Introduction

John Deere (NYSE:DE) is innovating in order to increase the food security of future generations. Its mission is clearly important and I find in this article that its business operations are a reflection of this. The year 2020 was a clear inflection point for Deere, as this was when operating leverage increased dramatically along with shareholder returns. In the article, I run Deere through the 10-bagger scale and discuss, among other things, secular tailwinds, increasing gross margins, and a strong corporate culture.

Check out how John Deere fairs against the latest companies that I’ve run through the 10-bagger rating list:

The 10-Bagger Rating List

Check out the start of this series in “The Hunt For Potential 10x Returns: 2 Software Giants” where I have calculated the required annualized return to gain 10x returns over different time horizons. The power and influence 10x returns can have on your portfolio is immense, and I believe there are certain factors that correlate with this outcome. In short, this is what the series is all about:

In this series, I will be rating one/two companies based on pre-determined criteria which have been found to increase the chance of a stock becoming a 10-bagger. My goal in this series is hence to give investors a quick checklist of 10-bagger factors for a multitude of different companies to compare with over time. Furthermore, I will be cumulatively adding to a scatterplot each company’s 10-bagger rating and Seeking Alpha Quant rating which we can track over time.

With inspiration from Christopher Mayer and Peter Lynch, as well as my own experience with investing, I have created the following rating list, which ranges from 1-10, with what I believe are the most important factors that contribute to a potential 10-bagger status.

Rating List

- Profitability (“ROIC”), (“ROE”) or (“ROCE”)

- Insider Ownership

- Share Repurchases

- Gross Profit Margin

- Intangibles.

Profitability: Ex. Returns on Invested Capital (“ROIC”), Return on Equity (“ROE”), Return on Capital Employed (“ROCE”).

| Rating | Level |

| 1-2 | <(0)-2% |

| 3-4 | 3-6% |

| 5-6 | 7-9% |

| 7-8 | 10-15% |

| 9-10 | 15%+ |

Insider Ownership

| Rating | Level |

| 1-2 | 0-5% |

| 3-4 | 5-10% |

| 5-6 | 10-25% |

| 7-8 |

25-50% |

| 9-10 |

50%+ |

Share Repurchase (yearly % purchase of outstanding shares)

| Rating | Level |

| 1-2 | <(-5%) |

| 3-4 | (-5)-(0%) |

| 5-6 | ±0% |

| 7-8 | 1-5% |

| 9-10 | 5%+ |

Gross Profit Margin

| Rating | Level |

| 1-2 | Compressing |

| 3-6 | Steady |

| 7-10 | Expanding |

Intangibles

| Rating | Intangible Asset |

| 1-10 | Company Culture |

| 1-10 | Industry Potential |

| 1-10 | Operating Leverage |

John Deere: $119 billion Market Cap

($1.119 billion for 10-bagger status)

| Characteristic | Level | Rating |

| Returns on Invested Capital (“ROIC”) | 15.64% | 10 |

| Insider Ownership | 6.33% | 7 |

| Share Repurchases | 2.27% | 7 |

| Gross Profit Margin | Expanding | 10 |

| Intangibles | Exceptional | 9 |

Total Points: 43/50

Returns on Invested Capital (“ROIC”)

