After getting the long-anticipated reverse stock split over and done with, which heavily weighed on the share price for months, a fresh look at Spire Global, Inc. (NYSE:SPIR) fundamentals and recent operating performance might be warranted. Typically, a reverse stock split, which became effective on August 31, is not well received within the institutional and retail investment community – often preceded and followed by a substantial decline in price. Having said that, most companies undergoing a reverse stock split had been performing poorly for years leading up to this event. This capital measure is also frequently accompanied by an attempt to raise fresh capital, as most of these companies are far away from being cash flow positive.

Quite in contrast to most of these companies, Spire’s subscription-based business is growing at over 30% p.a. with a rather high sales predictability and very attractive unit economics. Adding to that, the company is closing in on profitability with an affirmed guidance to reach cash profitability within the next 6 months. The reverse stock split was necessary to remain in compliance with the listing standards of the New York Stock Exchange, but it was also an opportunity to maneuver the share price into a more investor-friendly price range, for example, making the stock accessible to a broader universe of institutional investors who are restricted from investing in companies with a share price below a certain threshold. Being aware of these factors, management opted for a 1:8 split ratio. It appears management has been successful so far, as the share price rose by around 20% in the first two trading days following the split.

This article aims to address various aspects having an impact on the current share price. In the first part, I will start with a rather comprehensive description of Spire’s business model including its most recent operating performance, as I think the uniqueness and attractiveness of this listed asset is still not well understood within the investment community. In the second part, I will analyze several aspects that have arguably put a drag on the past share price performance. Some insights throughout the article are backed by statements directly coming from Spire with which I had an extensive exchange prior to this writing.

Business model

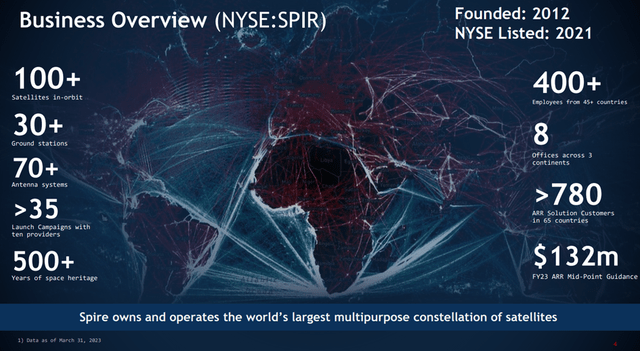

Founded in 2012, Spire is a global provider of space-based data and analytics. Data are sold as a subscription offering and delivered via an easy-to-use application programming interface (API). The company currently operates a fully deployed constellation of more than 100 satellites which primarily consists of its 3U LEMUR cubesat platform. Rather than delivering imagery – which most public earth intelligence companies are centered on – Spire’s multi-purpose nanosatellites are instead focused on radio frequency data. The company is vertically integrated, building its satellites, ground stations (over 70 antenna systems located in 16 countries), and software solutions in-house and selling its offerings directly to customers.

Source: Investor presentation (Spire Global)

The business is divided into four product verticals. Three of these verticals are focused on collecting and selling radio frequency data and analytics:

(1) Maritime data: Comprehensive ocean coverage that combines live data for vessel locations, weather conditions, and global shipping activity (AIS signals),

(2) Aviation data: Historical flight data, ADS-B flight tracking (100M+ position updates delivered daily), and current weather data,

(3) Weather data: Radio occultation (RO) sensors gather a variety of datasets that improve weather prediction forecasts or enable Spire to provide value-added weather predictions.

In my opinion, the weather business has the most growth potential driven by increasing budgets of weather agencies for commercial data purchases and the opportunity for Spire to gradually move up the stack from raw data collection toward value-added weather forecasting. In addition, considering the expense of damage caused by extreme weather events each year ($165 billion in the United States alone in 2022, according to NOAA), other customers beyond civil space and weather agencies represent customer opportunities for Spire.

