In mid-July 2023, and published on July 24, 2023, I was really happy to be a guest on Seeking Alpha Investing Experts podcast series, hosted by Rena Sherbill. At the end of the interview, I shared my highest conviction and best idea, Advanced Emissions Solutions, Inc. (NASDAQ:ADES). Although I covered the high-level moving pieces, I didn’t provide all of the details. Earlier this week, after reading a surprisingly bearish article, on ADES, by fellow SA Contributor, Henrik Alex, today, I decided to share some additional details with the goal of helping readers connect the dots here.

The Massive Catalyst – The EPA’s (March 29, 2023) Proposed PFAS Regulation Framework

On March 29, 2023, the EPA released its Proposed PFAS National Primary Drinking Water Regulation. For the first time, ever, in the history of the EPA, upon final enactment and signing into law, PFAS will be regulated. Currently, there is an extensive public comment period where wastewater treatment, drinking water, chemical companies, industrial associations tied to public water, and other ancillary participants are interacting. This is where comments, questions, concerns, and pushback gets waged.

This March 2023 CNN article does a good job of synthesizing the high-level and moving parts. Enclosed below is an excerpt from that CNN article:

The proposal would regulate two chemicals, PFOA and PFOS, at 4 parts per trillion (ppt). For PFNA, PFHxS, PFBS and GenX chemicals, the EPA proposes not one standard for each but a limit for a mix of them.

For perspective, prior to this proposed EPA regulatory framework, there were EPA guidelines, that weren’t enforceable, at 70 parts per trillion (ppt) on PFAS.

To help quantify the magnitude of these proposed changes, through a close Wall Street friend, we participated in a one hour expert call. If you move in the hedge fund circles, and are managing tens to hundreds of millions of dollars, depending on the particular investment, it can makes a lot of sense to pay an expensively hourly rate for an expert’s time and knowledge to learn about a particular technology or a regulatory policy proposal. To be clear, in the interest of being thorough, this practice is extremely common within the hedge fund world and is simply one component of a comprehensive investment research process.

I am not at liberty to list the particular industry expert’s name, but I can assure you that he is very credible and accumulated highly relevant experience and knowledge during this extensive career. This was a one hour call with a Ph.D., working as an independent consultant that specializes in water and wastewater treatment. He was a Research Director with two big publicly traded water technologies companies, for north of fifteen years. Prior to that he spent at least six years in industry.

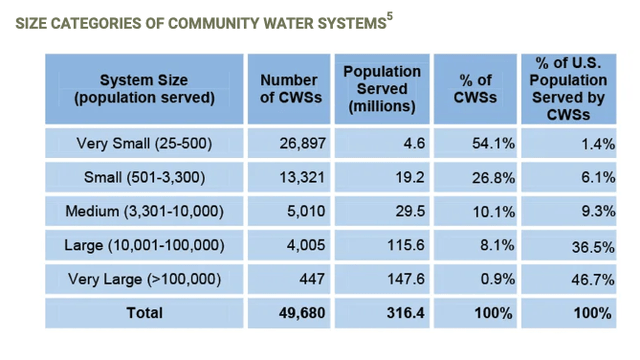

From this conversation, in the expert’s opinion, I learned there is broad and bipartisan support for this new EPA PFAS regulation. PFAS has reached a tipping point moment, in the collective consciousness, of the American public, and the June 2023 $10.3 billion PFAS settlement by 3M Company (MMM) is arguably one of the best signposts of this tipping point. Per this industry expert’s opinion, he would argue that this regulation will get enacted. Now, the targeted enactment date is by year-end 2023, and at which time the roughly 50K municipal/ water treatment facilities, in the U.S., will have three years to comply.

By the way, per this 2015 policy paper, by the University of Michigan, the roughly 50K community water systems number is confirmed.

University of Michigan

Moreover, he said, the final level, once enacted, might get as high as 10 ppt, but he couldn’t see it exceeding 10 ppt. And of course, it is possible final enactment gets pushed a few months, as policy and regulation is a deliberate process in Washington.

As a quick aside, if you’re super intellectually curious, here is a good two page primer on GAC, by the EPA.

