A Quick Take On Warner Music Group

Warner Music Group Corp. (NASDAQ:WMG) reported its FQ2 2023 financial results on August 8, 2023, beating both revenue and EPS consensus estimates.

The firm operates as a music publisher and promoter of musical artists and recordings worldwide through various record labels.

I previously wrote about WMG with a Hold outlook.

With U.S. consumer excess cash balances continuing to be depleted and student loan payment moratoriums ending soon, I’m cautious about an upside catalyst for Warner Music Group Corp.

My outlook remains Neutral [Hold] for the near term.

Warner Music Overview And Market

New York, NY-based WMG develops musical artists, facilitates the recording and distribution of music, and provides music publishing services.

Management is headed by Chief Executive Officer Mr. Robert Kyncl, who joined the firm in January 2023 and was previously Chief Business Officer at YouTube and spent seven years at Netflix.

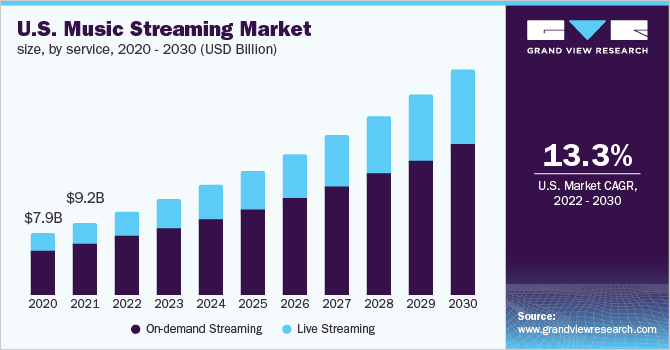

According to a 2022 market research report by Grand View Research, the global market for music streaming was estimated at $29.5 billion in 2021 and was forecasted to reach $101 billion by 2030.

This represents a forecast CAGR (Compound Annual Growth Rate) of 14.7% from 2022 to 2030.

The primary reason for growth in the industry is an expected growing use of streaming platforms that deliver audio to a wide variety of mobile devices.

The graphic below shows the historical and projected future U.S. streaming music market trajectory from 2020 through 2030:

U.S. Music Streaming Market (Grand View Research)

Major competitive vendors include:

-

Universal Music Group

-

Universal Music Publishing

-

Sony Music Entertainment

-

Sony/ATV.

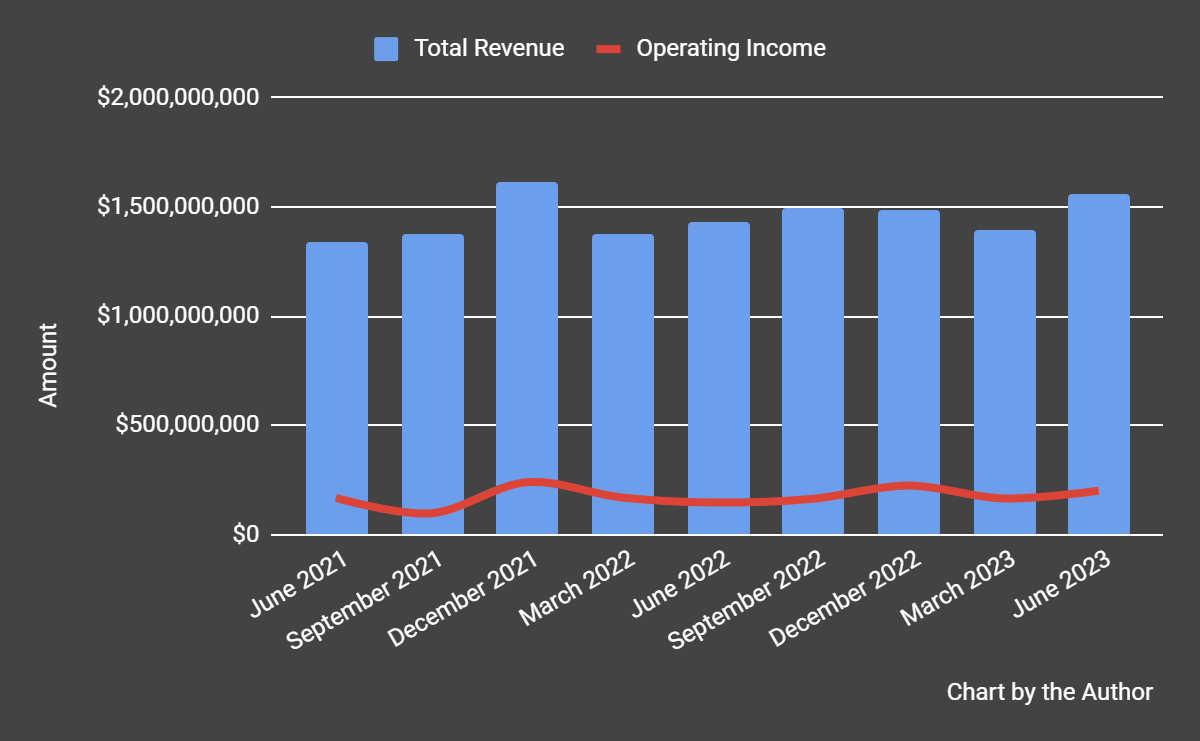

WMG’s Recent Financial Trends

Total revenue by quarter has risen according to the following trajectory; Operating income by quarter has trended unevenly higher.

