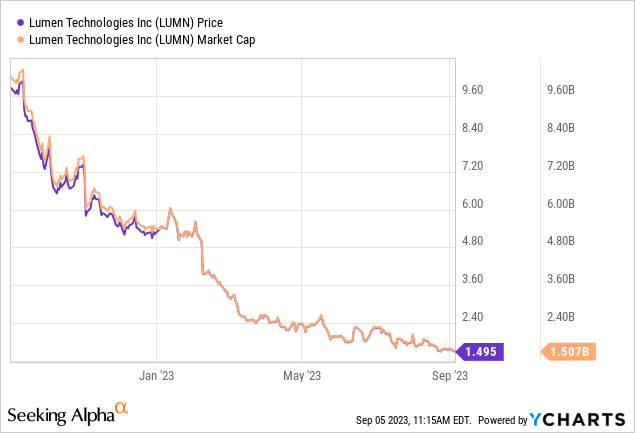

Boy realizes that he can still sell LUMN and lower his taxes

On our last coverage of Lumen Technologies Inc. (NYSE:LUMN) we suggested investors ignore the promises made by management and focus squarely on the exceptionally challenging macro environment for the company. We did offer investors one idea in the capital stack that made far more sense than taking yet another cut from the falling knife.

Century Tel Bonds which have priority in asset coverage are still yielding over 11% for about 2 years out. Rating agencies expect full recovery on these even in the case of a default. So these are areas for a calculated gamble. The Lumen Technologies common stock remains a no-touch situation, as it is trading a 20% free cash flow yield based on optimistic 2027 estimates. Even that free cash flow yield is theoretical, as we don’t think any of it will be returned to shareholders in the very best outcomes. Stay out of the Lumen Technologies common shares. Look at the bonds.

Source: Ignore The Management Outlook, Focus On The Macro

The stock has given a nod to our thesis and has moved 30% lower since then. We look at the Q2-2023 results and update our outlook.

Q2-2023

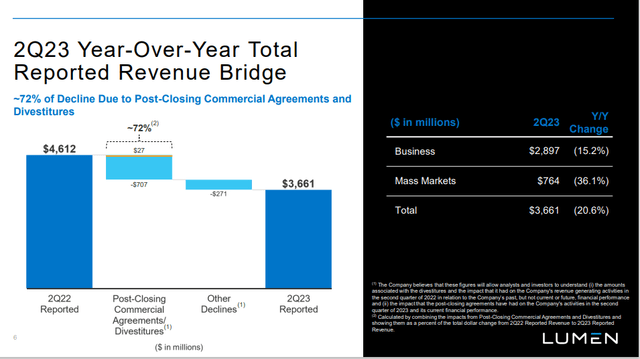

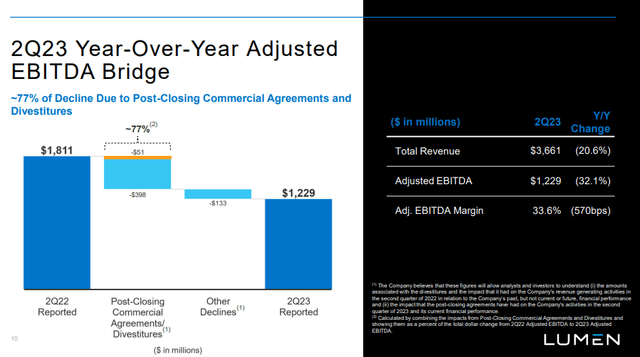

The revenue numbers were about in-line with estimates, with a total decline of more than 20.0% year over year. LUMN painted this into two categories and lumped the divestitures with “post-closing commercial agreements”. That refers to contracts that were not renewed or extended.

LUMN Q2-2023 Presentation

The year-over-year figures are clouded with those, but the quarter over quarter figures get to the meat of the matter. Even here, we see declines, and they are across every single category.