My next and logical question was can you help me quantify what that means for demand. He said, and I’m paraphrasing here, back of the envelope, and to capture the trajectory here, only 1% of the 50K water utilities have the technology in place to hit the new EPA standards. He said, if enacted at the 4 ppt levels, upwards of 25% of U.S. water utilities would need to treat this. Secondly, he said, at 10 ppt, roughly 10% to 12% of U.S. water utilities would be legally be forced to treat this.

Now, once finally enacted, and written into law, wastewater treatment facilities will have three years to hit the PFAS standards (get below the thresholds).

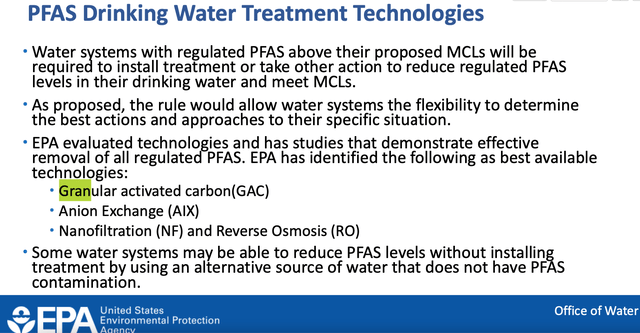

Incidentally, if you review the link to the March 29, 2023 EPA proposal document, the EPA listed Granular activated carbon (GAC) as the optimal solution to screen out PFAS.

See below:

EPA (Office of Water)

Moreover, per this industry expert, in his view and opinion, GAC would be the application of choice for upwards of 90% of the final solutions.

Now, I still need to be able to quantify this and work out how many incremental pounds, per year, of granular activated carbon, will be required by this new policy, once enacted. That said, current demand, before this major policy chance, is about 325 million lbs. per year.

The GAC Math

As I’ve been unable to model the demand, with any precision, and there are various way to do this, at this time, I’m not able speculate and as I don’t to risk incorrectly quantifying the incremental GAC needed (if/when these new PFAS regulations get enacted).

I don’t have access to good information on the amount of GAC required per flow rate. Therefore, without having access to good input data, I can’t attempt to even quantify how much incremental demand this policy would create. That said, directionally, I would argue it is fair to say it could be a meaningful number. Moreover, once enacted, and depending on the final ppt, and depending on sizes and resources of a particular water treatment entity, there is a three-year compliance period. And my understanding is the largest and better resourced water treatment facilities will have to do it sooner.

Calgon Carbon (owned by Kuraray)

In the United States, the largest granular activated carbon manufacturer is Calgon Carbon. Calgon is owned by the Japanese Chemical manufacturer, Kuraray Co., Ltd, which trades on the Tokyo Stock Exchange. To help readers get a better sense of how incredibly valuable GAC production was prior to these major EPA PFAS changes, let me explain.

On June 25, 2020, Calgon announced a $185 million brownfield investment and capacity expansion to its Mississippi plant. The then proposed $185 million investment was designed to add 50 million incremental pounds of annual GAC production. Now, off the record and completely anecdotally, as think about how dramatically supply chain and commodity costs spiked, from 2021 – 2022, I’ve heard the total price tag for Calgon easily exceeded $200 million.

For another input and way to value Advanced Emissions, ADES is currently working on a multi-phased $95 million upgrade to its Red River powder activated carbon (PAC) plant as well as enhancement to its Corbin, Kentucky plant, acquired from its Arq acquisition. Once successfully completed, the new Red River should have 60 million pounds of GAC capacity and 60 million pounds of PAC production.

So if the industry leader, Calgon paid $4 per pound of annual capacity, for its major Mississippi brownfield plant upgrade, then you very logically might argue ADES’s Red River plant GAC production (upon successful completion) is worth $240 million ($4 per pound of annual capacity x 60 million pounds).

As of yesterday, August 24, 2023, ADES shares closed at $1.79 per share. So with 35 million diluted shares outstanding, we’re talking about a company with a market capitalization of only $63 million. As of June 30, 2023, ADES had $67.6 million of cash (inclusive of $8.8 million of restricted cash) and $21 million of debt. As Henrik Alex’s article correctly pointed out, depending on ADES’s second half FY 2023 Adj. EBITDA as well as FY 2024 Adj. EBITDA, there could be a $20 million to $25 million CAPEX/ funding shortfall, to get all of the GAC upgrades, at both Red River and Corbin, KY, across the finish line. That said, ADES still has a number of PAC contracts, that were legacy contracts struck at very low inherent margins, that are rolling off. Upon renewal, ADES has done a good job of resetting these at market rates and with better protections to them (contract duration, and ratability provisions).

