 10-Q from Q1 2023. The non-cash portion of GAAP revenues has been running about a third and looks to me to be above 40% for 2023.

So we can throw out the chaff, though not perfectly. Here is the remaining wheat:

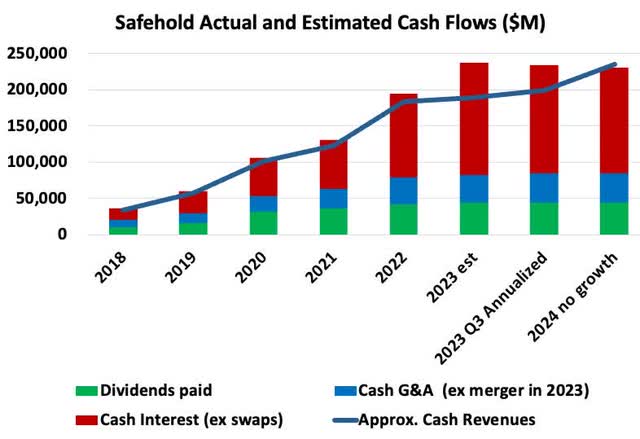

RP Drake

The solid line shows the cash revenues obtained from the GAAP revenues less the non-cash items on the Statements of Cash Flows. The red bars show the cash interest costs, similarly obtained.

The blue bars show the cash G&A costs. Going forward, this should run about $10M per quarter, increasing with inflation after some initial post-transition decreases.

The green bars show the dividends paid. These were quite close to Cash from Operations (less changes in working capital) until diverging somewhat in 2022 and a lot this year. Some years ago, the then head of Investor Relations shared their basic intent to pay out all the free cash flow as dividends.

What stands out today is that the top of the red bar for 2023 est. is above the cash revenues in my estimates. This is the impact of several factors, in my view:

- The increase in short-term interest rates during 2022

- The fact that preparations for the merger precluded doing much about it before April this year

- Debt increases to accommodate costs of the merger

Also shown is my best attempt to project Q3 costs and to annualize them, and to project 2024 assuming that the rest of the signed leases begin paying rent, but not assuming any growth. This includes anticipated revenue from management fees for STHO. We will see in future quarters how far off these estimates will have been.

Here it appears that cash earnings may not come back into balance with cash expenditures this year without a divided cut. The board could take a couple of different perspectives on this. They could, for one, decide to just eat the debt.

The amounts involved will be at most a few percent of the current floating-rate debt and less than 1% of total debt. We will see below that any deficit should rapidly go away as years pass.

Or the board could decide for cash-flow discipline and reduce or eliminate the dividend. I don’t know what will happen and I tell members of High Yield Landlord not to count in any way on the dividend. The story of value in Safehold has nothing to do with the dividend in near-term years.

I’m also not even talking about this aspect with management, having seen other managements get blindsided by their board on this issue before. There are more useful things to discuss.

Of course there are other items that appear at times and that impact quarterly cash from operations. They might provide fodder for somebody looking for a stick with which to beat up Jay Sugarman, but they don’t seem to me to have any enduring significance. In my view the items discussed above are what matters.

The G&A Costs and Their Context

The $10M per quarter of cash G&A costs supports a team who originates deals and implements ground leases. Based on what they accomplished before mid-2022, they should be able to sustain a run rate of at least $1.5B of additions to the portfolio (the maximum achieved to date by the same team was $2.2B in the TTM period through Q2 2022). We will base some modeling on $1.5B shortly.

Management has emphasized to me in conversations for several years that the point of this team and of nearly all the G&A is to grow the portfolio. Far fewer people would be needed to support public company costs and to run the portfolio, which takes a very small effort.

There is also the much-maligned stock-based compensation or SBC. Current filings are misleading for two reasons. First, the SBC is grade-vested on a 4-year schedule starting the date of the merger, so the accounting has it largest this year and falling a lot for the next three. Second, prior to the merger iStar covered the routine incentive costs but now it all falls on Safehold.

The run rate for SBC will be about $2M per quarter on average, but heavily weighted in the accounting into the first year of four. That total today is a bit more than 4% of current cash revenues. That fraction will decrease with time because the existing team can steadily bring on board new ground leases that add to revenues with no significant impact on G&A.

You can decide whether the amount of G&A upsets you. For me, there are more important things to focus on, specifically what growth it enables.

The Near Future Without Growth

The primary forward cash flows are simple after the merger, once you escape GAAP and get cash numbers. There is cash revenue, cash interest costs, and cash G&A expenses. That’s it, save for dividends.

There are still some comparatively small complications, mostly now as other kinds of revenue. This includes management fees for STHO and from the two funds Safehold manages. And there are potential future one-time events such as the property sale in 2022.

Portfolio growth has been challenged for the past year. The real estate and capital markets have been locked up. In addition, implementing the merger must have detracted from the ability to close deals. Even so, the portfolio has grown by $400M YoY at the end of Q2.