The fourth business is space services, which essentially provides a hosted infrastructure capability to third parties seeking to establish a presence in space. Space services employs Spire’s fully integrated satellite manufacturing operations, launch expertise, and ground station infrastructure to allow customers to rapidly establish their own constellation in space in a capital-efficient manner. Alternatively, customers might seek to simply host a payload on a Spire satellite or deploy their own software on a Spire satellite. For example, OroraTech recently selected Spire to build, launch, and operate an eight-satellite constellation dedicated to global temperature monitoring (e.g., wildfire monitoring).

Recap of the current operating performance

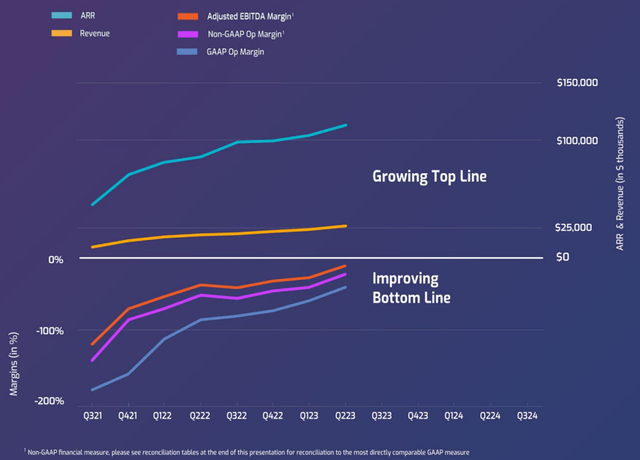

After a record first quarter, Spire delivered even stronger second quarter results with an increase in revenues by 37% y-o-y to a record $26.5 million, which exceeded the midpoint of the company guidance by $2.0 million. During the quarter, Spire added another $8.0 million of annual recurring revenue (ARR), coming in at $112.8 million as of June 30, an increase of 32% over the last twelve months. ARR net retention rate for the second quarter 2023 was 112%, up from 108% in each of the first quarter 2023 and the second quarter 2022. The significant growth in revenues and ARR metrics was driven by new customer additions as well as increased adoption by existing customers as part of their land and expand strategy.

As a result of the substantial operating leverage in their business model, Spire was able to narrow the loss in adjusted EBITDA to $3.0 million, a sequential quarter-over-quarter improvement of $3.7 million that exceeded the midpoint of their previous guidance by $2.9 million.

Source: Q2 2023 Investor Update (Spire Global)

Due to the strong results from the first half of 2023 – having exceeded their expectations for revenue and adjusted EBITDA, among others, two quarters in a row – management raised their margin expectations for the full fiscal year and projected the following notable milestones:

- positive cash from operations in the fourth quarter 2023

- positive non-GAAP operating margins in the second quarter of 2024

- positive adjusted EBITDA in the first or second quarter of 2024

- and positive free cash flow in the second or third quarter of 2024.

Judging from the recent track record and their guidance history, I think there is a good chance that they are going to hit these targets.

Attractive unit economics

I believe Spire – maybe as opposed to other space companies whose business models have significant capex requirements – is capable of delivering highly attractive unit economics over time. Its value-based pricing on the back of a SaaS subscription model allows for a high gross margin profile for its core data/analytics products. By collecting data once and selling it many times, Spire’s business is uniquely scalable with the potential to generate incremental sales with minimal marginal cost. The envisaged growth trajectory is not dependent on illusory production goals, large amounts of incremental capex, or extensive new software development. The main driver relies on the company’s success in its sales efforts and the ability to customize the product technology to address ever-increasing use cases.

