Investment Rundown

In the most recent report from Primoris Services Corporation (NYSE:PRIM), there was a clear sign of strength in the top line from the company as they managed to grow the backlog immensely and also translate existing demand into growth. The revenues grew by 38% YoY to reach $1.4 billion for the quarter. This seems to have ignited the share price as Primoris continues to impress over the last 12 months.

I like the valuation of the business and even though there are some risks associated with having a high concentration on a few customers for growth, the upside potential heavily outweighs it right now in my opinion. As the company is gaining momentum from construction and investments in it the outlook remains solid as I think we are at the start of another boom for the US. I am bullish on the coming years for PRIM and will be issuing a buy for it right now.

Company Segments

PRIM operates as a distinguished specialty contractor company, catering to a diverse range of industries with its extensive portfolio of services. With a firm foothold in North America, PRIM excels in offering specialized fabrication, construction, replacement, and engineering solutions that cater to the unique needs of its clients.

The company’s operations are segmented into three distinct categories, each encompassing its sphere of expertise and contributions to various industries. The Pipeline Services segment constitutes a pivotal part of PRIM service offerings. Within this domain, the company plays a vital role in the construction, maintenance, and overall integrity of pipelines. From facilitating pipeline facility management to ensuring their operational integrity, PRIM brings its expertise to every aspect of this crucial infrastructure.

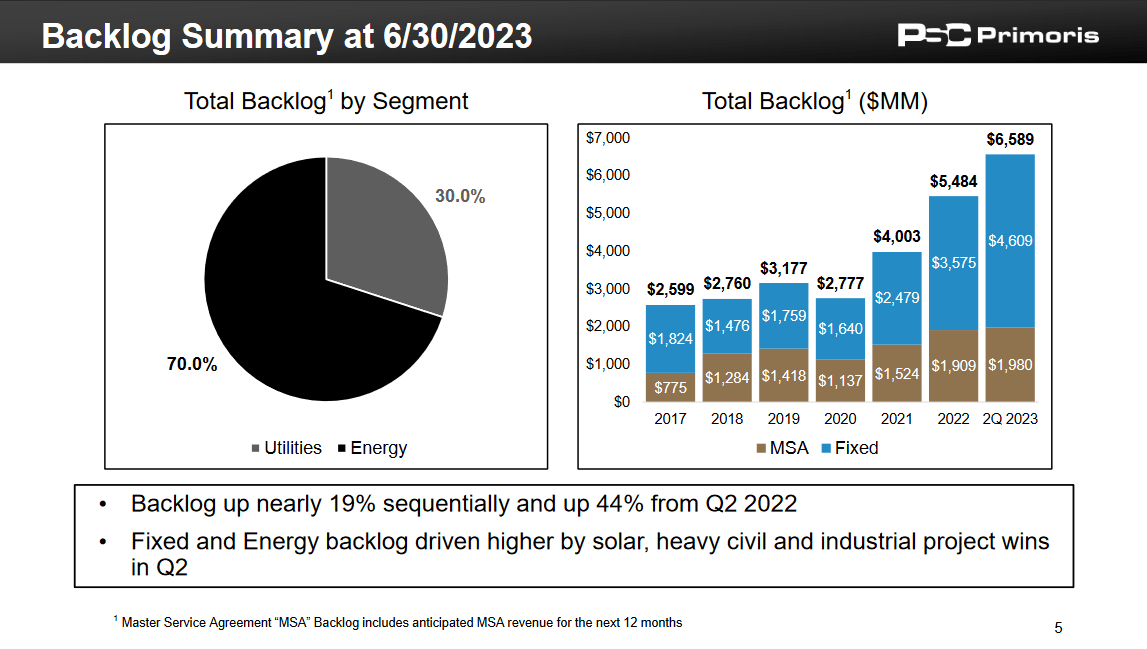

Backlog Summary (Investor Presentation)

One of the critical parts of PRIM right now is watching for strong momentum in the backlog growth of the business. In the last quarter, the growth was impressive and has been a primary reason for the strong appreciation in the value of the share price over the previous 12 months. Just every quarter the backlogs were up by 19%. The main growth drivers behind this came from solar, heavy civil, and industrial projects that PRIM won out on in Q2 this year. Seeing such strength brings me more optimism about the outlook for the company as it does tell a story about the market position the company has and the reliability one can have on them to continue acquiring projects and contracts.

