Diamondback Energy (NASDAQ:FANG) has a rather generous cash flow machine. But rather than return the money to shareholders, the company emphasizes per share growth as part of the return to shareholders. That puts the growth story emphasis “front and center” as it has been since the days of the company’s founding. It is very likely that the per share growth emphasis will continue well into the future.

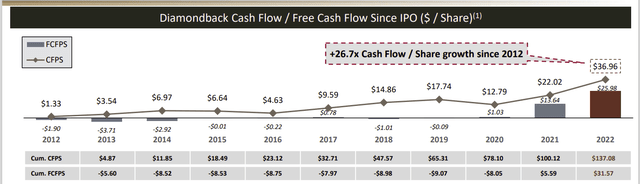

Diamondback Energy Growth Of Free Cash Flow And Cash Flow Per Share (Diamondback Energy Corporate Presentation August 2023)

The fast growth of cash flow per share since the IPO has been top-notch. It may also be of interest to investors that realize that rapid cash flow growth does mean rapid dividend growth. Therefore, by the time one retires, the original investment could be generating a lot of cash just from the base dividend.

Even with lower oil prices expected for the current fiscal year, the growth shown above is impressive. Whatever number will be posted for the current year will likely still continue that impressive growth story.

Other investors may be interested in an entity that is essentially a variable distribution vehicle. However, variable distributions come after opportunistic share repurchases. That is a very different emphasis on dividends from many companies.

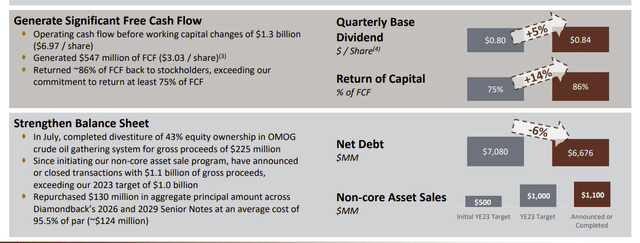

Diamondback Energy Second Quarter Dividend And Debt Progress (Diamondback Energy Corporate Presentation August 2023)

The dividend is being rapidly increased along with the cash flow rise. If management can keep that cash flow pace going, then the dividend could be quite substantial.

A 25% compounded return generally triples roughly every five years. In the first slide, cash flow roughly doubled in four years. Obviously, this year will be a cash flow reversal because commodity prices are lower. But if the ability to double cash flow as rapidly as management has recently done is maintained through accretive acquisitions, then this company is a very attractive investment proposal.

Management has a very long history of accretive acquisitions. That does lessen the risk of an acquisition failure. Furthermore, management frequently cleans the balance sheet by making noncore dispositions to reduce debt as shown above.

The only possible consideration is that if management decides that the debt needs to be lower once the noncore dispositions are completed, there may be a need for a reduction in free cash flow to accomplish that. However, it should be noted that most financial ratios are fairly conservative already, which limits the concern about lower debt.

The market really does not appear to favor organic growth at the present time. But that suits this management just fine. The base dividend growth combined with an occasional special dividend seems to please the market while the growth in per share results is likely to please the market long-term. This management appears to have found a win-win situation.

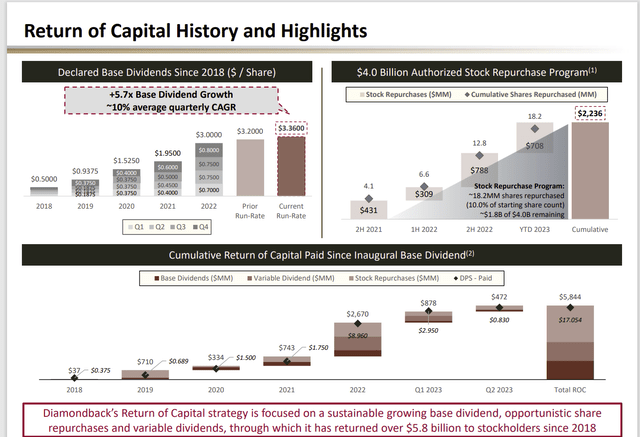

Diamondback Energy Return Of Capital History And Trend (Diamondback Energy Corporate Presentation August 2023)

Investors in effect get a double boost from the accretive acquisitions that use stock and then the repurchase of stock to have less outstanding than was the case before the repurchase.