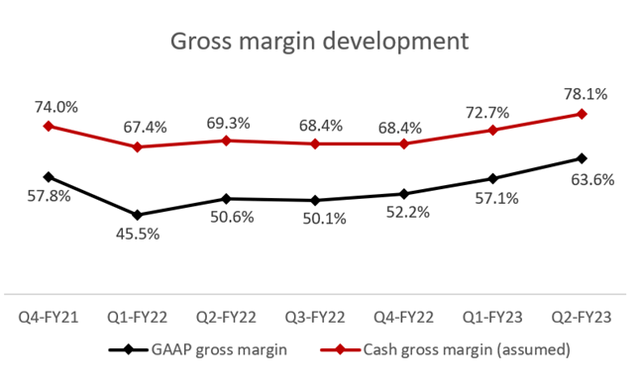

To showcase the operating leverage within the COGS leading to the strong gross margin development over the last couple of quarters, the table below has been prepared. The cash gross margin excludes incurred acquisition-related amortization (in particular, from purchased intangibles) and 90% of the depreciation amount resulting from PPE (rough estimate derived from the PPE composition shown in the notes).

Source: Own calculation based on 10-Q and 10-K filings from Spire Global

A GAAP gross margin and an assumed cash margin of 63.6% and 78.1% respectively in the most recent quarter speak for themselves – not that different from the gross margins of typical software SaaS companies. Assuming the company stays on track for over 30% annual revenue growth, the favorable operating leverage and the capital-light nature of the business model might generate significant annual recurring free cash flows in 1-2 years from now with a long-term free cash flow (“FCF”) margin substantially above 10%.

With regards to future capex requirements, it’s paramount to understand that Spire’s satellites are software-defined – meaning that new capabilities do not necessarily always require new satellites and instead can be inserted onto the existing fleet via a software upgrade from a ground station uplink.

Finally, in terms of competition, by focusing on the RF space, I think the company is better positioned relative to other space companies. The better-known and well-capitalized players are either operating in the imagery or communication field and according to the company’s CEO Peter Platzer, competition is rather expected to occur within the respective fields and less across them. Spire has a first-mover advantage in the radio frequency sensing market with over 500 years of accumulated experience and know-how as to how to operate devices and sensors in space. To replicate the company’s current fully vertically integrated platform – with its proprietary constellation, network of ground stations, pool of domestic and international licenses, and data analytics solutions – potential competitors would need to risk a lot of money and time in the first place in order to be able to compete with Spire across their product offering.

Innovation engine

One of the major reasons why Spire is still not profitable relates to the fact that management decided to keep investing in its proprietary technology. Over the last twelve months, the R&D expenses accounted for around 40% of revenues and have been sequentially rising in absolute terms to $9.8 million in the most recent quarter. The company is willing to tinker around which fosters its ability to innovate and introduce new solution sets and capabilities for customers. For example, RF signal geolocation is a new capability recently developed by Spire. This new technology is able to detect and locate RF signals with its existing fleet of satellites – a capability that was inserted via a software update taking advantage of the software-defined nature of its satellites. That’s why its already deployed LEMUR satellites can now be used to detect the source of Russian electronic warfare jamming/ spoofing signals in Ukraine.

Another example refers to satellite communication where Spire recently announced that the company is one of the first to successfully qualify, demonstrate, and operationalize optical inter-satellite link (OISL) technology on a nanosatellite. This technology which is inserted on its newest satellites improves data transmission speeds, data security, and constellation capital efficiency (e.g., fewer satellites required to provide the same capability) opening new use cases that were previously prevented from data bottlenecks. To underscore the importance of this technology, it needs to be noted that the development was funded partially through the European Space Agency (ESA) and the UK Space Agency (UKSA).

Its unique R&D capabilities were showcased once again last week when they announced that Spire was awarded a $4.6 million, 12-month contract by NASA on behalf of the National Oceanic and Atmospheric Administration (NOAA) to participate in a study in which Spire will compete with three other companies (Northrop Grumman being one of its competitors) to develop a Microwave Sounder for NOAA’s Near-Earth Orbit Network (NEON) program.

NOAA contract

In March 2023, Spire has been awarded an Indefinite Delivery Indefinite Quantity (ID/IQ) contract by NOAA to compete for orders under a $59 million ceiling running over a five-year period (Radio Occultation Data Buy II). Under this umbrella contract, it is only competing with PlanetiQ for the underlying data buys. In the most recent earnings call, we learned that Spire wasn’t selected for the first six-month order that started in July 2023. Based on my discussions with the company, I believe PlanetiQ might have offered more aggressive pricing, for example cost per RO profile. Whether or not its competitor was used by NOAA as sort of a bargaining chip relating to following orders, I assume management has drawn its conclusions from this decision. It’s worth mentioning that it is not the first time that they haven’t been awarded a contract during an ordering period by NOAA, only to win the following data buy then again.