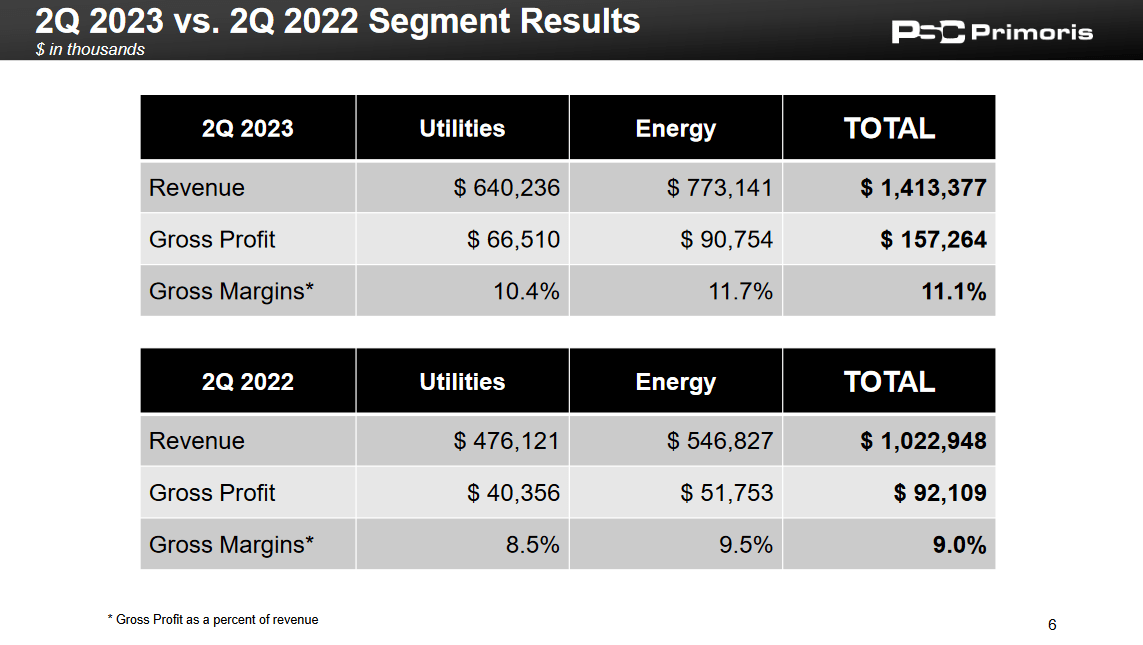

Q2 Results (Investor Presentation)

Another key highlight for the company is the growing margins too. The cost of products has been increasing as quickly as the revenues and this has of course led to some margin expansion for the business. What this tells me is that demand is increasing and PRIM can take advantage of this by raising prices without hurting backlog growth at all. This is also helping offset some of the higher interest expenses the company is forced to pay as a result of higher interest rates in the country.

