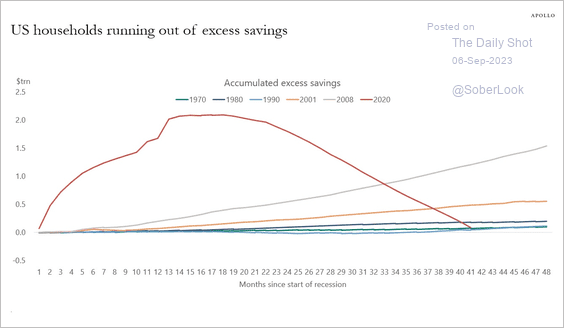

All eyes are on the consumer. Credit card use is on the rise as interest rates climb sharply. Excess savings are also being depleted among low-income groups, but the jobs market appears healthy (though not as hot as was seen earlier in 2023). Risky buy-now, pay-later (BNPL) firms face mounting challenges.

Still, I am upgrading Bread Financial (NYSE:BFH) from a hold to a buy based on a still-modest valuation and an improved technical situation.

Excess Savings Running Dry

Sober Look

According to Bank of America Global Research, Bread Financial is a financial services company providing simple, personalized payment, lending, and saving solutions. Bread offers a comprehensive suite of products including private label and co-brand credit cards, installment lending, and buy now, pay later (split-pay).

The Ohio-based $1.9 billion market cap Consumer Finance industry company within the Financials sector trades at a low 3.6 trailing 12-month GAAP price-to-earnings ratio and pays a moderate 2.2% dividend yield. Ahead of earnings next month, the stock has a moderate 35% implied volatility percentage, and its short interest is material at 7.3% as of September 6, 2023.

Back in July, BFH reported Q2 EPS of $0.95, topping analysts’ estimates thanks to a $15 million reserve release. The firm’s outlook dimmed a bit, however, as expectations for loan growth and net loss rates deteriorated. Amid the earnings beat, the management team remains cautious due to inflation and broader economic uncertainty regarding consumer trends, and lowered guidance for 2023. Loss rates are expected to stabilize over time, and the company authorized a $35 million share repurchase program.

With an executive team that is committed to growth initiatives, macro headwinds are many. The valuation accounts for the risks, though, in my view. Potential downside factors include an economic downturn leading to higher loan losses, increased defaults, and reduced loan growth. A weaker economy could also ding investor sentiment and reduce valuations further on this low-P/E name.

Good news hit earlier this month when RBC upgraded the consumer finance company due to possible benefits from a pending cut in late fees credit card companies can charge and the continued normalization of credit quality. But more firm-specific bad news struck in mid-August when Bread reported that its delinquency rate rose past pre-pandemic levels in July.

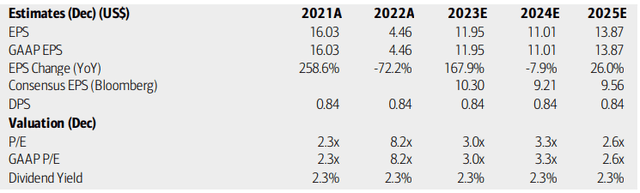

On valuation, analysts at BofA see earnings snapping back to normalized levels this year after a poor 2022. The annual EPS figure should revert to near $11 over the coming quarters while 2025 earnings power appears strong with per-share profits topping $13. The Bloomberg consensus forecast is not as sanguine as BofA’s outlook, though.

Dividends, meanwhile, are seen as holding at $0.22 quarterly. With very low earnings multiples, there continues to be a valuation appeal with the stock – something I highlighted when I last reviewed the name in the first half of 2023.

Bread Financial: Earnings, Valuation, Dividend Yield Forecasts

BofA Global Research

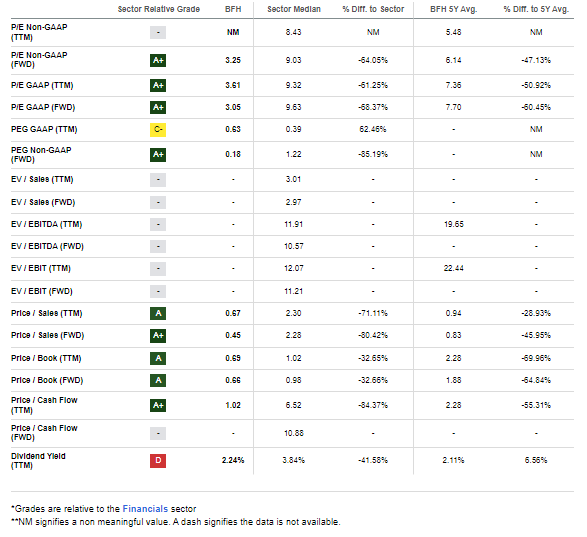

Looking closer at the valuation, if we assume $11 of normalized earnings and apply a sector-median multiple, then the stock should be multiples of where it is now. But BFH is a highly risky BNPL firm, particularly susceptible to downturns in the consumer cycle.

Thus, we have to discount the P/E. If we assign a 5x earnings multiple, below its 5-year historical average amid higher interest rates today (the firm has $4.7 billion in debt), then the stock is still substantially undervalued – $55 versus $37 today. Thus, I continue to like the stock on valuation.

