It’s been about 13 months since I announced to the world that I’m still avoiding Masonite International Corporation (NYSE:DOOR), in an article with the monumentally original title “Still Avoiding Masonite International.” Although they dropped in price immediately after I wrote the article, since then, the shares have returned 7.3% against a gain of 5.7% for the S&P 500. I should also point out that twenty four hours ago, the stock had “earned” 14% since I last wrote about the business, but yesterday was a bad day for shareholders. Yesterday’s precipitous drop in price has made the stock interesting to me again. Today, I want to work out whether it makes sense to buy back in or remain on the sidelines. I’ll make that determination by looking at the latest financial figures, and by looking at the current valuation as is my wont.

I know that my writing can be taxing, and for that reason I put a “thesis statement” at the beginning of each of my articles. This gives readers a bit more than they get with a title and bullet points, but much less than they get with a full blown article. This paragraph allows you to get in, understand my thinking in broad strokes, and then get out before you’re exposed to too much “Doyle mojo” and correct spelling. You’re welcome. I’ll admit that in many ways Masonite shares are cheaper now than they were, but in a world where it’s possible to earn over 4% risk free, they’re not cheap enough in my estimation. Investing is an inherently relativistic process, and when the risk free rate is 1% or lower, I might bite, but today I’m going to continue to eschew these shares. Put another way, TINA doesn’t live here anymore. Finally, I don’t adore the fact that indebtedness has risen at a time when there are very real signs that growth will slow in future.

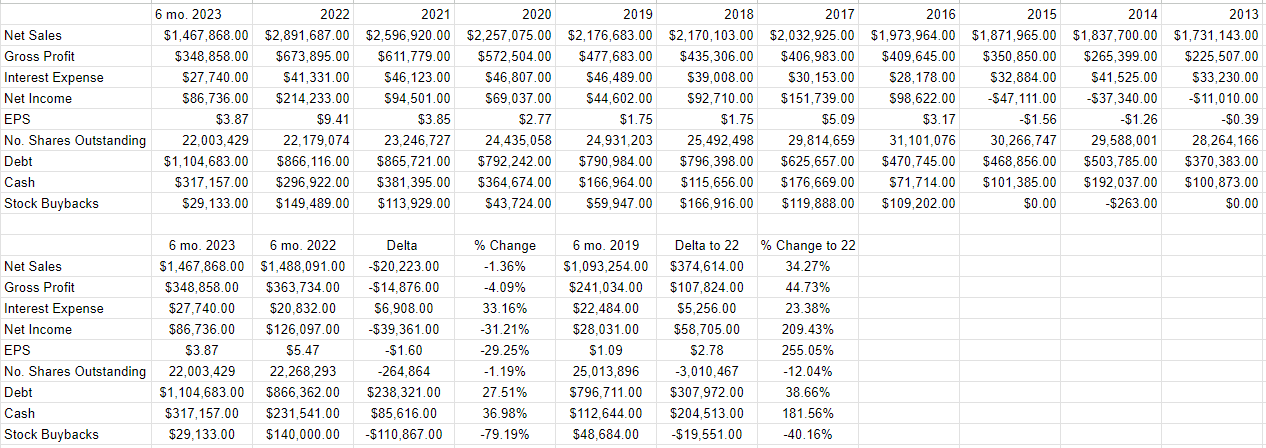

Financial Snapshot

The financial performance for the first half of this year has been fairly bad relative to the same period a year ago. Revenue and net income are down by 1.4% and an eye watering 31% respectively. Net income collapsed in spite of a drop of about $5.4 million to COGS expenses, and a $17 million reduction in income tax expenses. Selling, General & Administrative expenses rose by $26.9 million, and, worryingly, interest expense rose by $6.9 million, or 33%. The fact that we’re now in a world where interest expense represents fully 32% of net income is troubling, particularly because the debt load here is about $238 million higher now than it was this time last year.

So, the risk has actually increased relative to the last time I reviewed this business. The level of indebtedness has increased at a time when there’s some evidence that the industry is turning down. I’d be happy to buy the stock back, as I have fond memories of making money on it, but I’d need to be compensated for the risk with some evidence of a cheap stock and/or an improving macro environment.