Total Revenue and Operating Income (Seeking Alpha)

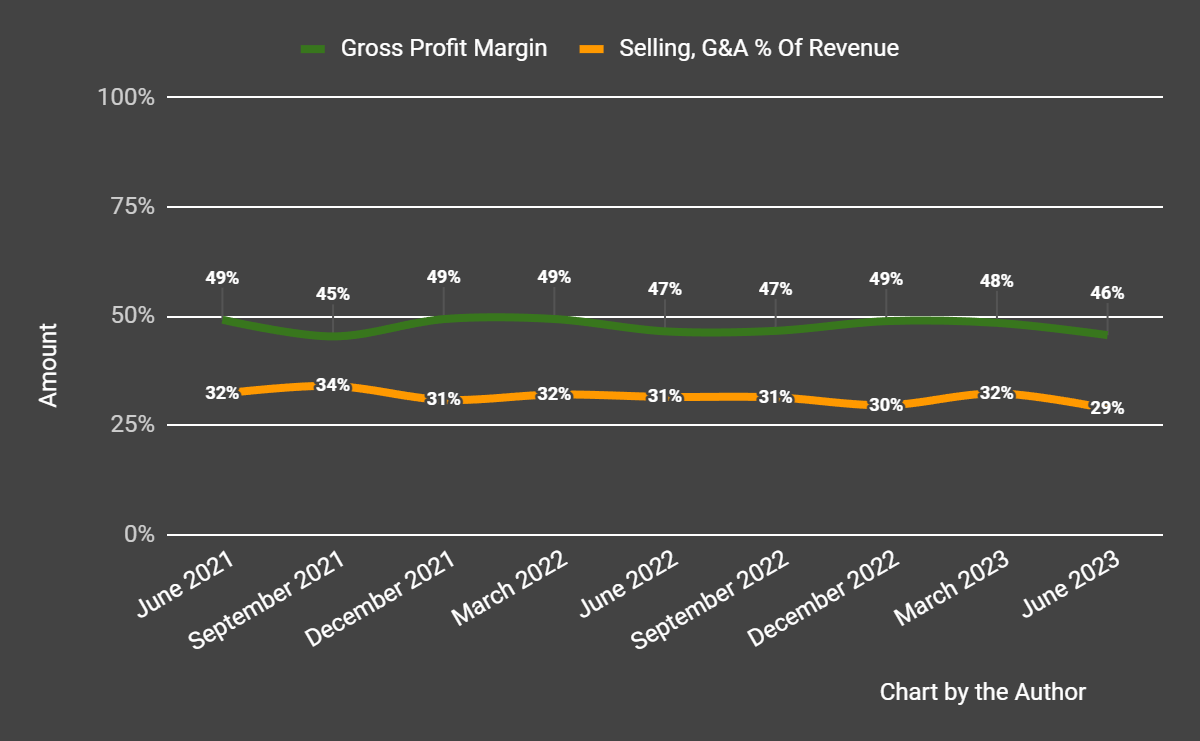

Gross profit margin by quarter has trended lower in recent quarters; Selling and G&A expenses as a percentage of total revenue by quarter have also moved lower more recently:

Gross Profit Margin and Selling, G&A % Of Revenue (Seeking Alpha)