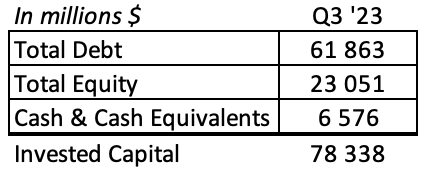

John Deere has a large balance sheet. The majority of Deere’s operations are debt as opposed to equity financed. As of the most recent quarter, the company had a total debt position of $62 billion and an equity position of $23 billion. To understand Deere’s capital structure, it is important to classify its operations into two categories. The first category is selling machinery (agriculture, turf, roadbuilding, and forestry equipment) and the second category is financial services. Deere’s financial services segment is disclosed to have an interest-bearing debt-to-stockholder equity ratio of 8.1 to 1, which implies that the company borrows heavily in order to finance its ‘financing receivables’ of $41 billion (Q3, 10Q). In fact, John Deere Financial Services currently holds $18 billion in short-term debt and $27.4 billion in long-term debt, which makes up around 73% of the group’s total debt position (DE Financial Services 10Q). Hence, the majority of Deere’s debt is attributable to its financial services category. In this category, the business model is built upon borrowing cheap and facilitating loans at high rates. In the most recent quarter, Deere’s financial services unit earned interest revenue (including intercompany) of $1.4 billion, paid $622 million in interest, and earned net income of $216 million (Q3, 10Q). With this clarified, we can better understand Deere’s total invested capital position of $78 billion.

The Author

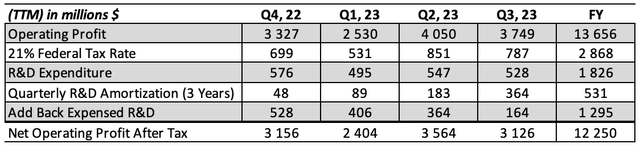

For the sake of this calculation, and in line with my previous articles, I will use twelve trailing months figures and I will adjust “NOPAT” by capitalizing R&D costs for an assumed 3 years. Since implementing the LEAPS strategy, which I discussed in my article “Deere: Incredible Company, But Still A Cyclical” Deere has begun emphasizing R&D, which is structured under one unit within the company, in order to deliver growth. During the latest quarter, R&D expenses made up 3.3% of total revenues. In all, the company’s high operating margin of 23.7% in the most recent quarter allowed Deere to generate a significant amount – $12.25 billion – of “NOPAT” during the “TTM”.

The Author

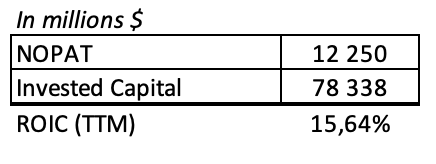

When putting these findings together, Deere had a “ROIC” during the period of 15.64%, which rates highly on the 10-bagger profitability scale. Deere achieves this primarily with a high operating margin and the “ROIC” is even higher for its business operations, excluding financing. The reason for this is that the capital base required to generate revenue for the financial services industry is disproportionately large compared with the company’s primary operations. For these reasons, I rate John Deere with a 10/10 with regard to profitability.

The Author

Insider Ownership

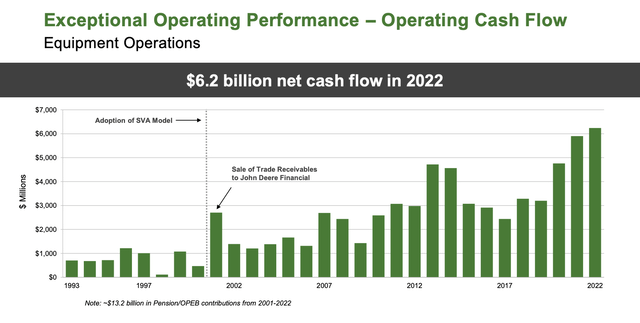

John Deere is by no means a founder-led company. Instead, it is a corporation with clear frameworks and management control systems that are intended to align managers to shareholder value creation. This is reflected through the company’s Shareholder Value Added (“SVA”) framework that it uses to evaluate its own performance. The company implemented this model around 2001 and around the same time, it sold its receivables to John Deere Financial. Since then operating cash flows have steadily increased.

