For anyone who has been following Cleveland-Cliffs (NYSE:CLF) over the years, the recent bid for United States Steel Corporation (X) is hardly a surprising move.

The much-needed consolidation within the industry has been going for quite some time and Cliffs’ CEO – Lourenco Goncalves is not deviating from his aggressive M&A approach. He is certainly not the type of CEO who will be swayed by quarterly developments and temporary macroeconomic headwinds in his ambition to create a national champion in steel production at a time when geopolitical imbalances are reaching unsustainable levels.

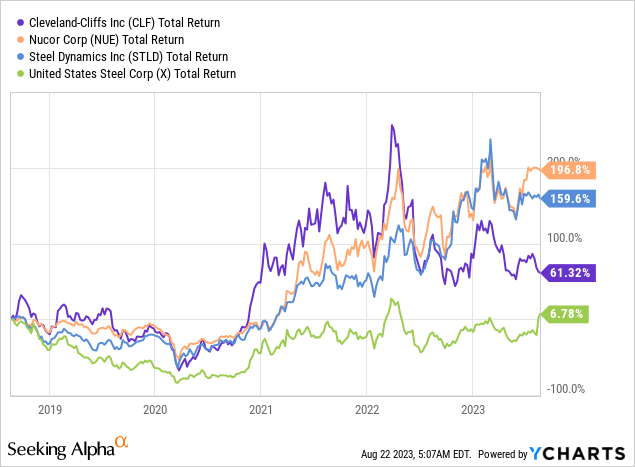

As he is setting even more ambitious goals, however, discontent among shareholders is growing as CLF continues to underperform two of its major peers – Nucor (NUE) and Steel Dynamics (STLD).

It also appears that the deal for United States Steel would not be a smooth sailing as more bidders emerge and the saga around United Steelworkers develops.

Seeking Alpha Seeking Alpha

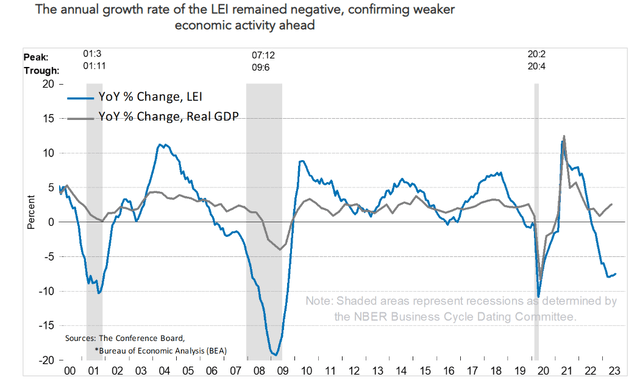

Last but not least, CLF exposure to the highly cyclical automotive industry could also make the matters worse for shareholders as The Conference Board Leading Economic Index® (LEI) signals an upcoming recession.

conference-board.org

All that highlights the importance of remaining critical and staying away from emotional biases when evaluating Cliffs’ current strategy and the latest move to acquire U.S. Steel.

Consolidation At Any Cost

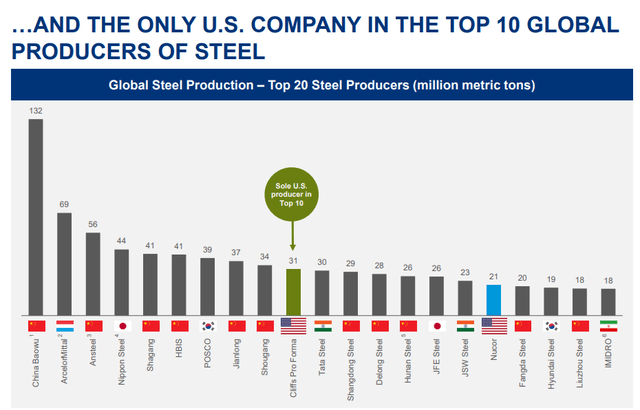

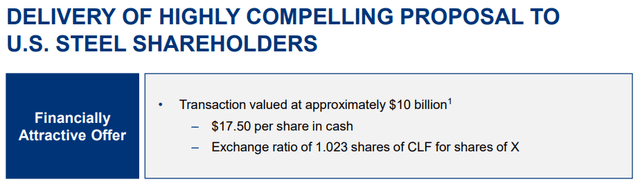

The prospect of owning one of the largest steel companies in the world is enticing and, to a certain extent, creates a halo effect that the deal for United States Steel would create additional shareholder value for CLF no matter what.

