Consumer appliance company, SharkNinja (NYSE:SN) was recently spun out of a larger Hong Kong listed firm. There are reasons to believe that a spin-out may temporarily depress the share price and that Shark Ninja could be somewhat undervalued at current levels.

Why Spin-Offs Can Be Attractive

Spin-offs from existing companies can tend to outperform the market on historical analysis. There’s logic to that because these new companies can benefit from greater management focus when compared to being subsumed in a larger entity. Plus, in some cases, spin-offs are ultimately acquired at a premium. The company also has high insider ownership with a robust track-record and viable strategy. As SharkNinja shares find a home with investors learning about this recently listed company and shows strong performance in 2023 as H1 numbers suggest, then the shares may appreciate.

Technical Factors

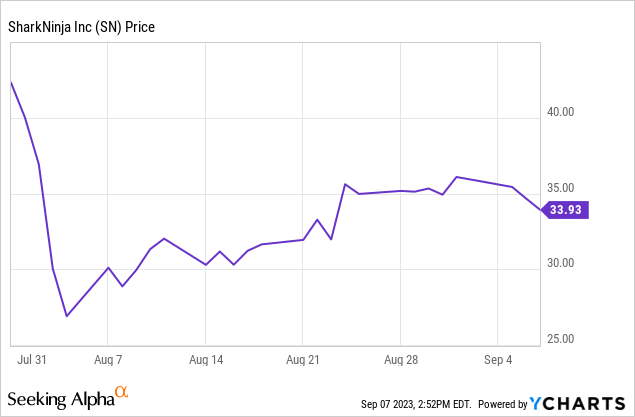

The technical factors may be quite encouraging, for those looking for value, because the legacy parent company, JS Global Lifestyle is listed primarily in Hong Kong, whereas the spin is U.S. listed. That may create a setup where those receiving the shares, blindly sell them rather than holding them for the long-term. It’s unlikely that investors trading primarily on the Hong Kong exchange want to own U.S.-listed shares.

This could create technical pressure, causing the shares to be undervalued. This may have been what happened since the spin-out occurred in late July. At some point, the indiscriminate selling should end and the shares will find a home with those more willing to own a U.S.-listed consumer appliance company. Of course, should it occur, that process can take several months.

Valuation – Relatively Attractive

SharkNinja’s valuation is relatively attractive if you assume they can continue to grow through geographic expansion and product innovation, which seems a fair bet based on their history. Of course, this is not a cheap company in absolute/static terms but may be attractive once incremental growth is considered.

Over its recent fiscal years (which align with the calendar year) SharkNinja has seen declining profitability and reduced gross margins. However, outside of the U.S. and China, the company has plenty of room for international growth and from entering new categories as it has done previously in categories such as ice-cream makers, grills, and air fryers. Encouragingly, Q2 results were generally strong, showing a return to growth but with some additional costs as a result of the spin, which is not unusual. It was also a positive that the cash flow results were stronger than profitability on the income statement.

Below I show the company’s P/E valuation in historic terms and how the business might look in 2025 if it can grow at rates consistent with H1 2023 of 14%, which is below its historic CAGR of 20%. That analysis assumes no change in margin structure.

| Year | 2020 | 2021 | 2022 | 2025e illustrative 14% net income CAGR from 2022 |

| Net income | $327M | $331M | $232M | $343M |

| Implied current P/E based on year shown | 14.4x | 14.2x | 20.3x | 13.7x |

Source: Company reporting, author’s analysis

The company was likely a Covid-19 beneficiary. As we’ve seen that, in many areas, purchases of goods spiked to unusually high levels as people had extra cash and couldn’t buy typical services. That may mean that the results of 2020-21 were probably abnormally good for the company as people stayed home and cleaned their carpets and blended smoothies.

Nonetheless, the overall picture for SharkNinja appears to be one of structural growth as the company innovates to meet customer needs and expands geographically. In this regard, H1 2023 results were broadly encouraging as the company has seen growth in sales, gross profits, and operating income of 14%, 24%, and 12% respectively compared to H1 2022. That’s not inconsistent with the company’s topline sales CAGR of 20% between 2008 and 2020. However, a sharp rise in other expenses, associated with the spin, caused earnings per share to decline to $0.71/share for H1 2023 compared to $0.76/share in H1 2022. Management quantified these costs as $35.1M, and it is likely the majority of these are one-time expenses, which suggests that normalized EPS grew to in the region of 0.80-$0.90/share in H1, we’ll get a better look at normalized expenses with the Q3 results.

It was also encouraging that the bulk of this growth came in the newer category of cooking and beverage appliances, where the company saw notable growth in Europe (especially the U.K.) and traction from the launch of its outdoor grill. However, the largest category of floor cleaning did see a slight decline in H1.

Business Quality

I believe SharkNinja is a quality business. Many of its recent innovations have landed, and the company typically demands premium pricing for its products of $200-$300 suggesting that customers see the value in its offerings and the reviews attest to that too.

The company appears to have adapted to the evolution of the multi-channel and online-centric retail landscape, with a focus on 5-star reviews over 3,000 patents and a sales CAGR of 20% between 2008-2022. Of course, the appliance market is competitive and not all innovations will land and margins on legacy products may erode over time, but the company appears to have a solid track record in driving innovation and has developed underlying sales and marketing expertise to support its products. It’s also encouraging that the company likely has some runway for growth in Europe and other markets outside of the U.S. and China, even without relying on future product innovation.

Insider Ownership

Alignment of incentives can go a long way in equity investing, and it’s encouraging that the Chairman owns 57% of the equity. Of course, that may also create limitations for the free float and inclusion in certain indices, but overall it’s likely a positive.

Risks

- An obvious risk for a company selling $200-$300 appliances to make ice cream and smoothies is that a weakening global economy would hurt sales. We’ve recently seen an uptick in unemployment and interest rates are at high levels, so deteriorating economic growth may weigh on the shares in the short-term. That said, the current macro risks are unlikely to be news to the market.

- The Chairman holds 57% of the shares, alignment of incentives is a positive to a degree, but he may act in ways that benefit his own interests rather than the broader company and the limited free float may prevent certain investors from owning the shares.

- The company does not control its channels directly and may see margins eroded by retailers over time and/or from copycat products where they have success.

- We’re still learning how the stories of Covid-19 beneficiary companies, of which SharkNinja likely is one, play out. It appears we’re now back to a more normalized post-Covid environment, and we’ve seen the trough after the Covid-19 boom in certain categories, but we’re still learning.

Conclusion

While not screaming cheap, SharkNinja is likely undervalued as a long-term growth play within consumer appliances. The company has a strong track record of innovation and a robust platform to support its business and that likely will continue.

It is likely earnings will increase over the coming years, fueling share price appreciation, and some multiple expansion is also possible if the company continues to execute. H1 results, notwithstanding exceptional costs, were encouraging, and if that trend continues and the likely post-spin selling of the shares abates over the coming months in favor of more dedicated owners of the shares, then the shares may perform well. That said, macro headwinds for consumer discretionary products should be monitored closely.

Read the full article here