Masonite Financials (Masonite investor relations)

The Stock

If you’re a regular, you know that I’m about to point out that the business, and the stock that supposedly represents the business are very different things. The business manufactures and sells doors. The stock reflects the crowd’s ever changing views on the distant future of the business. The crowd can be very capricious, and is affected by a host of inputs in addition to a forecast on the demand for doors in the future. The crowd’s affected by an ever changing appetite for “stocks” as an asset class, and central bank policies. These views change at a much more rapid pace than anything at the firm. For those who would expect that I’d make the point that stocks and the business are different and move on, prepare to have your expectations subverted, because that’s exactly what I’m about to do. Let’s imagine the tail of two Masonite investors. One bought this stock on September 1st (i.e., 5 days ago), and the other bought yesterday around 1pm.. The one who bought five days ago is down about 6% on their investment as of this writing. The one who bought yesterday afternoon is up about 1.4%. Not enough changed at the firm in five days to account for this variance in returns. I should also point out that the person who bought shares when they were cheaper did better.

This is one of the reasons why I try to buy shares cheaply. They come with less risk because they have far less to drop in price, and they offer greater potential reward, because it’s easier for the companies of these stocks to outperform the lower expectations that cheap shares imply.

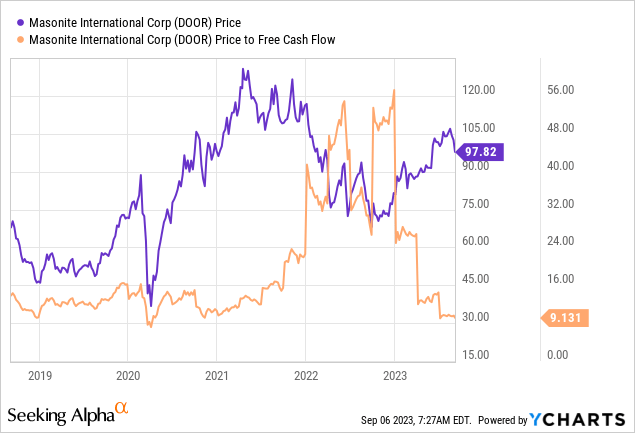

My regulars know that I measure “cheap” in a few ways, ranging from the simple to the more complex. On the simple side, I like to look at the ratio of price to some measure of economic value, like earnings, sales, and the like. I continued to avoid Masonite previously when the shares hit a near record price-to-free cash ratio of 36.7 times. Additionally, I didn’t love the fact that there was no dividend on this stock, at a time when capital could earn a risk free return of about 3.4%. Fast forward to the present, and the risk free rate has jumped to 4.54%, but the market is now paying less than 10 times free cash flow, per the following:

So, I’ll admit the shares are cheaper, but I’m not convinced that they’re cheap enough, when I’m not convinced that there’ll be much growth at a time when debt levels, and interest expenses, are rising rapidly.

As I wrote above, in addition to looking at simple ratios, I also look at more complex measures of valuation. In particular, I want to try to unpack the assumptions currently embedded in price. If you read me regularly, you know that I rely on the work of Professor Stephen Penman, and increasingly Mauboussin and Rappaport to do this. This approach uses stock price itself as a source of information. This method involves “reverse engineering” the assumptions that cause the current price. I’ll admit that this approach involves some high school algebra, and some people find that troublesome.

Anyway, according to my approach, the market is currently forecasting a fairly low growth rate of 2% for Masonite going forward. This seems pessimistic, which I like to see.

The problem for me is that Wall Street seems to be fairly optimistic in its forecasts still. If we assume that the second half of 2023 will resemble the first half, the company will post EPS of about $7.74 ($3.87*2). Wall Street seems to be assuming that EPS will be 21% higher by the end of next year. I don’t want to buy these shares back until all of the optimism has been wrung out of them, and in my view, we’re far from that point. Given the above, I’m going to continue to avoid the shares. I may miss out on some upside in price, but as yesterday’s market activity conclusively demonstrated, the market giveth, and the market taketh away. In the meantime, I’ll content myself clipping fairly decent risk free returns.

Read the full article here