Cleveland-Cliffs Investor Presentation

It is hard to argue against the synergy benefits from combining two large entitles in a highly commoditized sector and Cliffs’ recent history of delivering on such cost synergies solidifies the case for pursuing such a large deal this time around.

Cleveland-Cliffs Investor Presentation

But all that is hardly a reason to give your unconditional support for the latest acquisition target.

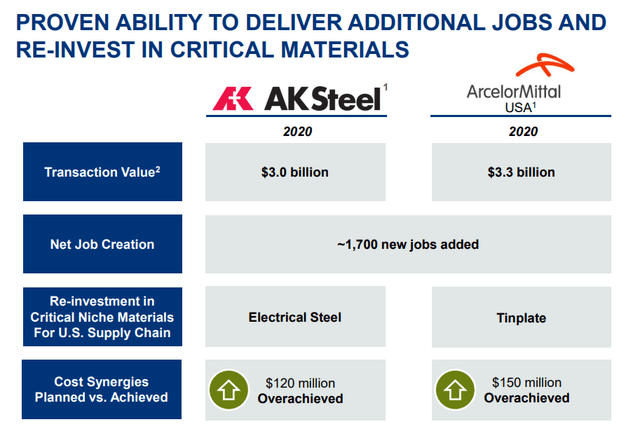

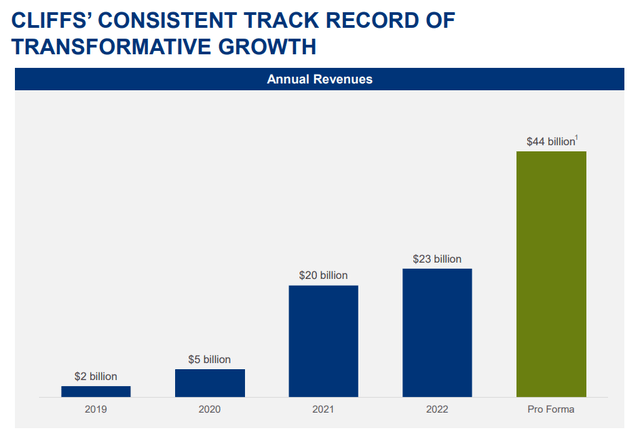

As a starting point, the deal for U.S. steel is nearly 3 times larger than those for AK Steel and ArcelorMittal U.S. operations.

Cleveland-Cliffs Investor Presentation

Even more importantly, however, a large proportion of the deal will be financed by issuing stock. At first, nothing unusual when considering how Cliffs paid for AK Steel a few years ago.

Jones Day website

The problem, however, is that Cliffs’ shareholders will be heavily diluted this time around since CLF stock price is now trading at considerably lower multiples.

This makes the deal far riskier for CLF shareholders and significantly increases the probability of Cliffs overpaying for its peer.

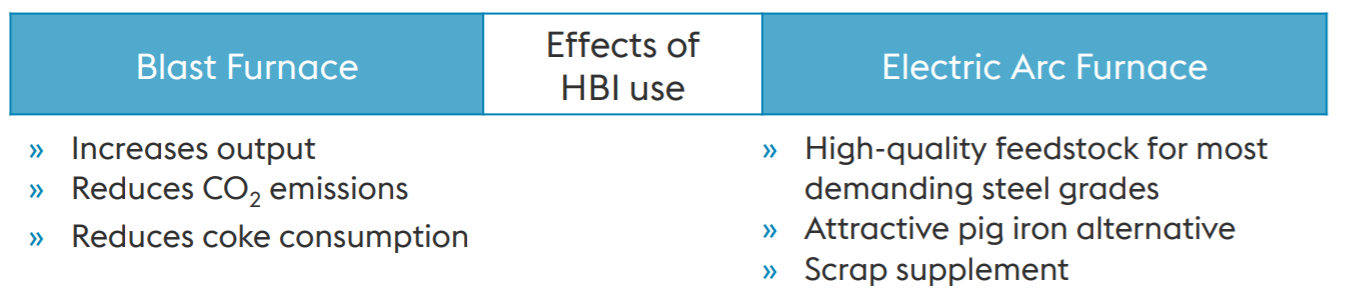

Another concern is that AK Steel was far easier to integrate than U.S. Steel would be. Not only due to its smaller size, but AK Steel also offered the opportunity for vertical integration through the use of Hot Briquetted Iron (HBI) produced in Toledo.