Deere Investor Presentation

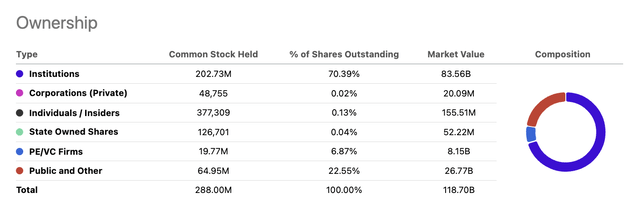

In all, insiders only own 0.13% of the outstanding common stock of Deere. However, given that the company is valued so highly, individuals/insiders still have $155 million in value from their ownership status. For example, CEO, John May had 82 thousand shares owned beneficially and almost 103 thousand exercisable options as of the most recent proxy filing (Proxy Filing). One interesting note, though, is that the company’s CFO – Joshua Jepsen – only owned 1,088 shares and had no exercisable options as of the same period. The most likely explanation for this is that he was promoted to his position in 2022 and his option programs are not near exercise dates. In all, by sticking to the 10-bagger scale, I can conclude that the company earns a rating of 1/10 due to the extremely low level of insider ownership. This by no means should be interpreted as the company is poorly managed or that it doesn’t have any entrepreneurial spirit, but rather that it may not have tight founder-led control.

Seeking Alpha

Share Repurchases

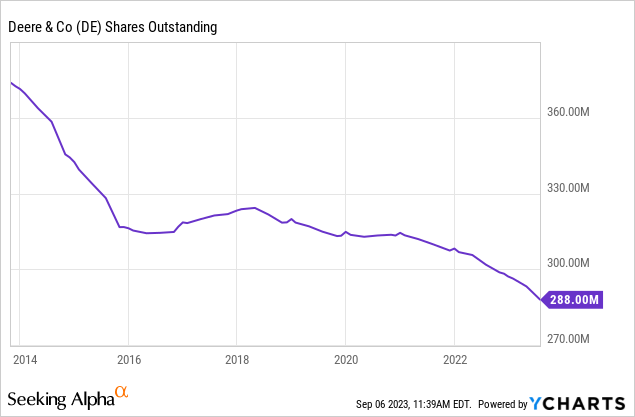

Deere often speaks to its strategic capital allocation priorities in investor presentations. The first priority is maintaining an “A” rating with regard to the company’s loan profile. In order to maintain a successful financing business, Deere is committed to being able to receive “low-cost and readily available short- and long-term funding” (Investor Presentation). The second priority is investing in value-adding activities within the business. The third is maintaining a dividend policy that consistently increases the dividend/share so that the company’s payout ratio is between 25-35%. Finally, the company uses excess cash to repurchase common stock. During the past ten years, Deere has reduced its shares outstanding from 372.5 million to 288 million which represents a decline of 22.7%. This equates to an average yearly share repurchase rate of 2.27%. In the most recent years, Deere has accelerated its share repurchases markedly compared with the period between 2016 and 2021. The reason for this is Deere’s surplus of excess cash during these past years of strong performance, which is in line with the company’s capital allocation strategy.

Gross Profit Margins

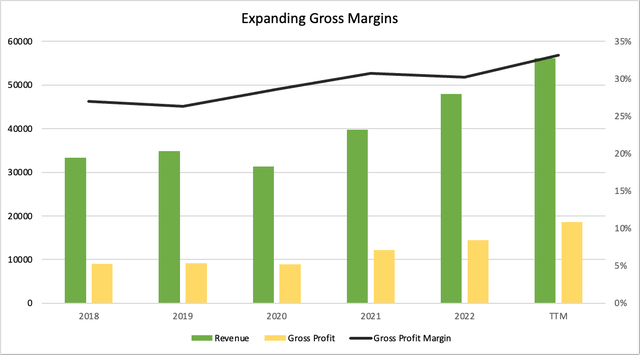

During the past five years, Deere has delivered exceptional gross profit growth performance. The company has grown from having a 26.9% gross margin in 2018 to have a 33.14% gross margin during the “TTM”. Looking even closer, Deere achieved a gross margin of 35.1% in the previous quarter, which means that the company has increased its gross profit margin by about 8.2% over the past five years.