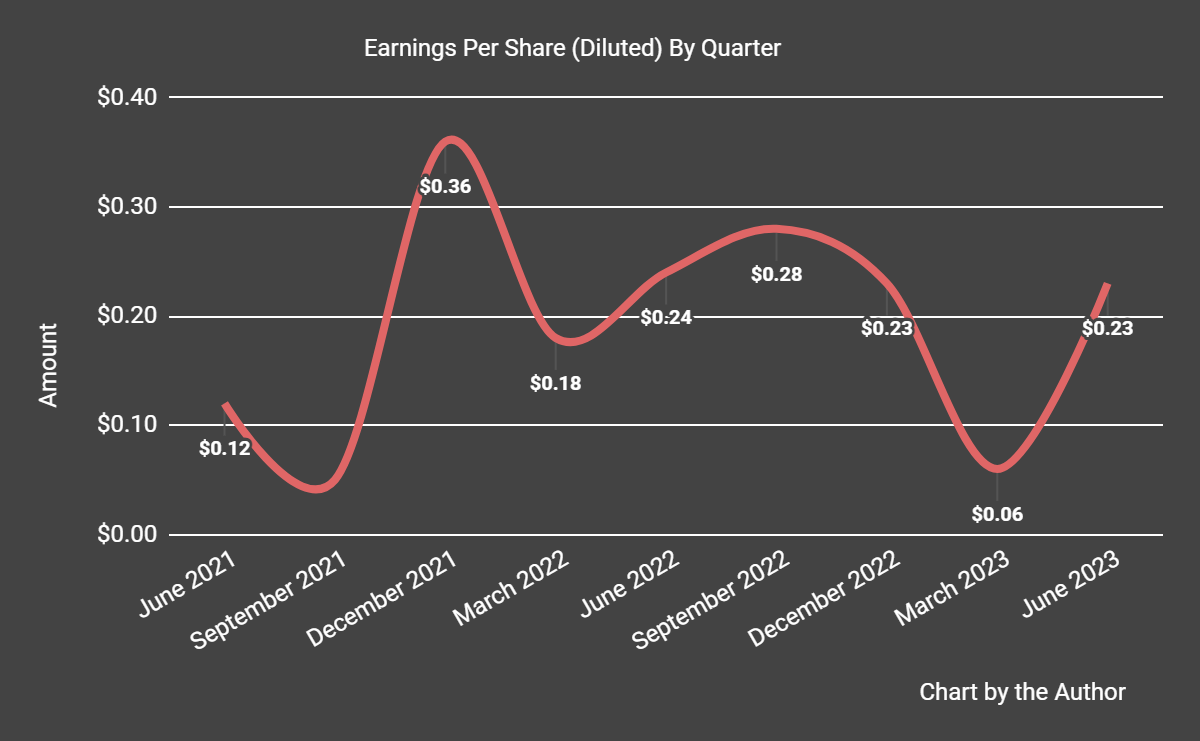

- Earnings per share (Diluted) have been highly variable due in part to seasonal factors.

Earnings Per Share (Seeking Alpha)

(All data in the above charts is GAAP.)

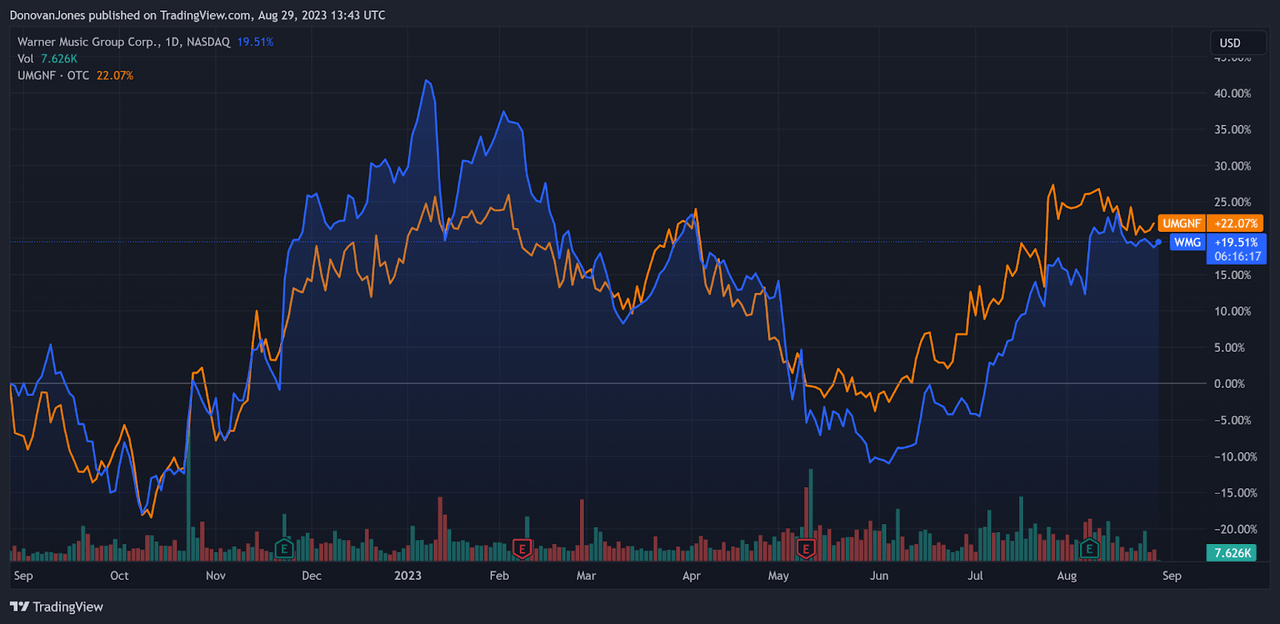

In the past 12 months, WMG’s stock price has risen 19.51% vs. that of Universal Music Group N.V.’s (OTCPK:UMGNF) rise of 22.07%, as the chart indicates below:

52-Week Stock Price Comparison (TradingView)

For the balance sheet, the firm ended the quarter with $607.0 million in cash, equivalents and trading asset securities and $3.99 billion in total debt, none of which was categorized as the current portion due within 12 months.