The skeptics seem to believe that Safehold will not grow their portfolio from here. One has to wonder what they think those people paid for by G&A will do. Perhaps they think that, rather than finding new leases, the management team will channel Wall Street movies and spend their time in alcohol and drug-fueled parties for the next 90 years.

Returning to reality, it might take a few quarters to get portfolio growth back up. And though it is highly unlikely, the capital and real estate markets could stay a mess for some years. So let’s see what the existing portfolio would do, without any additions.

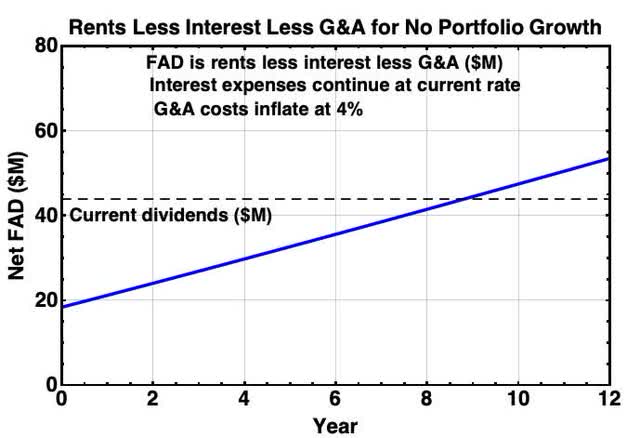

We assume that cash G&A remains as discussed above, with those costs inflating by 4% per year. There is an uncertainty regarding the future cost of the current revolver debt. Safehold at the moment has about $900M of floating-rate debt, as they did use the recent equity raise to reduce the revolver balance.

They have 5-year swaps in place under which $500M of that will cost them 3% interest (rather than the ~6% they paid in Q2). They also have $400M of Treasury hedges in place that will limit their cost on new debt to 3.47%.

In this context, it makes sense to me that near-term debt likely costs about the same as it does now. This would prove quite pessimistic if rates come back down within a year or two.

Revenues will increase somewhat, though, as current lease commitments are funded and rents escalate at 2%. Here is what I find for Funds Available for Distribution, or FAD [cash rents less cash interest expense less cash G&A] from the existing and pending portfolio:

RP Drake

Here the FAD (blue curve) does not include the revenue from management fees, notably for Star Holdings. These will close most or all of the gap vs current dividends for the next few years.

Even on this very negative scenario Safehold would stay cash-flow positive throughout the next decade. They have a real advantage from having no capex and no opex.

Thinking About Growth

It seems more sensible to me to expect that the Safehold team will proceed to grow the portfolio. That also is now a simple story. Here is the essence:

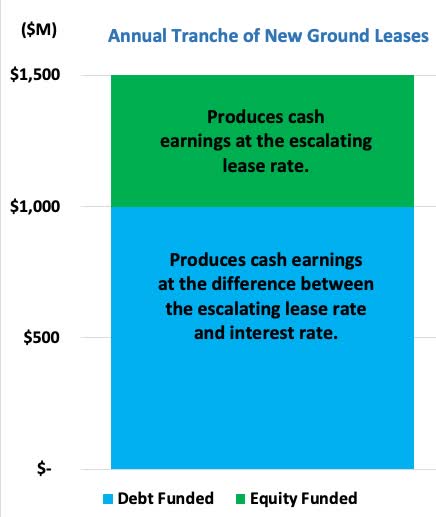

RP Drake

Safehold will invest about $500M of new equity per year to grow the portfolio and will pair this with about $1B of new debt. We will call the first set of leases equity funded and the second set debt-funded.

In presentations they have always highlighted the spread between the yield on the leases and the interest rate on the debt. But that spread is small. Comparatively speaking, it is the interest payments on the $500M of net new equity (green bar above) that provides the bulk of the net cash at first.

We don’t know where lease rates will settle, but the exact level is not the main factor determining value (more on this later). Here we will use 4%, so that the new equity generates $20M per year of new cash earnings.

More slowly the escalators on the invested capital from the debt-funded leases (blue bar above) add additional net cash earnings. Here, for simplicity, we assume that the spread is zero between initial cash lease rate and the interest rate. The exact value does not matter much anyway so long as it is small.

For 2% escalators, this generates an incremental $0.8M of net cash earnings in the second year. That increment increases with time. This gets more complicated if the interest rates are structured in time, but we won’t go there today.