Apart from being a substitute for some of those imports, HBI produced in Toledo will also be used in AK Steel’s Middletown Blast Furnace (BF) at first and later on in the Dearborn facility.

Source: Seeking Alpha

To an extent, this also holds true for U.S. Steel, which offers a lucrative opportunity for Cliffs to utilize its Toledo HBI.

Around 12% (240,000t) of Voestalpine’s HBI output is also being used at Big River Steel EAFs

Source: Seeking Alpha

voestalpine website

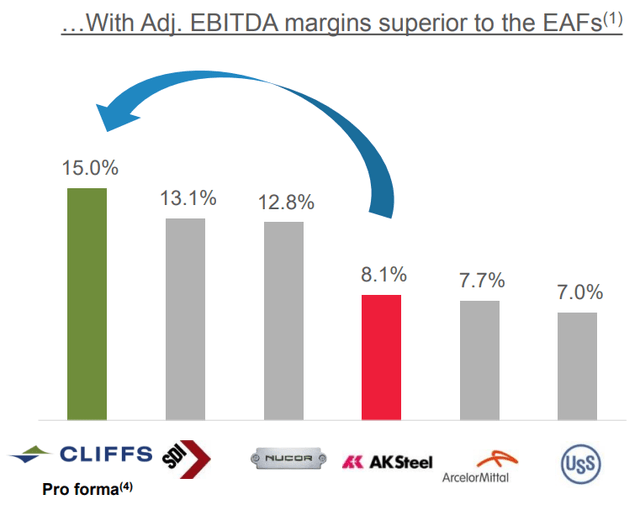

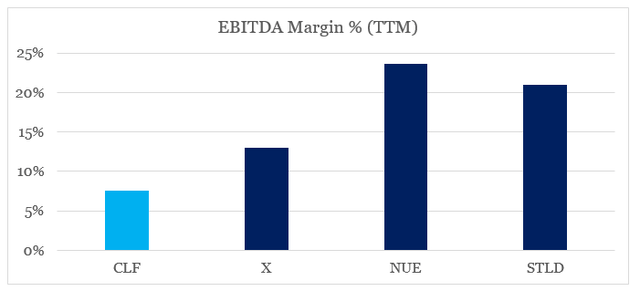

However, Cliffs’ promises for a significant margin improvement following the deal for AK Steel have not yet materialized. As we see below, the management expected that the deal would allow CLF to leapfrog its peers and achieve the highest EBITDA margin in the sector.

Cleveland-Cliffs Investor Presentation

Unfortunately, as of today, Cliffs has not yet achieved industry-leading profitability and is already looking for an even larger deal to accomplish that.

prepared by the author, using data from Seeking Alpha

Whether or not U.S. Steel would be the silver bullet is still up for debate, but it is clear that Cliffs’ shareholders have not yet reaped the benefits from the last two deals (not mentioning the deal for Ferrous Processing and Trading Co), neither in terms of margins nor in shareholder returns.

Seeking Alpha

As someone who saw a lot of potential in Cliffs’ acquiring AK Steel and ArcelorMittal US assets, I would be expecting the management to deliver solid results first and then set its target on the next large deal.

Empire Building

To put it briefly, empire building is associated with management’s desire to expand the business and the total assets under control, without necessarily aligning with shareholders’ interests.

Even though the CEO of Cliffs is among the largest shareholders and to me is one of the best executives in the industry as far as long-term strategy is concerned, his recent actions raise some hard to miss red flags. The strong desire to absorb yet another large competitor and the almost exclusive focus on size of the pro-forma company is a concern of empire building behaviour.

Cleveland-Cliffs Investor Presentation

I highlighted this risk in the past when the appointment of the CEO’s son as Chief Financial Officer and Executive Vice President of Cleveland-Cliffs made me very uncomfortable about ethics within the company.

Seeking Alpha

As attractive as the deal sounds, this is now the third large transaction in a matter of two years and I always grow wary of too many large deals done in a short period of time. This in combination with the recent executive changes makes me uncomfortable and strengthens the case for empire building behavior.