BFH: Compelling Valuation Case

Seeking Alpha

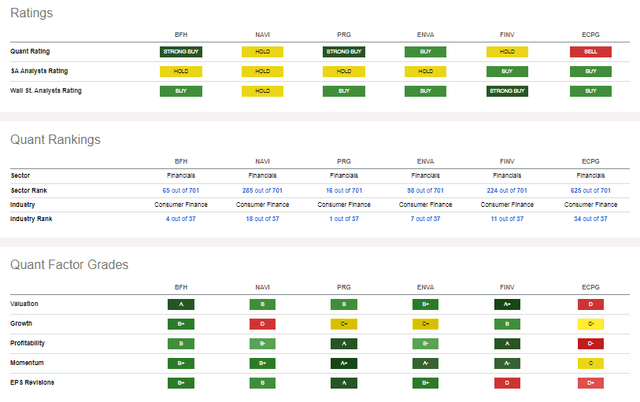

Compared to its peers, Bread stands out. Notice in the ratings view below that the firm has extraordinarily strong quant metrics which cannot be said of its rivals. With the dirt-cheap valuation mentioned above, a robust growth profile, high profitability, strong stock price momentum, and likewise healthy EPS revisions, there are several tailwinds. The over-arching risk remains the sensitive consumer, of course. Overall, the stock ranks 4 out of 37 in its industry.

Competitor Analysis

Seeking Alpha

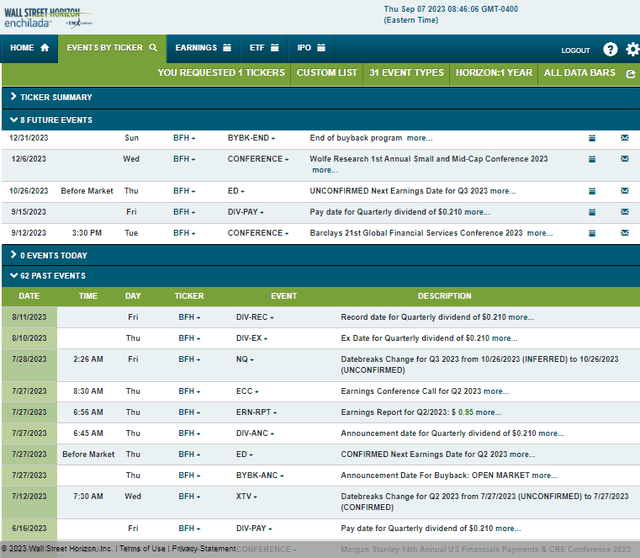

Looking ahead, corporate event data provided by Wall Street Horizon shows an unconfirmed Q3 2023 earnings date of Thursday, October 26 BMO. Before that, the management team is slated to present at the Barclays 21st Global Financial Services Conference 2023 from September 11 to 13. After the reporting date, another speaking engagement happens in December at the Wolfe Research 1st Annual Small and Mid-Cap Conference 2023. So, there are few volatility catalysts in the offing.

Corporate Event Risk Calendar

Wall Street Horizon

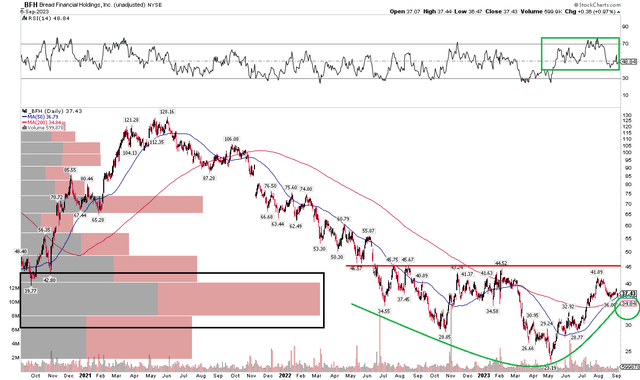

The Technical Take

I was admittedly much too bearish on Bread’s chart back in April. I outlined how the low $20s was support, and shares indeed troughed near $23 the following month, but that was a fantastic risk/reward opportunity considering the valuation. My mistake was not outlining that investing idea with a ‘buy’ rating. Today, the valuation case remains intact, and the chart shows more bearish to bullish reversal signals.

Notice in the chart below that BFH has resistance in the mid-$40s, as previously described, but the long-term 200-day moving average is now upward-sloped, a sign that the bulls are taking ownership of the broader trend. What’s more, the shorter-term 50dma has climbed above the 200dma in a golden cross pattern. Finally, the RSI momentum indicator at the top of the graphs is oscillating in the bullish 30 to 80 zone. I see support in the $33 to $35 zone with another layer of potential buying support in the $28 to $29 area.

Overall, the chart is encouraging, though the risk/reward is not as encouraging as back in Q2.

BFH: Bearish to Bullish Reversal, $45 Resistance

Stockcharts.com

The Bottom Line

I am upgrading BFH from a hold to a buy. I regret not putting a buy rating on it in April, but the valuation case is there, and the long-term trend may be reversing higher.

Read the full article here