According to a news article by SpaceNews, this $8 million contract was PlanetiQ’s first sale of operational radio occultation data for numerical weather models. Founded in 2015, the company has raised around $35 million to date and lists 23 employees on LinkedIn (in contrast, Spire posted the same number of job openings at the time of this writing). Unlike Spire, which has over 100 satellites in orbit along with over 500 years of space heritage, there are currently only two PlanetiQ satellites in orbit with a third one scheduled to launch later this year.

In addition, I was told by the company that there is a strong desire within the scientific community to incorporate up to 20,000 RO profiles per day into their numerical weather prediction models, even discussing quantities of up to 100,000 RO profiles to improve the prediction quality. Spire is capable of providing around 20,000 RO profiles per day which is more than what the rest of the world combined can deliver today (and around 6.5 times more than PlanetiQ can provide). Theoretically, it could also further expand its capabilities up to 100,000 profiles per day over the medium term (if there is indeed a demand for such a quantity). Based on that, management is very confident that they can secure a significant portion of this $59 million contract.

On a further positive note, given its large number of multi-sensor satellites, Spire was able to quickly pivot to RF geolocation use cases after the unexpected loss of this first NOAA order as outlined by CEO Platzer in the earnings call:

In the meantime, NOAA has reached out to us for other data types that we have with regard to weather. So that gives us great confidence on that. But even more importantly, it’s like the traction that we have seen as we have reallocated assets that are for RO into RF geolocation. And those contracts are multimillion-dollar contracts often for very, very short delivery times, and we have seen several of those coming repeatedly also from the same customer. So that reallocation has helped us a lot and given us great confidence in the growth. The momentum that we talked about a little bit on this call already that we have seen in the second quarter has carried into the third quarter. So overall, we feel very confident about the guidance that we have given.

In a nutshell, their software-defined technology allows them to optimize the amount of data they download for each one of their solutions and maximize the output from each satellite. In my opinion, with this high degree of adaptability Spire truly stands out from other NewSpace companies when it comes to tapping into a variety of income sources. It goes without saying that this technological ability can also be used as a bargaining chip in negotiations with all kinds of data purchasers.

Debt covenants

Before diving into the details of the loan agreement with Blue Torch Capital, we need to first set the scene. As of June 30, Spire had a cash balance (including securities) of $64 million and an outstanding term loan facility from Blue Torch with an aggregate principal amount of $120 million (apart from an interest-free government loan agreement amounting to $5 million). This credit facility – having a floating interest rate – matures in mid-2026 and comes with three (customary) financial covenants that will be examined in the following section.

According to the loan agreement (Section 7.03), these three financial covenants comprise: (a) Leverage Ratio (Financial debt / Adjusted EBITDA), (b) Total ARR Leverage Ratio (Financial debt / Annual recurring revenue (ARR)), and (c) Liquidity (minimum liquidity of $25 million at any time). Even though it was not completely clear to me from the definition of indebtedness in the agreement, it was confirmed by the company that the applicable debt amount for the covenant test only refers to the nominal Blue Torch facility of $120 million. While the minimum liquidity covenant is quite straightforward, the other two need to be analyzed in more detail.

Total ARR Leverage Ratio

This covenant has been applicable since the beginning of the credit period and runs through June 2024 (superseded then by the adjusted EBITDA covenant). For the time being, the financial covenants only relate to the ARR ratio which is tested on a monthly basis.

