Main Thesis & Background

The purpose of this article is to evaluate the PIMCO Municipal Income Fund III (NYSE:PMX) as an investment option at its current market price. This is a fund I keep on my radar screen because I see value in PIMCO’s CEF offerings across the board on many occasions. I am an avid investor in the muni space, and I have held muni CEFs from PIMCO in the past.

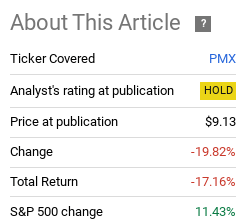

I always keep the national muni PIMCO CEFs on my radar, with a particular eye on relative value between the three. This is a strategy that has served me well over time, including in the short-term. Through this lens I saw a limited opportunity for PMX when 2023 got underway. In hindsight, I was correct to avoid it, but I should have been more bearish than neutral:

Fund Performance (Seeking Alpha)

Given this sharp drop and the fact we are approaching Q4, I thought it was time to do another article on PMX. After consideration, I see a brighter future for this fund than I did eight months ago. For multiple reasons, I believe an upgrade to “buy” is warranted here, and I will discuss them in the paragraphs below.

Valuation Story Has Dramatically Changed

The first order of business when it comes to evaluating a PIMCO CEF is the valuation. This is critical for me because these funds can often go through boom and bust periods. While some investors choose to ignore valuation when buying these products, they do so at their own peril, as there are a host of examples when paying too much for them turns out to be a disaster (this is true for PMX as well for the other muni and non-muni funds the group offers).

With respect to PMX, the story is much better now than it was in December when I turned cautious on it. The current market price actually represents a discount to NAV and that compares favorably to its sister funds:

| Fund | Current Premium to NAV |

| PMX | (6.03%) |

| PIMCO Municipal Income Fund II (PML) | 1.77% |

| PIMCO Municipal Income Fund (PMF) | 1.31% |

Source: PIMCO

As you can see, PMX has a distinct advantage when it comes to valuation right now. Further, in isolation, this entry point is considerably cheaper than where it was when I wrote my cautious article in December. At that juncture, PMX had a premium of a whopping 17% – that should be obvious to my followers why I wasn’t recommending buying it then!

The conclusion here is not to assume that PMX is automatically going to push higher. There are risks to a bull thesis here and I will touch on them in this review. But the point is to acknowledge that the valuation story has shifted dramatically and that should pique value-oriented readers. PMX is just compared to its valuation last here and when compared to its sister funds. That makes this CEF worthy of consideration at the very least.

Manage Expectations – Leverage Risk Is Heightened

Before I jump in to the other attributes I find appealing about PMX, I want to exhibit a word of caution. This is paramount to any article I write but especially in the case of leveraged CEFs at the moment. The disclaimer is that these are highly risky investments and should be treated as such. This type of product is not for the faint of heart – even though the underlying muni assets are some of the most stable one can find in the market. When a fund manager is buying amplified exposure to any asset class, risk goes up, and readers need to understand that and be able to withstand more volatility as a result.

As my followers know, I have been advocating against leverage for most of 2023. I continue to approach it cautiously now – even though a lot of pain has already occurred. So it may seem odd to be recommending PMX given the other articles I have written. In that spirit, readers should recognize this particular investment is not right for everyone. There is a lot of risk right now in a fund like PMX that is leveraged beyond what I am normally comfortable buying:

PMX’s Leverage (PIMCO)

Because of this I think readers need to be mindful of their own allocation. Are they already invested in a lot of similar funds and/or employing a lot of leverage? If so, then PMX probably isn’t right for you. But perhaps you are lacking leveraged plays and/or have too much cash. In that case, dipping your toes in here could work out.

The reason for the caution is the yield curve remains heavily inverted. This continues to pressure short-term borrowing costs while limiting longer-term income opportunities:

Yield Curve Inversion (Bloomberg)

This goes directly against the strategy that would be advantageous for funds like PMX (borrowing cheaply and reinvesting at higher rates). The reality is that as long as this remains the case, PMX is going to face some trouble. Borrowing costs are going to be elevated while income opportunities are limited, which isn’t a great backdrop. To see why this matters to investors, see the below:

PMX’s Costs (PIMCO)

The bottom-line is the leverage is not really helping the fund here because it is costing around 4% and income opportunities on the muni curve are probably only offering around that. So PIMCO is borrowing to break-even if its lucky. And the honest truth is PIMCO doesn’t care so much about that – they get fees either way. Those costs are passed on to the end user – you as the investor – and this means that buying in to leverage at the moment doesn’t offer a lot of advantages. PMX has other positive attributes, to be fair, but this isn’t one of them.

Income Story Mixed

Expanding on the prior paragraph, PMX is seeing its income metrics come under pressure. This is likely due to the leverage and elevated borrowing costs as I just discussed. The point to keep in mind is that PMX faces a very real possibility of an income cut if macro-conditions do not change soon. The good news is it is holding up slightly better than its sister funds. That, combined with the cheaper valuation, are central to why this is the fund I would buy if I wanted exposure to PIMCO’s national muni options:

PIMCO’s UNII Report (PIMCO)

The probably leads readers to a natural question: with this ominous looking UNII graphic, why would one want to buy PMX?

