Dear readers/followers,

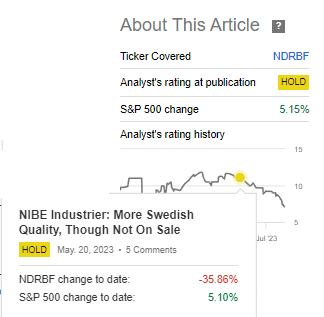

My initial coverage of this symbol of NIBE (OTCPK:NDRBF) came at a time when the company was trading very high. Since that time, the company is down over 35%, confirming my neutral thesis and the estimate that the company was trading much too high/expensive at this particular time.

NIBE RoR (Seeking Alpha)

My own way of investing in this particular business centers around the use of strategic Cash-secured puts during times of weakness. I currently do not have any such options running though due to the generally unfavorable premiums I’ve seen for this company as of late.

Still, this is how I believe one should invest in NIBE when it is that expensive.

In this article, I’ll revisit the company and see if it offers a better upside.

NIBE – Great company, improving valuation

This company normalizing to something resembling an investable price would be quite a feat. That should be clear enough from my first article on the business. Despite it being an impressively high-growth stock, the company does not, as I see it, have the sort of appeal to justify a 32x+ P/E. Not with a yield of less than 0.75%, not with a growth rate even averaging 18-19% over time (some companies do this at lower multiples), and even with the fundamental safety of the business. Since 2019 and since the COVID-19 crisis, this business has been on the valuation equivalent of what I would consider an “acid trip”.

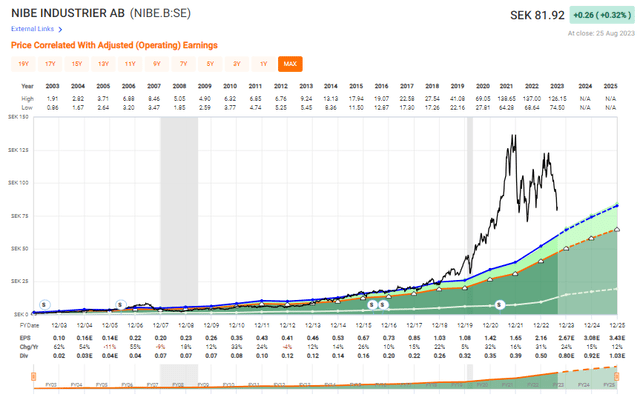

NIBE Valuation (F.A.S.T graphs)

I offer congratulations to those conservative value investors who held it prior and did not sell until the top, but I know of extremely few who had the acumen and foresight (and luck) to do just that. Most of the people I know either bought close to the ATH or during one of the drawdowns, which at this time leaves them at relatively unimpressive levels.

The argument here is that the company now trades at a 10-year average in terms of earnings – but this to me is not necessarily an argument, because this takes the acid-trip period of 2019 to 2023 into consideration.

But more of that later. Results first. These results are a perfect example of why even stellar results won’t save you if your valuation is illogical in an environment like the current one.

Why?

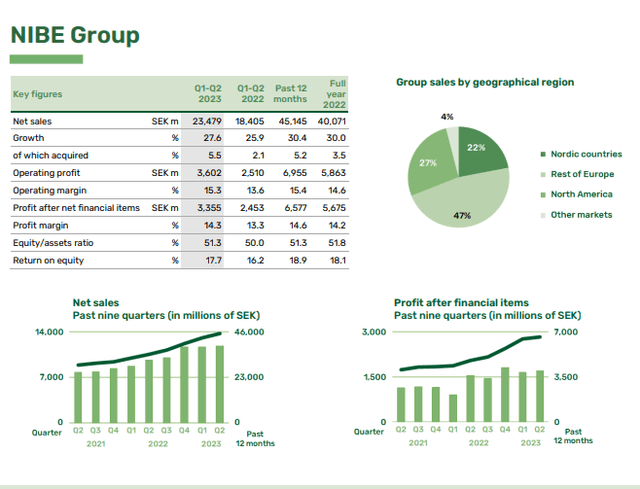

Because the company reported sales increases of 27.6% and still fell. Profit was up almost a billion SEK, and it still fell. EPS was up almost 30% and it still fell. The company had several significant M&As and several key improvements in its fundamentals and processes.

