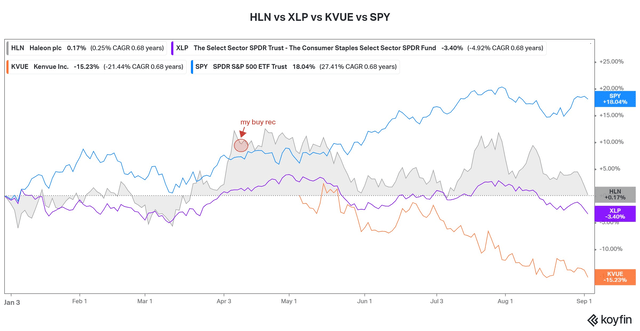

Please see my last article on Haleon (NYSE:HLN) where I went into some detail on the company and tried to explain where I think it is going and what the opportunity as an investment is. Since that note, the share price has slumped. From my initial recommendation, we’ve seen the share price move from $8.77 down to the current level of $7.90. When compared to the broader market on a year-to-date basis, the return is dismal too. If, however, we compare it to its broader peer group in the consumer staples universe (XLP), the performance looks a little better and has taken a step further if we compare to the recent listing Kenvue (KVUE) its relative return is even better. From a timing perspective, it seems like I was a little off to be honest, but the reason I’m referring to both XLP and KVUE too is because defensive stocks have actually had a pretty bad year, especially when compared to high-flying growth and tech stocks.

Haleon vs. Consumer Staples, Kenvue and the S&P500 (Koyfin)

On a year-to-date basis, HLN is up a meager 0.17%, XLP is down 3.4% and KVUE since the listing is off a pretty hefty 15.23%. The latter has fallen more recently because of JNJ exchanging the majority of its stake via a swap for its own shares just recently (at a discount). I suspect that the sudden flurry of liquidity in KVUE has something to do with its sell-off rather than its underlying performance. I digress however as this isn’t a note about Kenvue but its peer and competitor Haleon.

How has Haleon performed?

So how has HLN performed? Pretty well to be honest, in a market where investors are clamoring for big-cap tech stocks and AI-exposed companies, some in the more mundane parts of the market are churning out solid results and being sold off indiscriminately.

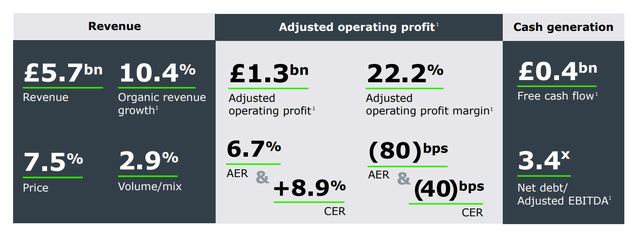

On the 2nd of August this year, HLN released results for the six months ended 30 June 2023 and the numbers were good, in my opinion. See the presentation here.

H1 Performance (Company Presentation)

H1 Organic revenue was up by 10.4% with 2.9% in volume growth augmented by 7.5% of price increases. Very nice to see that a portfolio as defensive as this one can still grow volumes while driving pricing higher. Not all companies can boast of that feat, and many consumer staples peers have surrendered volumes to higher prices during this inflationary burst. (Kraft Heinz is an example) Not this company, however, it’s having its cake and eating it too.

This culminated in first half adjusted operating profits rising by 8.9% in constant currency to just under £1.3bn

FX proved to be a headwind with currency moves shaving 3.5% from the numbers during the second quarter, however, despite this, the company still delivered a beat of over 1.6% vs. consensus.

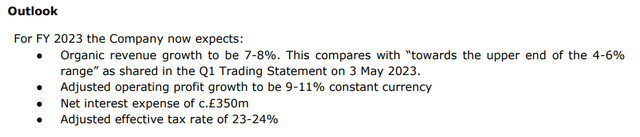

Even more impressive to me, however, was that for the second time this year, they actually raised their FY2023 revenue forecast and are now expecting growth of 7-8% for the period in question, from a prior range of ‘the upper end of 4-6%’. Adjusted operating profit is now expected to grow by between 9-11% in constant currency.