LUMN Q2-2023 Presentation

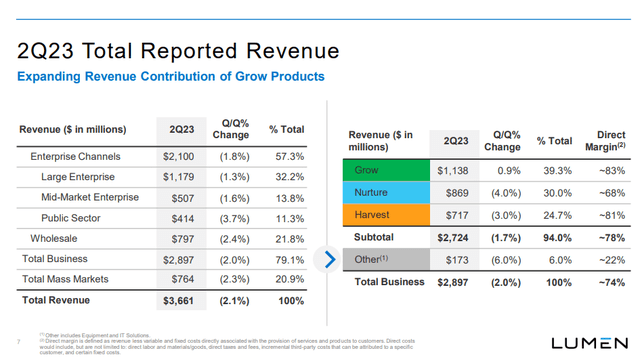

LUMN’s “grow”, “nurture” and “harvest” segments showed a slightly different picture with one actually growing.

LUMN Q2-2023 Presentation

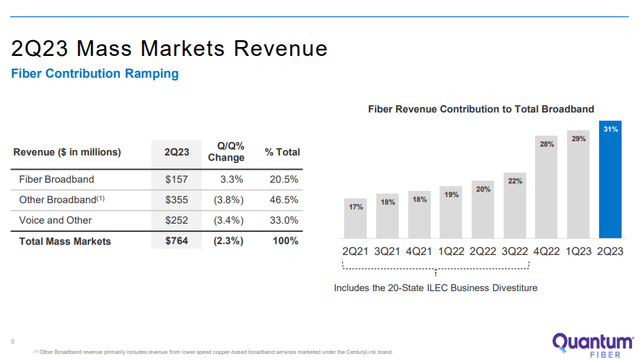

There was no real bright spot in the report, save that fiber broadband moved up by 3.3%. While the contribution to revenues from the Fiber side appears to be accelerating, that is more of an illusion created by other segments continuing to bleed.

LUMN Q2-2023 Presentation

With that deep of a revenue decline, EBITDA drops were expected to be steeper as the leverage model would work in reverse. Total EBITDA was down 32.1% and adjusted EBITDA margin got crushed to 33.6%.

LUMN Q2-2023 Presentation

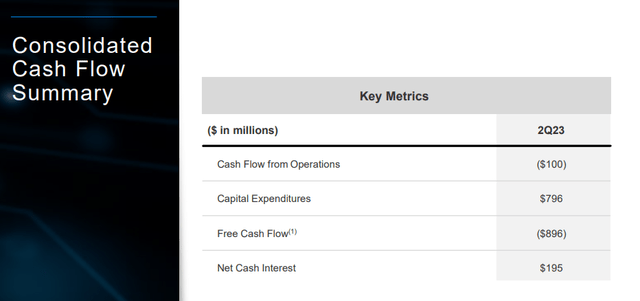

That margin is by far the lowest we have seen since we have followed this company. The last leg of support that bulls had often clutched on to was the free cash flow. We saw this in 2022 when despite the revenue declines, the free cash flow yield drew in many bulls. Well, that is gone as well. With capex of nearly $800 million, we saw a negative $896 million of free cash flow.

LUMN Q2-2023 Presentation

Outlook

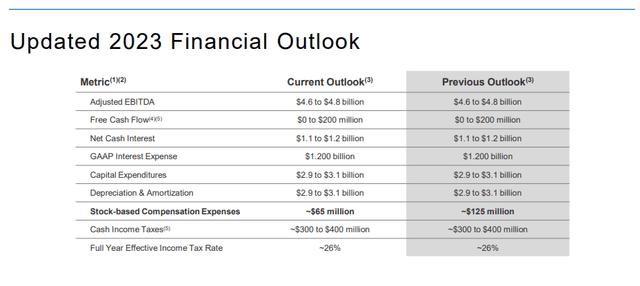

The current guidance for 2023 was essentially unchanged except for the stock based compensation.

LUMN Q2-2023 Presentation

For 2024, consensus estimates point to $13.84 billion in revenues, another 5% year-over-year decline and an EBITDA of $4.45 billion along similar lines. We think both numbers are optimistic, but EBITDA is likely to come further away from the mark than the revenue estimate. We would look for another $3.0-$3.2 billion as a capex estimate. That means we are likely left with yet another free cash flow negative year, coupled with expanding net debt and a rising debt to EBITDA level.