As of June 30, the Total ARR Leverage Ratio amounted to 1.06 ($120 million divided by the ARR of $112.8 million) which is below the stipulated upper limit of 1.10. Thus, the company was fully compliant with regard to its (financial) covenants in Q2. Having said that, after the unexpected loss of the first order under the NOAA contract, they might fail to comply with this covenant in Q3, at least based on the midpoint of their ARR guidance ($108 million would result in a ratio of 1.11 at the end of Q3). Blue Torch is fully aware of the current situation as Spire is obliged to send them monthly reporting packages including updates on the actual results and company projections. By doing so, any financial covenant issues can be addressed in advance. As far as I understand the situation, they have been proactively working with the loan provider on a solution.

Leverage Ratio

This covenant relating to adj. EBITDA targets will first be tested in June 2024. In the current version of the loan agreement, this covenant would require Spire to generate an adjusted EBITDA of $10 million in Q2, $13.3 million in Q3, and $20 million in Q4 of 2024. This would translate into an adj. EBITDA of over $43 million just for the last nine months of next year. For 2025, the loan agreement stipulates an adj. EBITDA of $160 million. To put these targets into perspective, it needs to be highlighted that the company is currently trading at a market cap of around $120 million. It’s worth mentioning that there are some cure rights in place (Section 9.02) in case Spire fails to meet these profitability targets.

My understanding is that they have already been discussing those targets with Blue Torch in advance, so they would adjust and resolve any issues well before those timelines are applicable. That said, management appears to be very happy about the deals they have closed to date in Q3 and the remaining 2023 pipeline across all four of their solutions.

Admittedly, the loan agreement contains some very tight and ambitious financial covenants. But based on my discussions, I’m positive that Spire and its lender will come to terms in due time. Just to put these financial targets into perspective, assuming they achieve the EBITDA targets implied by the current covenant thresholds the company could pay off the outstanding credit facility in 2025 – largely funded by that year’s free cash flow without any refinancing need (but keep in mind, the loan is not due until mid-2026). Based on that, I think there should be enough cushion built into those EBITDA targets for Blue Torch to consent to some covenant amendments – especially given the strong operating performance.

ATM offering

Again, starting off with a bit of background: following a dramatic decline in the share price since the IPO (de-SPAC date) in August 2021, Spire entered into an $85 million at-the-market (ATM) equity distribution agreement in September 2022. It appears that the possible need for a dilutive equity issuance down the road is directly related to the takeover of exactEarth in Q4 2021 – an acquisition that alone consumed $105 million of cash. Even though management hadn’t used it until June 2023, I still think the overhang from this potential equity offering combined with a stock that is lingering around the magical $1 threshold weighed heavily on the past share price performance.

In the most recent 10-Q and earnings call, we learned that management made use of this option for the first time, selling – adjusted by the split effect – 2.2 million shares at an average price of around $3.60 which amounted to cash proceeds of $7.9 million – a dilution of nearly 12%. This disclosure was not well received by the market, as evidenced by the share price reaction following the earnings release – despite posting a strong operating performance.

As outlined above, there hasn’t been any covenant breach so far (as per June 30, 2023). Based on the earnings call and my exchange with the company, the decision to raise cash at this point was arguably driven by three aspects that are sort of intertwined: first, it was solely management’s decision to take advantage of the high-volume day in the market when the reconstitution of the Russell indices occurred to raise some additional funds to bolster the balance sheet. Secondly, as stated above, Spire is currently proactively addressing any possible financial covenant issues with Blue Torch Capital in advance of a potential breach. Unsurprisingly, the debt provider was appreciative of the additional cash raised. And finally, management did expect to receive the $8 million from the first NOAA order.

How should an investor in Spire assess this decision now? I think one needs to evaluate this decision in light of the exactEarth acquisition in 2021 and the related debt issuance. Often in life, for a single bad decision, you must pay twice. Back then, management significantly overpaid for the company at an equity value of $131 million (approx. 7x EV/LTM revenue). The combined entity is currently valued at only around $120 million. That’s a lot of (shareholder) value destruction within a short period of time, at least in relative terms. From a capital allocation perspective, this was a string of bad corporate actions which brought the stock down where it is trading now – giving new investors the opportunity to benefit from management failures in the past.