Now management does make opportunistic purchases a priority in the sense that management is not wedded to a variable dividend as many other managements are.

Therefore, the cash returned through dividends (both base and variable) is probably lower than would be the case elsewhere. But the dividend appears to be growing faster as a result because management is growing per share earnings in two ways (accretive acquisitions and share buybacks).

The company has grown production organically in the past. Now, whether the market would permit such a strategy in the future is very uncertain.

The Investment Grade Advantage

This company has access to lower cost debt than is typically the case in this industry because the balance sheet debt is rated investment grade.

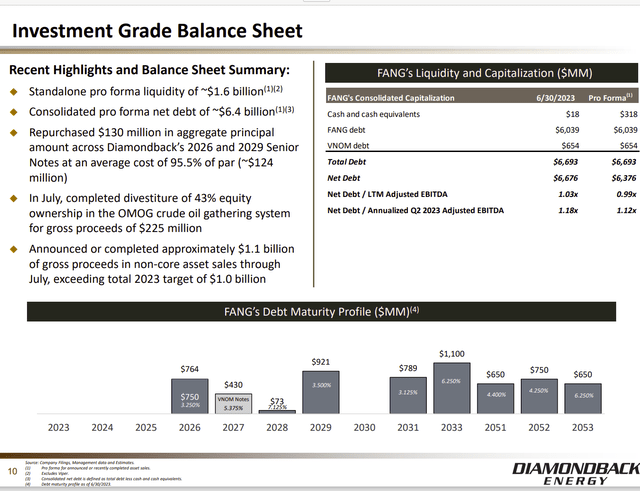

Diamondback Energy Debt Strategy (Diamondback Energy Corporate Presentation August 2023)

Since management has no debt due for a while, and what debt that will come due in the near future is easily handled by cash flow, that gives management a lot of flexibility to repurchase debt.

The Federal Reserve has been raising interest rates. This is a big negative for outstanding bond prices, even though these bond prices “got a boost” when the company attained investment grade status.

But that big negative for bondholders is a positive for a company with cash to retire debt. Diamondback clearly has that cash. Therefore, management can retire bonds that provide the best deal in the long run. Cash flow was boosted by the sale of noncore properties. As shown above, management has boosted that cash flow advantage by retiring debt at a discount. Those purchases are likely to continue as long as the bonds trade at a discount.

This management wants to get the debt ratio under 1 using considerably more conservative guidelines than the current industry conditions. But that really should be no problem given the level of cash flow at the current time.

Key Takeaways

Management keeps making accretive acquisitions that grow earnings per share. Then a portion of the cash flow is directed to opportunistically repurchase shares that raise the per share earnings more. It magnifies the accretive effect of the acquisition.

Finances are conservative enough that the company has attained an investment grade rating. That should mean that this company can survive any cyclical downturn in better shape than many competitors with lower-rated debt. It also gives the company access to lower cost debt than is the case for many competitors.

That makes this potential investment idea a growth story. Income investors either need to look at this as a variable income entity with an emphasis on opportunistic common share repurchases or more probably, income investors need to pass on this idea.

The base dividend is growing rapidly because this company generally grows per share production by double digits. Therefore, the base dividend is likely to grow by double digits in the future.

The main risk in this investment would be loss of key personnel that would result in future stock price underperformance. Of course, there is also a risk of a cyclical downturn because this is a very volatile and low-visibility industry.

But this management has long performed at a level superior to most managements. Long term, they have done pretty well for shareholders. That is likely to continue in the future as long as an investor does not overpay for the common shares. Right now, this is a buy consideration as a result.

Read the full article here