Over the trailing twelve months, free cash flow was $628.0 million, during which capital expenditures were $127.0 million. The company paid $46.0 million in stock-based compensation in the last four quarters.

Valuation And Other Metrics For Warmer Music

Below is a table of relevant capitalization and valuation figures for the company:

|

Measure [TTM] |

Amount |

|

Enterprise Value / Sales |

3.5 |

|

Enterprise Value / EBITDA |

18.8 |

|

Price / Sales |

2.8 |

|

Revenue Growth Rate |

2.6% |

|

Net Income Margin |

7.2% |

|

EBITDA % |

18.4% |

|

Market Capitalization |

$16,800,000,000 |

|

Enterprise Value |

$20,500,000,000 |

|

Operating Cash Flow |

$755,000,000 |

|

Earnings Per Share (Fully Diluted) |

$0.80 |

(Source – Seeking Alpha.)

As a reference, a relevant partial public comparable would be Universal Music Group; shown below is a comparison of their primary valuation metrics:

|

Metric [TTM] |

Universal Music Group |

Warner Music Group |

Variance |

|

Enterprise Value / Sales |

4.1 |

3.5 |

-16.7% |

|

Enterprise Value / EBITDA |

25.1 |

18.8 |

-25.2% |

|

Revenue Growth Rate |

14.3% |

2.6% |

-81.9% |

|

Net Income Margin |

10.8% |

7.2% |

-33.9% |

|

Operating Cash Flow |

$1,910,000,000 |

$755,000,000 |

-60.5% |

(Source – Seeking Alpha.)

Commentary On Warner Music

In its last earnings call (Source – Seeking Alpha), covering FQ3 2023’s results, management highlighted revenue growth after a ‘challenging first two quarters’ of its fiscal year.

The company saw revenue growth from a wide variety of labels, territories and business segments.

Notably, management touted recent increases in subscription services that license the firm’s music and said that it hasn’t seen increasing churn from end-users.

Total revenue for FQ3 2023 rose 9.2% year-over-year while gross profit margin fell 0.9%.

Selling and G&A expenses as a percentage of revenue dropped 2.7% YoY, a positive signal indicating increasing efficiency and operating income grew an impressive 37%.

The company’s financial position is reasonably strong, with plenty of liquidity, $4 billion in total debt but strong free cash flow of $628 million in the past twelve months.

Looking ahead, consensus estimates for revenue in fiscal 2023 indicate revenue growth of 2.2% year-over-year.

If achieved, this would represent a material decline in revenue growth rate versus fiscal 2022’s growth rate of 11.66% over 2021.

Regarding valuation, in the past twelve months, the firm’s EV/EBITDA valuation multiple has risen by a net of 3.6%, as the chart from Seeking Alpha shows below:

EV/EBITDA Multiple History (Seeking Alpha)

A potential upside catalyst to the stock could include continued strength in consumer demand for music streaming and entertainment content and shows.

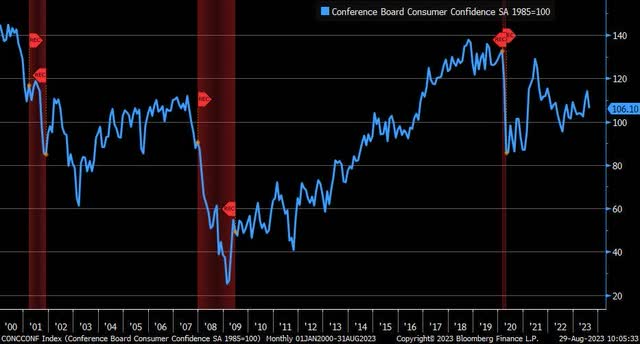

However, U.S. consumers appear to be nearly depleting their excess cash balances, and a number of economists indicate these excess balances may be used up by the fourth quarter of 2023.

The most recent Conference Board Consumer Confidence Index indicated an abrupt drop in August 2023, to 106.1 from 114 in the prior month:

U.S. Consumer Confidence Index (The Conference Board)

Additionally, U.S. student loan deferments are coming to an end in September 2023, with potentially billions of dollars in student loan payments accruing again, reducing spending power from this important demographic.

While the near-term macroeconomic future outlook is so uncertain, my outlook on Warner Music Group Corp. is Neutral [Hold].

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here