”Demand remained high. This was mainly due to the transition to a more sustainable society in both Europe and North America and to measures taken by end-consumers to mitigate expected continued volatility in energy prices in Europe,” said Gerteric Lindquist, NIBE’s Managing Director and CEO.

“The supply chain situation improved significantly in the latter part of the period as our sub-suppliers’ delivery capacity and delivery reliability improved further. This, in turn, means that we have gradually returned to more normal delivery times and our assessment is that we will have restored our delivery performance in the second half of the year.”

”The acquisitions completed in the period will also expand our market presence and give us new product offerings and good insights into new business models.”

(Source: NIBE 2Q23 Commentary)

None of this, despite all the positivity, caused the company to see anything close to improvements or positive trends in terms of its valuation.

NIBE IR (NIBE IR)

There was no real negative to be had. The company’s sales mix continues to be attractive, the company is mostly in attractive climate solutions, and it remains one of the market leaders or amongst the market leaders in what it does. With a gross margin of over 32%, net margins in the double digits, and EBIT margins close to 15%, it remains a leading industrial – and many analysts even consider it significantly undervalued here, worth well over 130 SEK/share.

I am obviously not one of these analysts.

NIBE Revevenue/Net (GuruFocus)

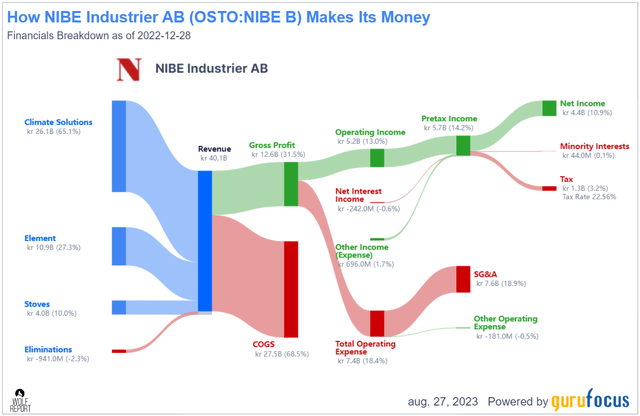

But I will state with clarity that this company offers a convincing business, and streamlined business model, with industrial COGS of Sub-70% and industrial SG&A of below 20%. No matter where you look in the world, if you’re talking billions in revenues if you’re talking a manufacturing business, those are numbers indicative of a very good business model.

There really only are two flies in the ointment when it comes to this company’s valuation case. The first is the yield. The company’s yield is almost zero, and very unlikely to change significantly going forward. Most of the company’s earnings go straight back into the business and R&D. That’s arguably a good thing for a business like this because it does keep them in a market-leading position.

However, it’s also why I’ve “stayed out” for as long as I have, and why you’ve never seen me be bullish on this company.

One more caveat can be mentioned – NIBE is primarily a European/Scandi business. It’s overall international business is low, and this is part of the risk you’re taking,

NIBE also remains an institutional darling. The ratio of sales to buys is extremely skewed to the “BUY” side. Over the past few years, only one sell alert from the institutional side has gone out – the rest are all Buys. Not even the weakness in the last few months since my last article has managed to significantly change this outlook.

To be clear, NIBE is exactly the sort of growth business that I could see myself investing in. But this would require it to trade at the right price. But it does check all my investing boxes in terms of quality and appeal. Another example here in the Nordics is Tomra (OTCPK:TMRAY), and I tend to review this one from time to time as well. Tomra however, is worth more and also at a position where I can consider it undervalued.

NIBE is not.

Worries and things to look at with this company, going forward?

Almost nothing. Most of the analyst’s questions cover specific growth rates and market expansion in NA, specifics for the pump side, and the like. That would also be what I would consider attractive here, but it’s in no way something that would either make or break this company. Volumes and growth is what it’s about here, given that the company reports to be relatively unimpacted on the macro and SCM side at this time.

Also, and this is perhaps the biggest thing, FX. Nothing the company can do about it, but you are investing in a business that’s mostly SEK, and with the SEK currently at historical weakness, this is not necessarily a good thing, regardless of the currency mix in sales.

Let’s look at valuation here, and why the company’s improvement in valuation still doesn’t necessarily put it at as clear an upside as we’d want to, even with the current 2Q23 in the books and results absolutely stellar here.

NIBE – Still Expensive, but getting cheaper.