The answer is that the yield has some room to work with. PMX is currently yielding over 5% on the open market and, on a tax-adjusted basis, the net income stream to investors can be much higher than that (depending on an individual’s tax rate). The verdict here is that if one can handle some volatility, withstand an income cut, and currently sits in a high tax bracket, then the distribution may look enticing:

Current Yield (PMX) (Seeking Alpha)

What I am suggesting is that if PMX sees a modest cut and can keep the yield in the 4% range, that elevates the after tax yield above 5% again for higher-income individuals. That remains desirable with inflation starting to edge down. So while the income story doesn’t look great on the surface, I still see it as a buying opportunity for the right person.

September Often Weak Time For Stocks

With some of these headwinds in mind, let me now shift to why one would want to buy munis – and PMX by extension – in the current environment. For me personally I see munis (or bonds as a whole) as a reasonable way to round out of a portfolio for the long term. So having a core allocation makes sense to me in most circumstances. But if we are focusing on right now there are reasons to buy/add to positions given the outlook for equities. This leads me to the underlying notion that munis provide a nice equity hedge, and that is a time-tested relationship.

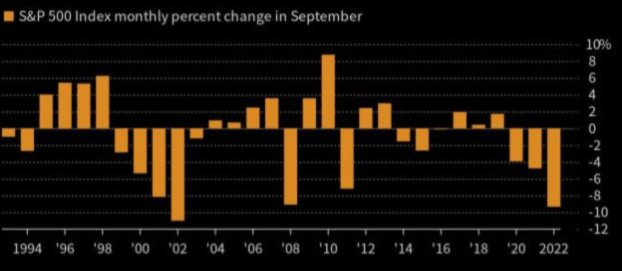

Through this lens, readers should note we are right on the cusp of a new September. While nobody knows for sure what the market will do on any given day, month, or year, history does suggest that September is often a rough month for stocks (as measured by the S&P 500). There have been strong Septembers throughout time, of course, but the most common result is for the index to end the month in the red:

Equity Performance (S&P 500) in September (Yahoo Finance)

What I am getting at here is that equities are likely gearing up for a volatile time period based on historical patterns. This means that front-running this potential outcome via equity hedges (such as munis) could be a timely move. This is central to why I am a likely buyer of funds like PMX for the moment.

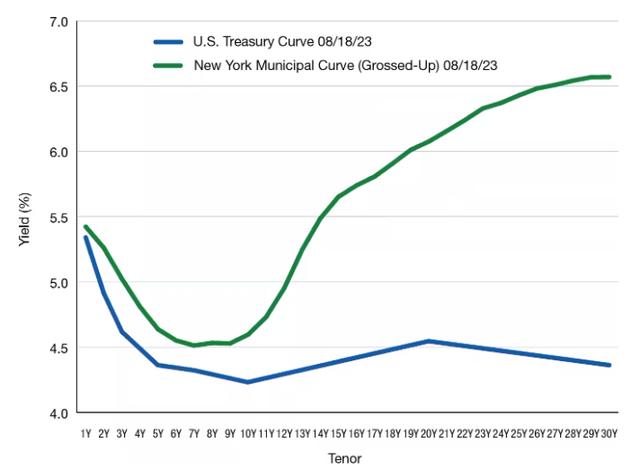

New York’s Yield Curve Looks Attractive

My final point of discussion looks at a developing factor that is positive for munis – especially those from New York. While I highlighted earlier how the treasury curve is deeply inverted and pressuring leveraged CEF’s expenses, the muni curve is starting to normalize. This is great news for investors as fund managers are starting to have more opportunity on the longer-dated aspect of the curve to find higher levels of income. Case in point is New York. A clear representation of how that NY muni curve is steeper than the Treasury curve is shown below:

Yield curve (tax-equivalent yield basis for NY municipal bonds) (Lord Abbett)

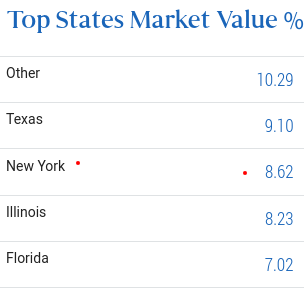

While PMX is a national muni fund and therefore holds issues from a host of different states, it is still relevant to this discussion. That is because NY is a top state weighting in the fund, at almost 9% of total assets:

PMX’s Top State Allocations (PIMCO)

Of course, this is most useful for those muni funds that focus exclusively on NY issues. But I am not a NY resident (although I was in the past) so finding CEFs that are solely NY-based is not a tactical move for me. Being a resident of a relatively low-tax jurisdiction – North Carolina – I prefer funds that offer diversified exposure in the muni realm. That is why PMX remains top of mind, and I view its inclusion of NY securities as a tailwind for broader fund performance given the steep nature of the yield curve at present. This offers PIMCO opportunities to improve PMX’s income metrics if fund managers elect to continue to hold NY exposure in this fund.

Bottom-line

In terms of market price (excluding distributions) PMX is in bear market territory since my last article. While not comforting on the surface, the good news for prospective buyers is the fund’s market price has fallen faster than the underlying value. PMX’s NAV has actually held up reasonably well and that has made a steep premium turn into a healthy discount in its share price.

This leads me to think the worst may be offer, as PMX continues to offer an above-average tax-free yield and exposure to a sector that has historically been a strong hedge against equities. Given we are approaching what is generally a weak time of year for stocks in the U.S., amplifying exposure to hedges may turn out to be opportunistic. As a result, I am upgrading my rating on PMX to “buy” and suggest readers give this idea some consideration at this time.

Read the full article here