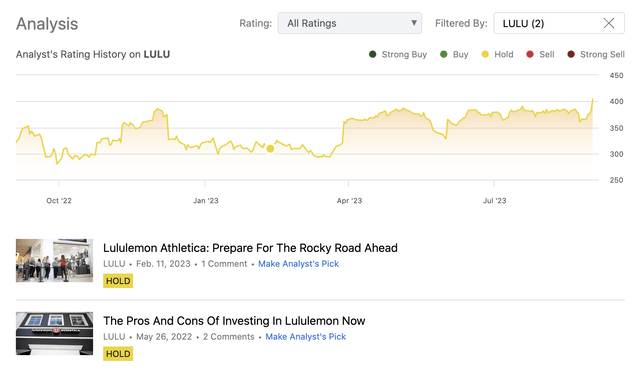

Lululemon Athletica Inc., (NASDAQ:LULU) together with its subsidiaries, designs, distributes, and retails athletic apparel and accessories for women and men. We have initiated coverage on the company is May 2022, with a neutral outlook. In February 2023, we have published a second article, reiterating our “hold” rating.

In both articles, we have highlighted the firm’s impressive growth and profitability, as well as its attractive returns to shareholders as “pros”. On the negative side, we have highlighted relative overvaluation, inventory management and potential headwinds due to the challenging macroeconomic environment.

Since our first writing, the stock price has gone up by as much as 41%, outperforming the broader market, which has gained “only” 11% in the same period.

Rating history (Author)

The aim of today’s article is to give an updated view on the firm based on the latest earnings results and macroeconomic readings.

Q2 results

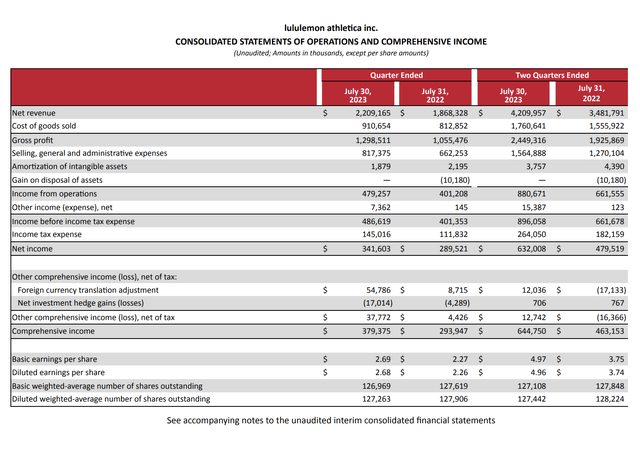

Sales

Just like in the previous quarters, LULU’s second quarter earnings did not fail to impress. Despite the challenging macroeconomic environment, the firm’s revenue has increased by 18% year-over-year, reaching $2.2 billion. The increase has been primarily driven by the international markets, in which revenue has grown as much as 52% YoY, while the growth in North America has been 11%. Important to note that comparable sales have gone up by 11% compared to the same period in the prior year.

Income statement (LULU)

These results are clearly indicating that despite the relatively weak consumer, the firm has managed to keep the demand high for their products. Many other retailers have been presenting significant year-over-year declines in revenue, citing the softer than expected demand. LULU, however, is in another league.

Our performance remained strong in Q2 as both revenue and EPS exceeded our expectations. Our ongoing momentum is a reflection of our portfolio approach to growth, differentiated business model, and innovative product assortment. We are excited about our opportunities in the second half of the year and look forward to continue delivering on our Power of Three ×2 growth plan.

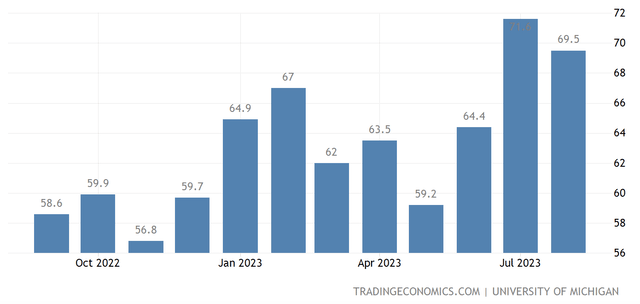

Looking forward, we expect the macroeconomic environment to improve from a consumer perspective. The level of consumer confidence has gone up significantly in the past months, potentially indicating a positive change in the spending behaviour of the consumer. This development could fuel further demand in the coming quarters.