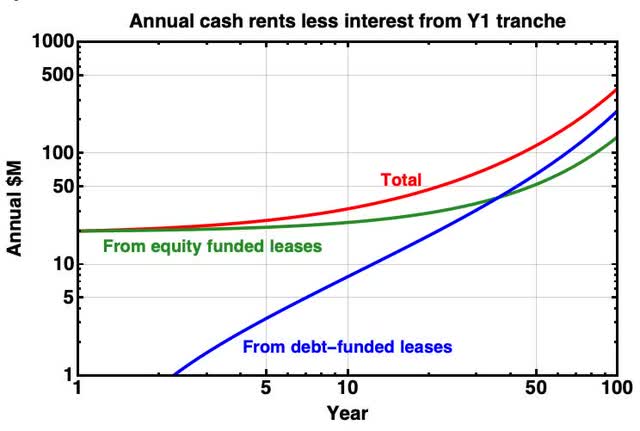

First let’s look at the consequences of the first tranche of investments at a total of $1.5B per year. Here they are on a log-log plot:

RP Drake

You can see that for about 40 years the equity-funded leases (green curve) carry the load and that the debt-funded ones (blue curve) take over after that. Debt refinancing might alter the exact trajectory of the blue curve, but across the whole century this is a small detail.

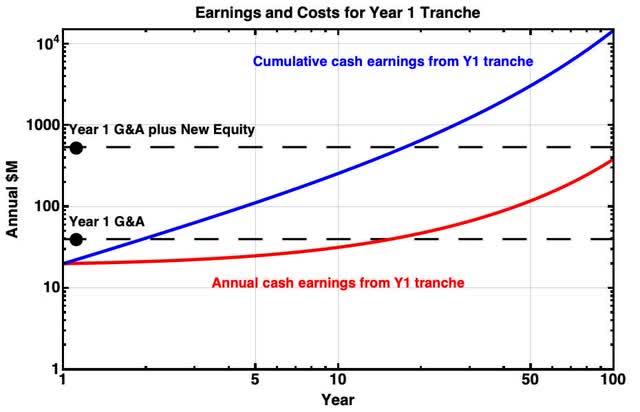

Next, for this first tranche, we compare the cumulative cash earnings with the associated equity and G&A costs.

RP Drake

The cumulative earnings (blue curve) recover all the invested new equity (and the year-1 G&A) within 20 years and then provide additional earnings for another 80 or so. In total, the cumulative cash earnings over 99 years are more than 26 times the invested new equity. This is a CAGR of 3.3% on those funds.

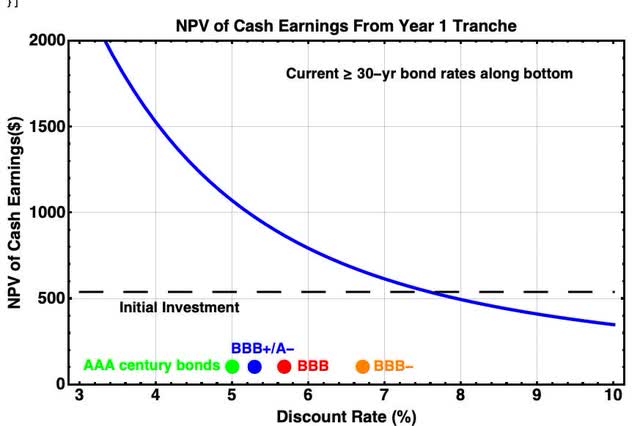

Of course one should not care about non-discounted cash flows, especially over decades. So we discount the annual cash earnings shown by the red curve and determine the NPV of the cash earnings as a function of discount rates.

RP Drake

Note the title of the chart here. The plot addresses the NPV of cash rents less interest costs from one and only one tranche of ground leases.

Those ground leases, like any leases, are assets of Safehold. We are asking what they, net of debt, are worth.

The most important factor that determines what they are worth is the discount rate used to value the cash flows. If this is equal to or smaller the median current discount rate for >30-year bonds rated BBB- or above, then this one tranche of ground leases creates value. That is true even with today’s elevated interest rates.

Safehold claims that the discount rate should be closer to that of the highest credit ratings. Green Street, myself, and some other analysts agree. The implication is that using new stock to provide equity for the tranche is accretive to overall shareholder value.

I have a lot of new things to say about the discount rate, earnings multiples, and what they mean for SAFE. But they won’t fit here. So stay tuned for a next article, which I hope will be the last one for a while on this company.

Takeaways

Safehold has transitioned to a state where its future cash flows will be much simpler than those of its past. If you want to know where things are going, think about their future as a fully internalized company.

Two reasons for the simplicity of the cash flows are that they have zero Capital Expenditures and near-zero Operating Expenses. To my mind, this is significant in the context of valuation.

If real-estate and capital markets remain difficult or interest rates increase further, then it appears to me that the dividend might not be well covered during the next few years. This is even allowing for management fees they will receive, though these ought to mostly close any gap.

But if you look ahead a few years, Safehold should be growing strongly and the dividend should be steadily increasing. Still, investing in SAFE strictly for the near-term dividend does not seem wise to me.

There are two more important points. First, the cash flows will get cleaner and the earnings will rise from here, likely rapidly. Second, the value of the Safehold cash flows is very much not in current-year numbers or even current-decade numbers.

SAFE is and always will be a NAV play where most of the value comes from distant decades. This is very much a story like that for very long-term bonds.

They are locking in cash flows that will last a century. No other REIT is anywhere close to that.

One needs to think clearly about what that means. Stay tuned.

Read the full article here