That said, upon completion, at 60 million pounds of annual GAC production, valued at $4 per pounds, I would argue that ADES could tap the debt market to fund the funding shortfall.

Said differently, $240 million less $40 million of debt, still means ADES’s GAC production alone should be worth $200 million, again net of debt. $200 million / 35 million shares equals $5.71 per share.

In addition, in this basic back of the envelope modeling exercise, and this doesn’t assign any value to Red River’s 60 million pounds of PAC nor does it assign any value to Arq’s state-of-the-art facility and extensive patent protected portfolio. Lastly, this back of the cocktail napkin math excludes the value of vertical integration and ADES’s thirty year supply of bituminous coal reserves, acquired from its Arq acquisition. ADES will be the only vertically integrated GAC producer of a significant bituminous coal reserve, which is the key input in the manufacturing of GAC.

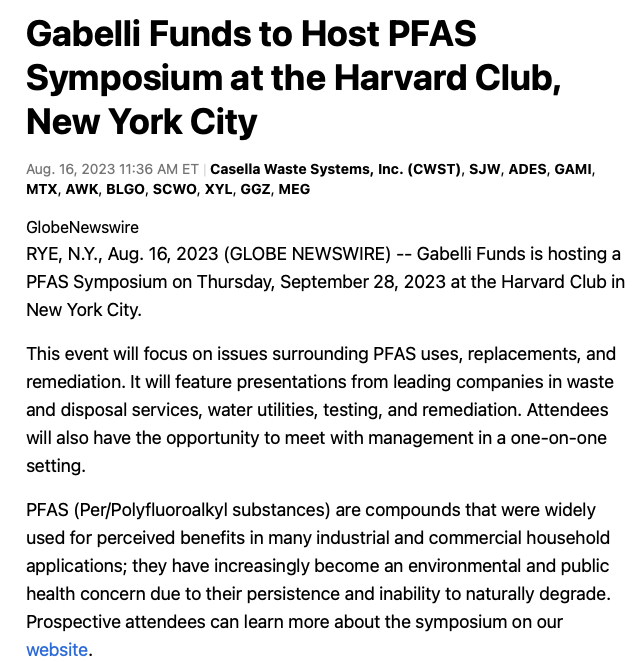

The September 28, 2023 Gabelli PFAS Conference, in New York City

If people still haven’t worked out what a major catalyst and big deal PFAS and the new proposed EPA regulation is then look no further than this August 16, 2023 press release:

Seeking Alpha

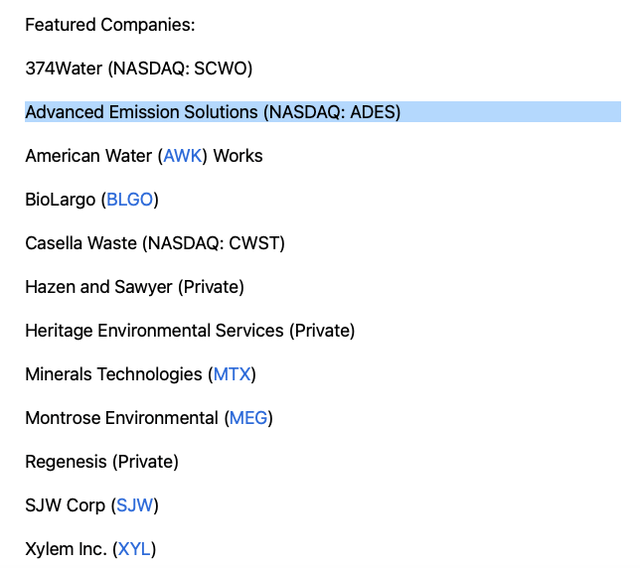

Lo and behold, little old ADES is one of the featured companies that will be there.

Seeking Alpha

Super Mario, Mario Gabelli, is one of the most successful value investors of all time and he runs a good firm. As a good mutual fund manager, a big part of the research process is think far sightedly and understanding/identifying major catalysts and demand drivers before the market does. The last step, once a major catalyst is discovered, is finding direct ways to investment in publicly traded businesses that stand to benefit from a major catalyst.