U.S. Consumer confidence (tradingeconomics.com)

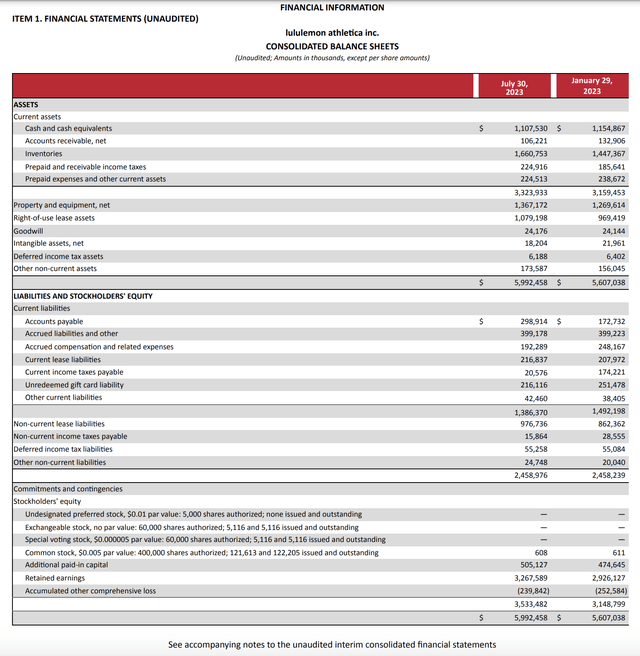

Before we move onto the next section, we also need to take a look at how the accounts receivable have developed, especially in relation to sales. In tough economic times, sometimes, firms try to inflate their sales figures by pulling forward revenue from the near future. It is often done by either selling more on credit or changing revenue recognition rules. Normally, if accounts receivable grow at a faster rate than revenue, it could be a warning sign.

Balance sheet (LULU)

It is, however, not the case for LULU. While revenue has increased by 18% year-over-year, accounts receivable have shrunk by roughly 20%.

Margins

Sales growth is not everything in business. Profitability plays a significant role as well. And the macroeconomic environment, including inflation and energy prices, can have a significant influence on the bottom line results.

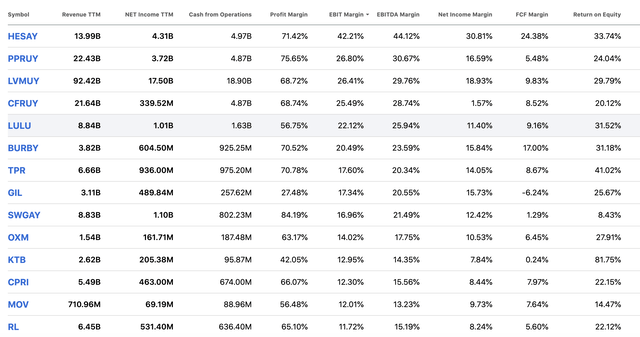

Once again, unlike many other retailers, LULU has actually achieved to expand its margins. The gross profit margin increased 230 basis points to 58.8%, while the operating margin increased 20 basis points to 21.7%. To put these figures into perspective and show how attractive they are, the following table compares LULU’s profitability with its peers’ from the Apparel, Accessories and Luxury Goods industry.

Comparison (Seeking Alpha)

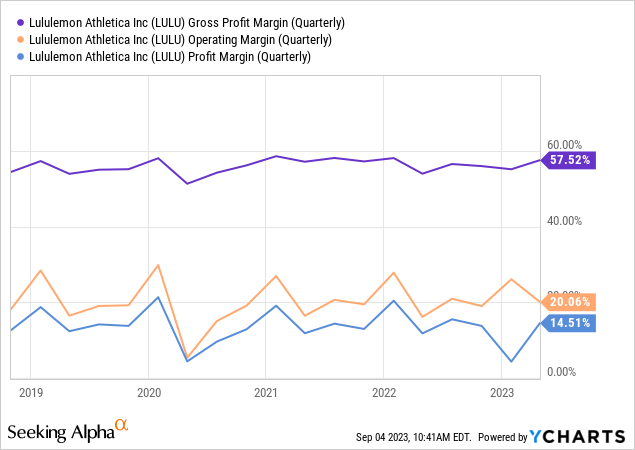

Also important to show, how the margins have been developing over the past years. The following graph shows that, while there have been ups and downs, the firm has managed to keep its profitability relatively stable, despite all the headwinds.

Here we would like to point out two factors that can have an influence on the margins in the near term:

1.) Inflation

Inflation has a direct influence on cost of goods sold, but also influences SG&A and marketing expenses.