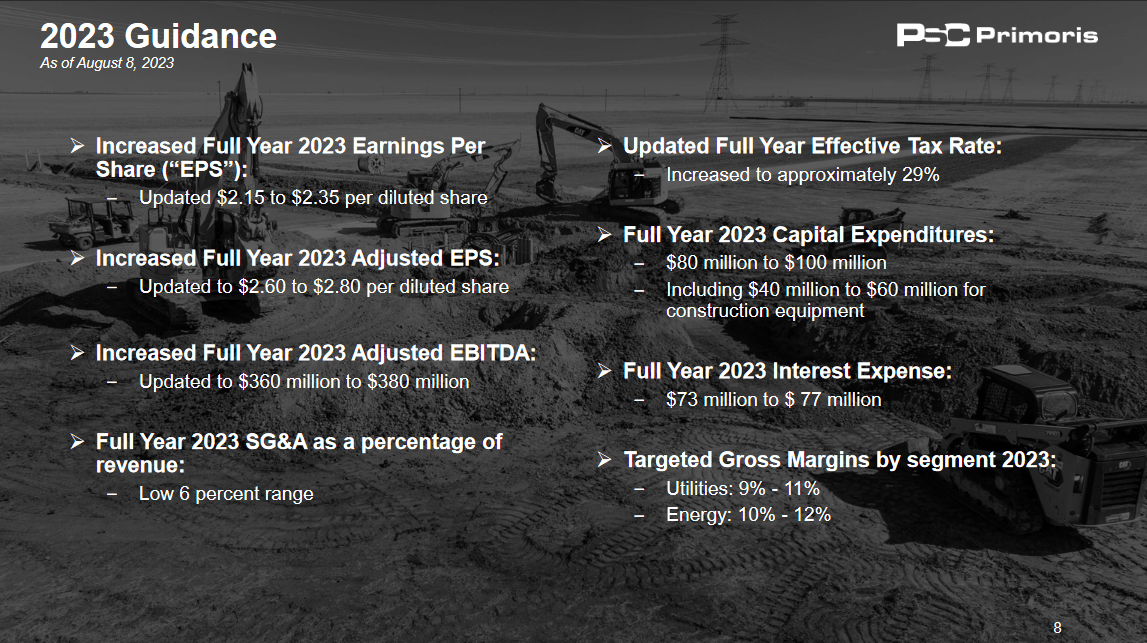

2023 Guidance (Investor Presentation)

Looking at the remaining part of 2023 I think the guidance remains very promising as the EPS is set to come at $2.15 – $2.35, a slight increase from previous estimates. Looking at the gross margins though there aren’t a lot of higher expectations than from what the last quarter had to offer. They are set to come in at 10 – 12% for the energy segment and 9 – 11% for the utilities segment. Pretty much in line with what the last quarter had to show.

Risks

The revenue dynamics of the company are intricately tied to the outcomes of diverse projects, ranging from significant construction endeavors to smaller initiatives funded through MSAs. The company’s financial performance hinges on the successful execution of these endeavors, reflecting the broad spectrum of projects it undertakes.

In the realm of more substantial construction projects, the company’s income is directly linked to the favorable completion and outcomes of these ventures. These larger projects contribute a significant portion of the company’s revenue and serve as key drivers of its financial health. However, it’s important to note that the culmination of a significant construction project doesn’t necessarily translate to a permanent loss of the client. Instead, the company’s ongoing relationship with the client may persist, albeit with varying implications for future revenue generation.

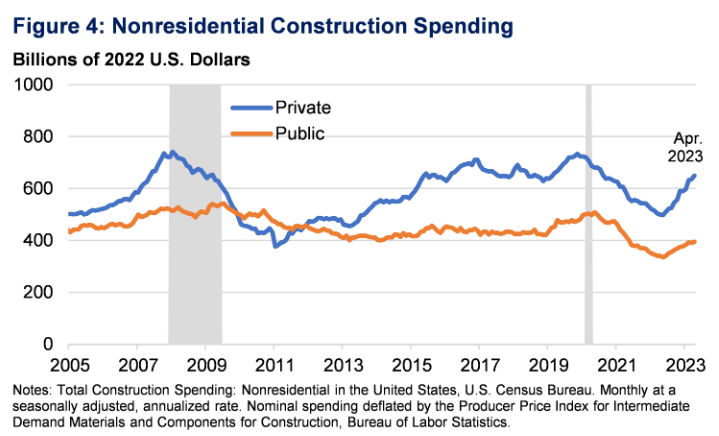

Construction Spending (US Census Bureau)

The composition of their client base is noteworthy, with the top ten clients playing a significant role in shaping their revenue landscape. In 2022, these top clients collectively contributed approximately 46.1% of their total revenue. This concentration underscores the company’s reliance on a relatively small group of clients for a significant portion of their financial performance. I think that this will likely weigh somewhat on the company as they aim to gather up more and more contracts and customers when investments into construction are increasing once again. In the medium term, I think we are in the face of another construction and manufacturing boom in the US and PRIM is very well positioned to take advantage of this, even regarding their high concentration on a few single clients

Final Words

The price for PRIM has been steadily increasing over the last couple of months but is yet to reach a point where I would be considering them heavily overvalued. At an earnings discount of around 40-50%, I would say that PRIM is heavily overvalued. Right now, the P/E is 12 or 26% below the sector. Looking more at the valuation, we can see that the P/S is very low at just 0.33. This, in comparison to the actual growth of the business, I think indicates that PRIM is a good deal right now based on those metrics. I think that operation in the construction and engineering industry the company is benefiting very well from direct investments into the space as it is rebounding. The market seems to be on the brink of another strong opening boom and I think PRIM is a great way to benefit from this. Higher demand and backlogs translating to better earnings should ultimately yield decent shareholder value as the dividend is increased and buybacks are possible to keep up. With a near 30% discount based on earnings as well for the company to the sector, I think it further solidifies it as a buy right now.

Read the full article here