The Author

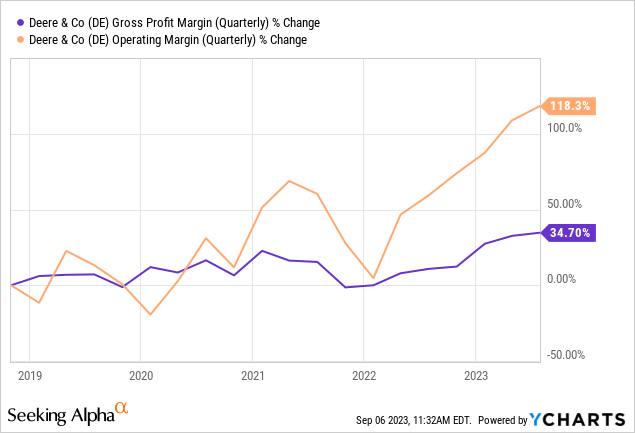

This performance has allowed Deere to drive operating leverage as well. Given that Deere operates within the manufacturing of machinery, a large part of the company’s cost structure comprises the cost of goods sold. Simply increasing gross margins slightly can lead to large increases in the operating profit margin. As shown in the graph below, the 34.7% increase in gross margin during the past five years has actually resulted in a doubling of the operating margin. This can be attributable to the price increases that Deere has realized due to strong demand for its products, especially large agricultural equipment. Based on the performance of gross profit over the previous five years and especially based on how it has contributed to improved operating performance, I rate Deere with a 10/10 with regard to gross margin growth.

Intangibles

| Intangible Asset | Rating |

| Company Culture | 10 |

| Industry Potential | 10 |

| Operating Leverage | 7 |

Average Points: 9

1. Company Culture

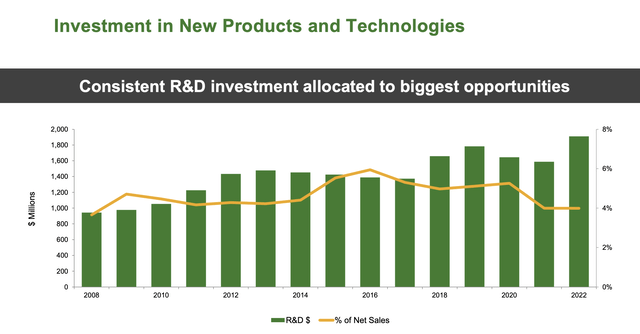

“We innovate on behalf of humanity” (Deere) clearly states the purpose that John Deere has. The company projects a needed 60-70% increase in agricultural production to feed future generations. This is why new, efficient, and productivity-boosting products are a key priority for the company. Innovation is a core pillar of Deere’s culture. Over the past five years, the company has had consistently higher R&D expenditures compared to the prior five-year period. The organization has a clear focus on the “biggest” opportunities. I believe this is extremely important since productivity growth on the farm will be the key driver to delivering the required increase in food production to feed the growing population.

Deere Investor Relations

For Deere, food security is not only an intended outcome for future generations but also the current one. The company partners with many food banks and food security funds, where it invests in food security for communities around the world (Deere Purpose & Goals). This is completely in line with the company’s mission to help humanity. The strong corporate narrative at Deere is rounded off with the company’s final pillar: caring for customers. Deere’s customer focus is evident. During the investor day presentation last summer, Deere brought countless farmers from different regions in the US to present their experience of Deere’s products. This type of customer contact seems authentic and it seems as if Deere embodies these values. In all, I find that Deere has a clear mission. Furthermore, and even more importantly, the company has goals, targets, initiatives, and strategies in place that are all aligned with this mission. For this reason, I believe the company earns a 10/10 with regard to corporate culture.

2. Industry Potential

Agricultural Equipment

Based on projections by Fortune Business Insights, Deere’s largest operating segment is set to grow with a “CAGR” of 7.3% through 2030. This means that the total market size will grow from an estimated $169 billion in 2022 to $296 billion in 2030. Deere has a profound footprint within large ag. around the globe and this segment is likely to become even more lucrative for the company going forward. Based on the company’s 2022 10K, Deere achieved total sales of $22 billion within its large ag. and production business segment. This implies that the company had a global market share of 13% in 2022. As farmers continue to need to decrease input costs within their production, they will continue leaning toward Deere products that provide instant feedback through the John Deere operations center. Furthermore, farmers are likely to continue to adopt products such as See & Spray and general autonomy. Since Deere is so focused on delivering value through investments in R&D, I believe the company will have significantly better products than competitors such as Agco Corp (AGCO), The Toro Company (TTC), and CNH Industrial (CNHI) in the field. The evident tailwind as well as the company’s market position set Deere up well to continue capitalizing on the agricultural equipment industry.