One factor that is allowing this show to go on is the interest expense. At a GAAP level, we are still near $1.2 billion. But this is nowhere near where the markets are. If LUMN was forced to refinance even a fraction of its giant debt load at today’s interest rates, this would game over for the company. While the stress is seen across the bond maturity profile, we can see it in the extremely near-term maturities as well. For example, LUMN’s bonds maturing April 2025, less than two years away, have a yield to maturity of near 23%.

Interactive Brokers Sep 5, 2023

The December 2025 bonds are approaching 27%. Historically, It is amply clear that the market does not expect any of these to be paid off and a restructuring is likely far before that.

What’s The Bull Case?

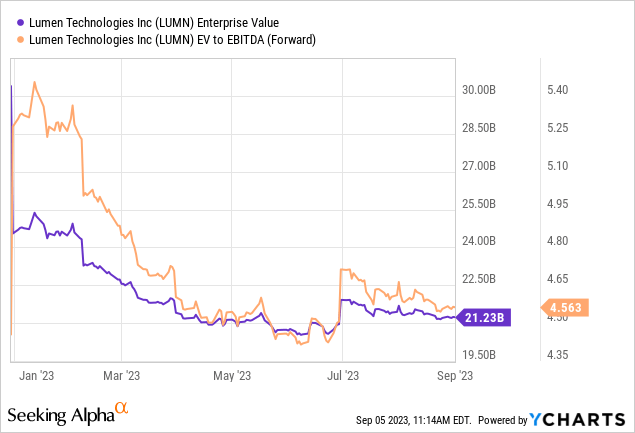

LUMN appears cheap on an EV to EBITDA basis. At 4.6X turns, you are pretty much betting that bankruptcy is in the cards at some point.

The bull case here is that the market capitalization is incredibly small relative to enterprise value.

So any positive news is likely to send the stock soaring higher. Even if you believe fair value is 5.5X EV to EBITDA, well that creates another $4.0 billion of enterprise value in theory and LUMN shares should more than triple.

Verdict

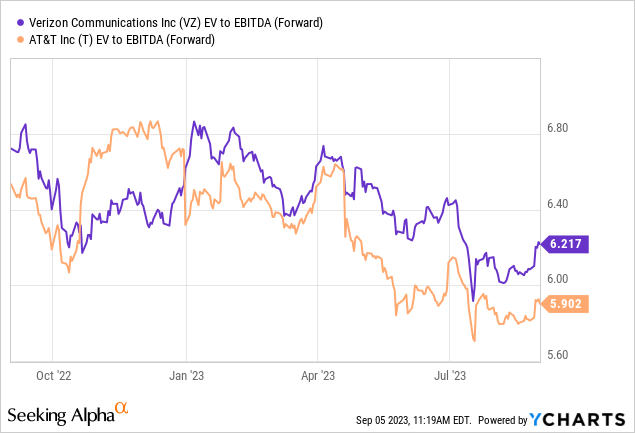

As much as we would like to go value hunting (dumpster diving for the disenchanted) here, we think that management is still not in the right frame of mind. This growth strategy is dangerous, especially with the amount of capex that will be required. Sure, if we were in ZIRP (zero interest rate policy) and investors were salivating at buying B rated bonds for just a 5% yield, something could work out. The whole bond ladder is yielding 25% on average and screaming that this status quo is not working out. While 4.6X EV to EBITDA feels cheap, you get incredibly profitable firms today like AT&T (T) and Verizon Communications (VZ) for near 6.0X.

We just don’t see the juice here in the equity and think it will be visiting the pink sheets within 12-18 months. On the bond side, your odds are slightly better. The April 2025 bonds look the most likely to be paid off, if things go superlatively well. So that is one way to go. If we go past that maturity then the next set of bonds to consider would be whichever is cheapest in terms of price. That would be the September 2039s trading at $27.687.

Interactive Brokers Sep 5, 2023

The good part about these is that current yield is extraordinarily high as well as the bonds yield 7.6% on par and 27.5% at the current price. So if you are bullish, take that 27% plus yield instead of speculating on where the stock goes.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

Read the full article here