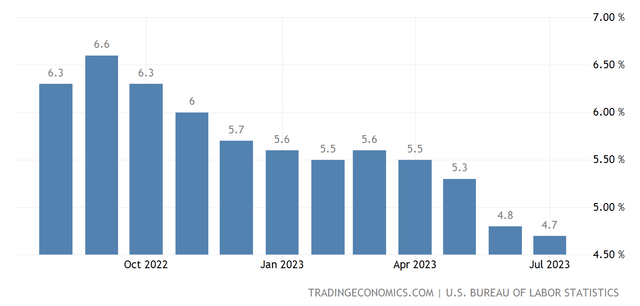

Fortunately, there has been a clear downward trend in the core inflation in the United States since Q3 2022.

U.S. Core inflation (tradingeconomics.com)

We expect this downward trend to continue due to the Fed’s commitment to aggressively combating inflation.

2.) Inventory management

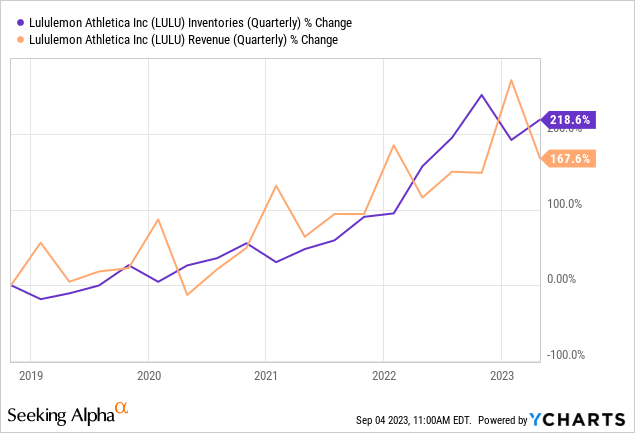

Today, we are much more optimistic on the firm’s inventory management as they have managed to keep their revenue growing. The chart below indicates that over the past 5 years, inventory levels have grown roughly in line with revenue.

For this reason, we do not expect excess or obsolete inventory having a negative impact on the margins in the near term.

Valuation

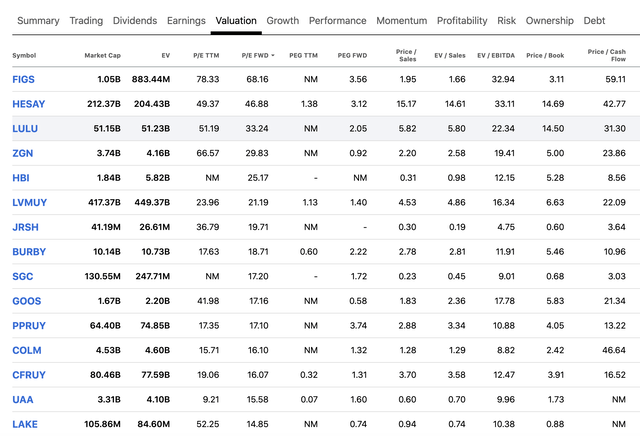

From a valuation point of view, our opinion has not changed much since our last writing. LULU remains to be one of the most expensive firms in the Apparel, Accessories and Luxury Goods industry, according to most traditional price multiples.

Comparison (Seeking Alpha)

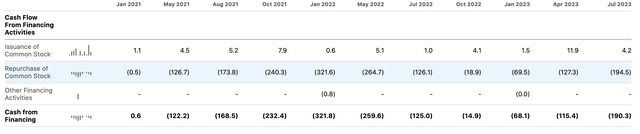

While the firm is indeed growing fast, and it is still committed to returning value to its shareholders in the form of share buybacks, we believe that this premium is too high.

Share buybacks (Seeking Alpha)

Currently, the consumer discretionary sector median P/E Non-GAAP (FWD) is 15.2x. While we do not expect LULU to come down to this level, due to the above highlighted impressive growth and profitability, we would like to see a P/E multiple between 20x – 25x, in order to get bullish from a valuation point of view.

Conclusion

In Q2 2023 LULU has once again managed to deliver impressive quarterly results. Double digit sales growth, expanding margins and improving profitability have been dominating the headlines.

The improving macroeconomic environment, including consumer confidence and inflation, are likely to further boost LULU’s performance in the coming quarters.

LULU has stayed committed to returning capital to its shareholders in the form of share buybacks.

From a valuation point of view, we are still not bullish on the firm, and for this reason, we maintain our “hold” rating.

Read the full article here