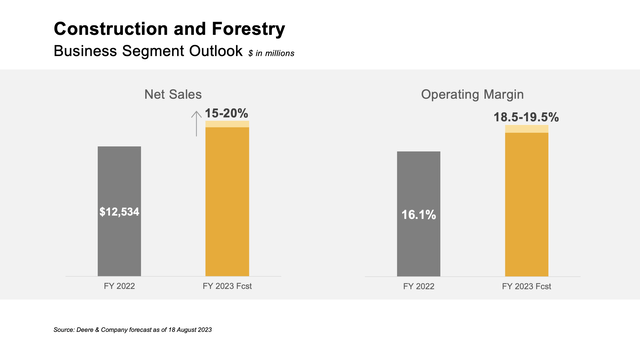

Construction & Forestry

Deere’s smallest segment in 2022 was construction and forestry, where the company achieved net sales of $12.5 billion. Despite this segment only delivering a little more than half the revenue in the agricultural segment, management is optimistic about tailwinds that will support growth going forward. The tailwinds are the following:

- The “successful integration of Wirtgen, the dissolution of our Deere-Hitachi joint venture, and the strategic portfolio actions that have helped us focus the business.”

- Construction job growth and mega infrastructure government spending initiatives: “[W]hile we see nice tailwinds from mega project spendings tied to government funds, most of these projects will primarily benefit 2024 and potentially even 2025, supporting an elongated cycle for construction equipment sales.”

- “We see more and more opportunities to leverage technology into construction, into roadbuilding, in particular, that are going to create real value for customers.”

(Deere Q3 Earnings Transcript)

Based on Global Newswire’s market projections, the global forestry equipment industry is set to grow by a “CAGR” of 4.8% – from $8.96 billion in 2022 to $13.62 billion in 2031. Global Newswire points to several important market dynamics within the forestry industry such as a steady demand for timber used for production, increasing environmental regulation, a consolidating market, and technological advancement. I believe that Deere is conscious of these themes and will be ready to capitalize on them. Deere is developing electric equipment to be used in forestry and has the economic power to consolidate this market. For FY 2023, Deere is forecasting construction & forestry to grow by 15-20%, while the global forestry industry is projected to stagnate or even decline by 5%, while global roadbuilding is projected to remain to grow by 5% in the best case (Deere Q3 Presentation).

Deere Q3 Investor Presentation

Based on Fortune Business Insight’s market research on the construction equipment industry, it seems that Deere has a large market to expand into. Based on the research, global construction equipment will grow from $142 in 2022 to $238 billion in 2030, representing a “CAGR” of 6.6%. When taking these two markets together, global construction and forestry was worth around $151 billion in 2022 which means that Deere had an implied market share of 8.3% in these markets.

Small Agriculture & Turf

Small agriculture is not broken down specifically into a market in any research reports that I found, however for the scope of this analysis I will assume it will grow at a similar rate to general agriculture equipment (7.3%). Turf equipment, on the other hand, is forecasted by Persistence Market Research to grow by 4.5% annually from $13.2 billion in 2022 to $21.3 billion in 2033. Based on the report, growth will be driven by various business purchases and government purchases. Furthermore, while diesel fuel sources are currently the most popular for this type of equipment, the research firm projects electric options to grow very rapidly. Deere has already introduced electric turf products to the market and it is one of the company’s priorities going forward (Deere Electric Turf Product).