On the other hand, we are probably faced with a binary event here. In the long run, this (minor) capital raise doesn’t change the big picture here either way. If they succeed, this decision will ultimately curb the huge upside only slightly. If not, it doesn’t matter anyway. Given the current covenant situation and a prospering business with highly attractive growth prospects, one could make the case that it was indeed in the best interest of long-term shareholders. Finally, it’s worth mentioning that CEO Platzer with a stake of more than 8% is the largest shareholder in Spire, so we can certainly agree that management’s and shareholders’ interests are aligned. If they are really serious about being close to profitability as they keep reiterating, I wouldn’t expect any further substantial capital raise.

Against this background, I was very happy to read that Spire significantly upgraded their management team in August by hiring a seasoned executive for the CFO role. Leo Basola joined the firm with immediate effect after having served as senior finance officer of Equifax International for more than four years, where he provided financial oversight for 23 countries and played a strategic role in growing data and analytics sales and improving margins. Prior to that, he was CFO at the Danaher subsidiary ChemTreat for five years. I firmly believe that having such a reputable executive now bodes well for future capital allocation decisions.

Valuation considerations

While acknowledging some questionable capital allocation decisions by management over the last two years, I still believe Spire is significantly undervalued from a risk-reward perspective. The stock became just another victim of the valuation crunch seen over the last 12-24 months within the NewSpace and SPAC universe. As outlined above, in contrast to many de-spaced but also NewSpace firms, the company seems to have a very robust competitive moat established by already having a fully deployed satellite constellation in low Earth orbit. Unfortunately, management hasn’t been very successful so far in effectively communicating the equity story to the investment community.

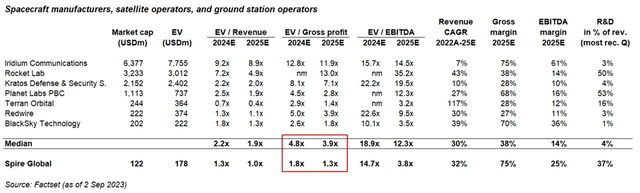

Considering the multiples that its closest space peers are trading at, it becomes apparent that Spire is valued at a significant discount to virtually all of them. The peer group is currently trading at median EV/Gross profit multiples of 4.8x (2024E) and 3.9x (2025E) respectively (accounting for the all-important operating leverage inherent in the respective business model, I consider the gross profit metric to be the most relevant one). In stark contrast, Spire only trades at 1.8x and 1.3x gross profit (2024E/25E), even though its financial profile metrics reflecting analysts’ consensus estimates exceed the respective median value of the peer group in each of the four benchmarking categories.

Source: Own calculation based on FactSet estimates

Assuming a valuation based on the peer group’s median gross profit multiples (2024E/25E), the stock would trade between $18.50 and $22.00. As a matter of fact, Spire’s most recent sell-side price targets per FactSet range between $20 and $32 (four analysts with a consensus price target of over $26 as of September 2, 2023). At the current share price, the implied probability – baked into the market pricing – that Spire will ultimately succeed is rather low given the envisaged EBITDA targets in the loan agreement and management’s most recent guidance. Consequently, it doesn’t need much to surprise the market to the upside.

Conclusion

This opportunity isn’t rated as a Strong Buy because there aren’t any risks involved in the investment thesis (as outlined above). The stock has suffered significantly from poor capital allocation decisions in the past rather than a weak operating performance or an unsustainable business model. IF Spire only comes close to the EBITDA targets stipulated in the current loan agreement over the next two years, there is a reasonable chance we will be talking about a billion-dollar company by then. Even assuming they are 2-3 quarters behind schedule, my investment thesis wouldn’t be dramatically different.

Following the implementation of the reverse stock, a position in the stock has been de-risked quite substantially, while at the same time opening the stock up to a more sophisticated and long-term oriented investor base. Adding to that, there are several catalysts in place, such as large new contract wins on the back of a more diversified customer base, further evidence regarding the achievability of its profitability timeline, or positive news relating to the financial covenant situation, which have the potential to lead to a significant re-rating of the stock in the short- and medium-term.

Read the full article here