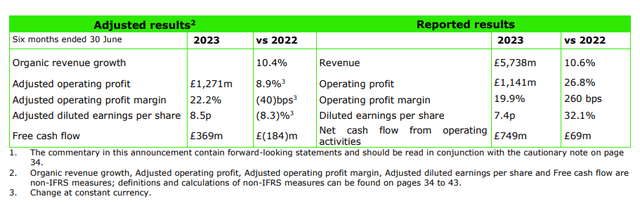

As anticipated in my initial note, portfolio optimization across this newly formed sector would become a trend. Companies are looking for power brands and scale. In this vein, they decided to divest of the Lamisil brand of skincare products to Karo Healthcare, which should result in an inflow of cash of around £250m upon its completion later this year. I’d expect this sum to be used to reduce debt and help the company with its deleveraging efforts. Post the spin-off from GSK, the company was saddled with a chunk of debt, and it has stated that it intends to run that down aggressively via its strong cash generation and other optimization measures such as this divestiture. Net cash flow during the first half was £749m and free cash flow of £369m will certainly help it achieve this goal. Net debt to adjusted EBITA pre this sale is 3.4x, which was down from 3.6x post spin, so they are making headway to reach their goal of less than 3x by the end of 2024.

Result Metrics (Company Presentation)

Power Brands delivering

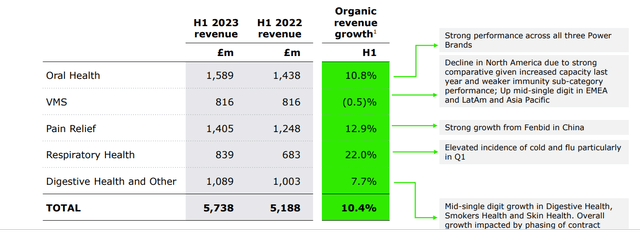

Standout performance from Sensodyne, Parodontax, Panadol, and Otrivin seem to be driving results, as was the reopening in China. Oral Health delivered organic sales growth of 10.8%, OTC pain relief grew by a solid 12.9% and Respiratory Health jumped by a hefty 22%. Thanks to these brands and despite macro headwinds, 55% of the business either gained or maintained market shares YTD, this has resulted in the strong outlook as alluded to above and below.

Divisional Performance (Company Presentation) Outlook Statement (Company Results Announcement)

So, operationally things are chugging along quite nicely with the only real headwind (for now anyway) being currency. Of course, this isn’t anything we as investors or management can do anything about, so although worth noting, it’s really the operational performance we need to watch quite closely. It is however having enough of an impact that management actually made the following statement during results.

Forex Comment (Results Announcement)

If you like myself just see currency moves as a cost of doing business for global companies, it shouldn’t bother you too much. These types of things come out in the wash over time.

Valuation

Now that KVUE has been listed, we can compare them side by side from a valuation perspective.

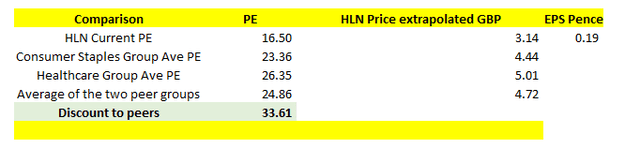

At current prices, both are trading at a PE of around 17x, which is fascinating! By hook or by crook, for the time being, the market is valuing these two companies equally. The result of this is that I’ll remove my 20% discount applied to the broader consumer staple and healthcare peers, as outlined in my last note. With these two trading side by side, we’ll see over time how the market evaluates them independently and as a group of ‘Pure play’ consumer health companies. What we can see however is that they are trading at a discount to their more ‘traditional’ peers.

Valuation Comparison (Analyst)

This discount is also quite significant and at over 30% just feels too steep to me, especially for a company that is performing well in the current environment.

As mentioned right at the top of the article, Consumer Staples has had a relatively bad year in comparison to the broader S&P 500 and that can be seen in both the prices of the sector and in HLN. The average staples PE in April was just under 30 today it’s closer to 24. The whole sector has derated as investors grapple with growthier alternatives and companies that were already well-priced. However, HLN was not only cheap to begin with on a relative basis but as its price has declined along with the sector it remains cheap.

Risks

I’ll point you to the risks section of my last note to get a sense of what one needs to watch with this company, which hasn’t changed much.

The risk of lawsuits needs to be added to this too, as there is a potential overhang that exists from Zantac lawsuits against both GSK and Pfizer. The group is currently not a party to any Zantac claims, however. They also think that they are in the clear with regard to this. Nonetheless, it needs to be noted.

Conclusion

Haleon continues to perform well despite the tough macro and persistent inflation. The result of which has been a further beat and raise in the last results, which the market has largely ignored. As consumer staples stocks have lost their luster this year, Haleon too has seen its share price decline from earlier highs, which not only widens the discount it currently trades at but also improves the margin of safety for long-term investors like us.

Continuing debt reduction is a real positive and is supported by its really strong underlying performance and cash generation. As debt levels come down, the investment proposition becomes even more attractive.

With the macro-outlook becoming even more uncertain in recent months, I remain focused on finding high-quality companies that seem to be trading out of kilter with peers or prospects. I continue to believe that Haleon is one such opportunity.

Haleon remains a strong buy in my books.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here