Total Addressable Market

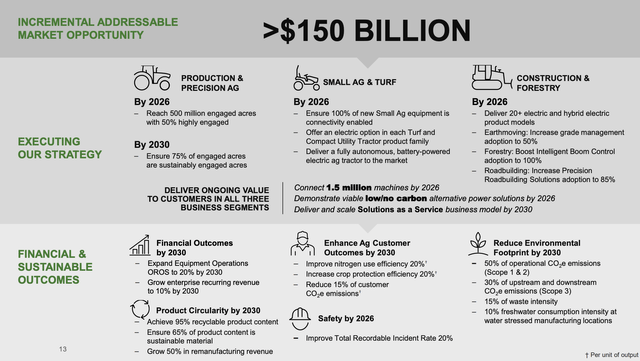

In all, when summing up the various industry market projections, Deere has an addressable market in 2030-2033 of roughly $568 billion. Moreover, the company sees an incremental addressable market opportunity of at least $150 billion from implementing its LEAPS strategy. Based on tailwinds from the secular growth industries that Deere operates in and the company’s likelihood of consolidating these industries through strong product development and brand, I give the company a rating of 10/10 with regard to the industry potential.

Deere Investor Presentation

3. Operating Leverage

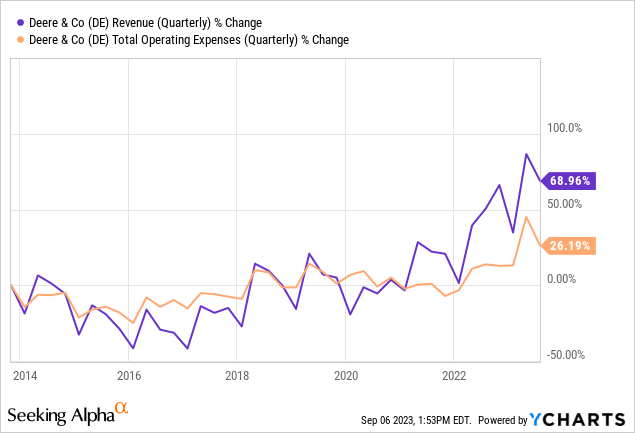

I define operating leverage as a company’s ability to generate the same dollar of sales while incurring fewer operating expenditures over time. Deere, over the past ten years, paints the picture of a company that has struggled with driving operating leverage between 2014 and 2021. However, this trend broke abruptly in 2022 due to hot demand for agricultural/forestry/construction/turf equipment. This demand allowed Deere to realize large price hikes on its machines while also increasing output. The combination of this is the most likely cause of the recent operating leverage. Over the past ten-year period sales have grown by 69% while operating expenses have only grown by 26.19%.

Will this operating leverage hold up as the demand cycle wanes downward? In the coming 2-4 years I suspect that Deere has a high probability of reverting back to a lower level of operating leverage. I suspect this will be due primarily because of slower volume growth and low price increases compared to previous periods. During the long term, however, I believe that Deere has the potential to drive operating leverage even higher than today’s levels. One of Deere’s financial goals is to achieve 10% recurring revenue as a percentage of total sales. The company could be able to achieve this through autonomous products such as full self-driving equipment, See & Spray, ExactShot, and more automated products in development. The adoption and success of these will depend on regulation – as an example, California does not allow for autonomous tractors as of yet (The Robot Report) – and it will also depend on ease-of-use for farmers. Pricing is likely to be less of an issue due to the quick investment payoffs in these new technologies. Since farmer adoption is a difficulty right now, the extent of improvement within this field can either be a headwind or a tailwind for the future potential operating leverage for Deere (McKinsey). For these reasons, I rate Deere’s operating leverage a 7/10.