That the company is at substantially better positioning and upside than when I last wrote about it is undeniable. A 35% drop is nothing small. My previous price target for this particular company was at around 90 SEK/share, and the company is currently at 82 SEK. But in the current market situation, high-valued companies are getting cheaper, and growth companies are getting discounted more and more.

I’m going with a rating upgrade here. My target of 92 SEK/share stands – but it’s a high growth target, and this needs to be taken into consideration. I do not consider NIBE worth 40x P/e as some are wont to do.

S&P Global analysts give the company a target range of 70 to 140 SEK, with an average of around 110 SEK. Despite this, only 3 of the company’s 9 following analysts give the company a “BUY” here (Source: S&P Global). This mirrors my own sentiment on the matter. The company is certainly cheaper, but is it cheap enough?

Maybe.

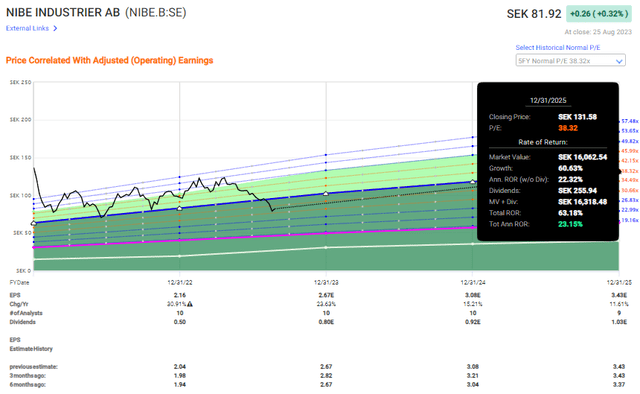

Here is the normalized 5-year upside in terms of P/E.

F.A.S.T graphs NIBE Upside (F.A.S.T graphs)

But again, this includes the sort of acid-trip period we’ve had for the business. In order to both account fairly for the improved growth profile as well as ignore or discount properly for the ZIRP valuation, I believe NIBE should be around 25-31x P/E – and by 31x P/E, I would say that at most. Higher should, on the basis of yield, not be considered valid.

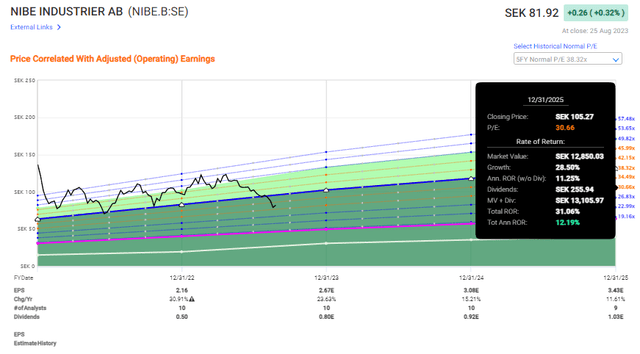

F.A.S.T graphs Upside (F.A.S Tgraphs)

So at 31x P/e, this is around a 12-13% annualized upside. That’s also why 92 SEK PT, at which point we’re barely looking at double-digit upside annualized. Remember, though. I typically look for upsides closer to 15% annualized if I am even to invest.

So despite this being a “BUY”, and despite me seeing an upside here I remain as cautious as ever to invest in this sort of high-growth business unless I can see that I’m getting well-rewarded for the risk I’m taking.

So while a “BUY”, I would still say that there are materially better opportunities for you to invest in with both safer and higher upsides, not to mention clearly better yields and dividends.

That gives me the following thesis on NIBE, as updated for the 2Q23 period.

Thesis

- NIBE Industrier is one of the best industries with a climate focus in all of Scandinavia. It’s a high growth, high safety, and low yield, a combination I have become more interested in over the past few years. However, the company is trading at one of the highest valuations we’ve ever seen barring exuberance, and this makes it a tough sell for me.

- I would say that NIBE needs to fall to clear double digits – preferably below 90 SEK, but at the very least to 92 SEK before I would be willing to expose capital here. I have written options on a continued basis here, trying to “catch” the company at a good price, but so far all I have gotten is a few very nice premiums.

- I am at a “BUY” here – and my PT is 92 SEK/share stands as of the latest quarterly results.

Remember, I’m all about:

1. Buying undervalued – even if that undervaluation is slight, and not mind-numbingly massive – companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn’t go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

The company does not fulfill my valuation-related criteria. Because of this, I view it as a no-go and say “HOLD”.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here