Source: Seeking Alpha

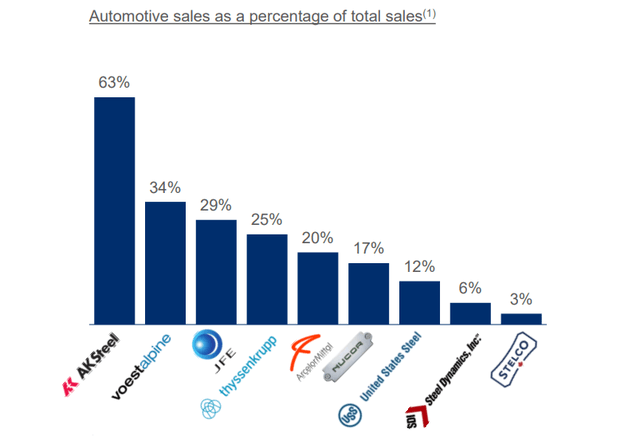

As much as I admire the CEO’s long-term vision for the steel industry, his recent remarks are also becoming increasingly political, and it appears that Cliffs’ monopolistic power over the automotive sector in the U.S. is one of the major reasons for pursuing the latest deal for U.S. Steel.

Our customers are starting to recognize the important role that HBI has played in our carbon reduction goals. With that, we have recently introduced in our invoices to our clients what’s called a Cliffs’ H surcharge, which is a $40 per ton surcharge applied to each ton of steel made with Cliffs HBI, for the ones that work in metric tons is $44 per metric ton.

We deserve to be paid for a characteristic of our steel that truly differentiates us, particularly when compared to other major suppliers of steel to the automotive industry in the United States, in Europe, in Japan, in South Korea, in China or anywhere else throughout the entire world. We also believe that the $40 per net ton Cliffs H surcharge should be passed along by the car manufacturers to the final consumer, and that would only increase the window sticker MSRP price of a car by less than 0.1%.

Source: CLF Q2 2023 Earnings Transcript

After absorbing AK Steel and ArcelorMittal’s operations in the U.S., U.S. Steel’s large exposure to the automotive sector would literally cement Cliffs’ monopolistic power as a supplier to the sector in North America.

Cleveland-Cliffs AK Steel Acquisition Presentation

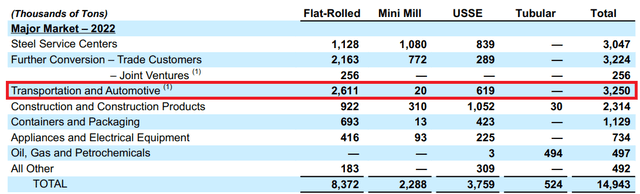

As we see from the latest 10-K SEC filing, the transportation and automotive segment is by far the largest for U.S. Steel.

U.S. Steel 10-K SEC Filing

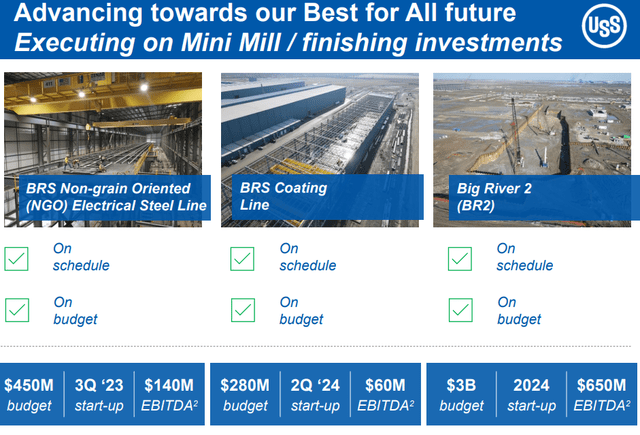

Of course, the company would also give Cliffs significant growth runway with the Big River 2 project, which would be of strategic importance for Cliffs’ HBI and other metallics.

U.S. Steel Investor Presentation

Conclusion

From pursuing key strategic deals with the right timing, it appears that Cleveland-Cliffs is now embracing the mantra of aggressive consolidation at any cost. Even though synergies with U.S. Steel would be significant, the deal holds significant risks for Cliffs shareholders and would not necessarily translate into higher shareholder returns.

Read the full article here