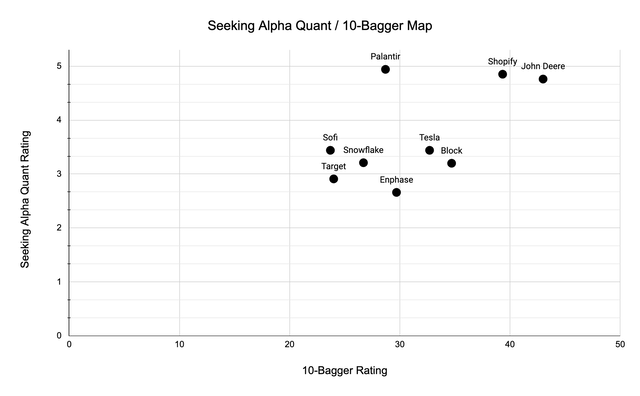

10-Bagger Rating & Seeking Alpha Quant Map

What follows now is a map continuously plotting the companies I analyze based on my 10-bagger rating and Seeking Alpha’s quant rating. This allows us to gauge different companies’ performance over time.

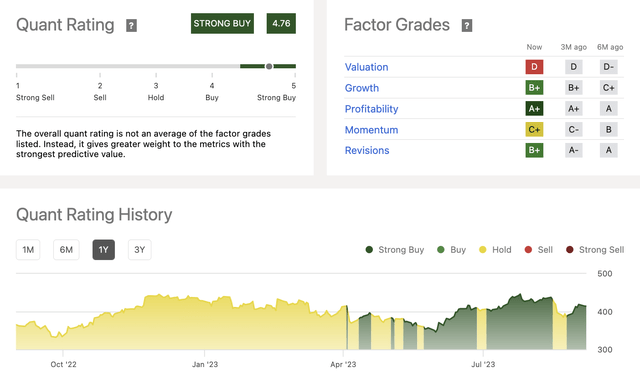

John Deere Quant Rating: 4.76/5.00

Seeking Alpha

Rating Map

In this analysis, I find that John Deere scores a record 43/50 on the 10-bagger scale and a 4.76/5.00 with Seeking Alpha’s quant rating. This is the highest total rating yet, which implies that Deere has the highest 10-bagger potential based on this scale. Similar to the quant rating, I find that Deere has incredible profitability (A+), and strong growth (B+); furthermore, I am also concerned about the rapidly increasing valuation during the past two years (D).

The Author

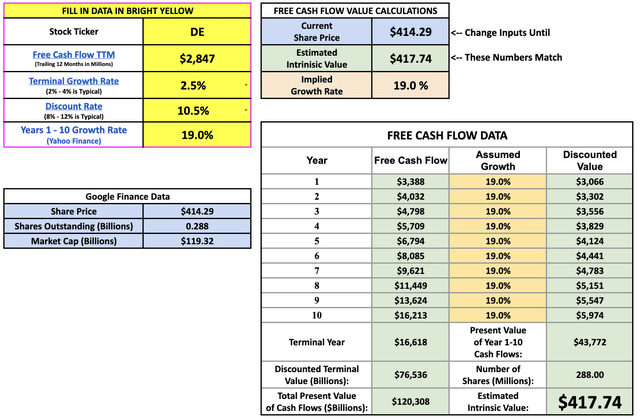

Valuation

John Deere is an ideal company to throw into a reverse cash flow model to the maturity of the business. With this said, one setback is that free cash flows vary heavily historically from year to year. For example, in 2021, the company posted free cash flows of $5.1 billion. Therefore, the implied growth rate of 19% could have been lower given a year of low capital expenditures. I use a slightly higher discount rate of 10.5% for Deere due to the company’s heavily leveraged position, which increases the risk profile of the company. Furthermore, the 2.5% terminal growth rate reflects Deere’s maturity, yet ability to re-invent itself with initiatives such as the LEAPS initiative. So, even though Deere’s share price has increased sharply during the past two years, the price seems to accurately reflect reasonable cash flow generation in the future period. Given that Deere can increase subscription revenues and therefore cash flow margins while delivering on its strategy, I find the current implied free cash flow growth of 19% per year reasonable. In conclusion, Deere has fundamental qualities that could prove the company to become a clear 10-bagger. Furthermore, the current valuation could support this type of stock price appreciation and for these reasons, I rate the company a strong buy.

Brian Feroldi/Stoffel/Withers

Read the full article here