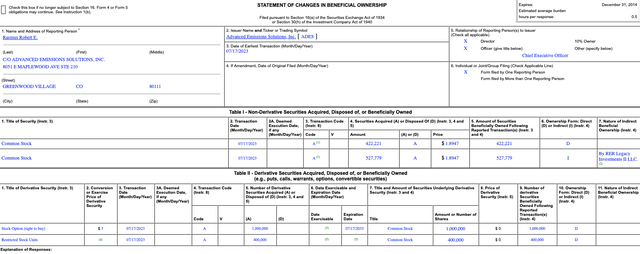

The New CEO, Robert Rasmus, is another positive

On July 17, 2023, Bob Rasmus took over as CEO of ADES. On day one, out of his own pocket (this wasn’t free stock options or restricted stock), Bob acquired 950,000 shares of ADES, at a $1.90 purchase price.

Sec.gov

Moreover, and perhaps more interestingly, he elected to only take a $50K annual cash salary, a modest annual cash bonus, and the vast majority of his compensation is tied to stock options that have at least a $3 strike price. His restricted stock has much higher strike prices.

I haven’t yet had the chance to speak with Bob, and I’m hoping to do so, by mid-September 2023, as I understand, per my conversation with Ryan Coleman, of Alpha IR, Bob is deep in the weeds and has his sleeves rolled up, learning every aspect of the business. That said, at least logically, a seemingly wealthy individual doesn’t take a new CEO role, with only a $50K annual salary, and come out of pocket, to buy shares, unless he was really bullish on Advanced Emissions Solutions, Inc.’s business, valuation, and outlook.

Risks

Trading under $2 per share, at present, ADES has a small market capitalization and is thinly traded. Over the past few months, the stock has moved from $2 per share down to low $1.20s, back to the upper $2.90s, and back down to the upper $1s. As this is really a 2025 story, where management has to prove to Mr. Market that its Capex timelines, milestones, and budget can be met, these are biggest business executional risks. Lastly, given the high interest rate environment, and where this is a big increase in Adj. EBITDA, which is more of a 2026 event, ADES needs to do a much better job courting more of an institutional ownership base. Clearly, there has been too much ‘hot money’ / short-term money that is trading in and out this stock to make $0.25 to $0.50. Also, it possible the EPA’s PFAS ppt higher than expected (higher than the 4 ppt or 10 ppt).

Putting It All Together

At $1.79 per share, ADES currently only has a $63 million market capitalization. On March 29, 2023, the EPA proposed the biggest policy change, on PFAS. Moving from 70 ppt to 4 ppt (and the final numbers, once enacted, might drift a little higher) is a major catalyst for future granular activated carbon demand. ADES in the only pure play and public traded way to directly participate in the future GAC demand, if/ when this EPA PFAS regulation is enacted (and again, if/ when enacted, there is a three-year time period, depending on the size and resources of water treatment facility/ entity to get into compliance).

If you take a step back, I recognize the leading bearish argument is the risk of dilution in order to fund what could be upwards of a $20 million to $25 million CAPEX funding gap, to complete the $95 million of phased Red River and Corben, KY plant upgrades. That said, given how valuable ADES’s collection of assets are here, if the funding gap is the final bridge to require to bring online 60 million pounds per year, of GAC, I would argue ADES could tap the debt market and not dilute the equity holders. As I explained earlier in the piece, at $4 per pound of annual capacity, which excludes all of ADES’s other valuable assets, you get to a $240 million valuation. Even assuming an incremental $20 million of debt, or $40 million of total debt, upon final CAPEX, you arrive at a $5.71 per share valuation for ADES shares. Again, this excludes the value of 60 million pound of annual PAC production, this excludes the value of thirty years of bituminous coal reserves, and excludes the value of Arq’s Corben plant and its valuable and patented portfolio.

Lastly, we have a very smart CEO, in Bob Rasmus, who has his money where his mouth is, who on day one came out of pocket to buy $1.8 million worth of ADES shares. Moreover, Mr. Rasmus accepted a very insignificant cash compensation package and only really gets paid if ADES’s stock performs and trades materially higher than $3, as the strike price on his options was struck at $3 per share.

In closing, I hope this helps readers connect the dots.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Read the full article here